A financial plan is a road map to help guide you to a better future. Not just about budgeting or investing, a good financial plan will help you navigate your way through all of life’s major financial milestones.

On one hand, your financial plan acts as a set of rules or principles by which to live. Think of Harold Pollack’s famous ‘index card financial plan’ which lists nine rules such as; save 20 percent of your money, max out your retirement account each year, pay off your credit card balance in full each month, and pay attention to fees. It’s something you can carry with you all your life.

On the other hand, your own financial plan needs to be malleable and allow you to adjust course when life throws you a curveball. Sure, your core principles might stay the same, but finances can change in a hurry when you get married, have kids, buy a house, suffer an illness or disability, get divorced, move across the country, or gear up for retirement. Your financial plan should act as a compass to get you back on track.

While a financial advisor can help you set up with a plan, many are focused solely on product sales such as mortgages, investments, and insurance. They’re not likely to ask where you see yourself in five years, and might not truly understand your short-and-long-term money needs.

A better option might be to work with a fee-only financial planner who can take an objective look at your overall financial health and draw up a plan to help you reach your goals. The challenge is a lack of fee-only advisors in Canada, plus a comprehensive plan could set you back several thousand dollars.

One idea is to create a basic financial plan of your own. The process alone will allow you to think about money in ways you never have before. If in the end you have more questions than answers, by all means reach out for professional guidance.

Here are eight steps to help create your own financial plan:

Create Your Own Financial Plan

Step 1: Identify your goals

Sit down with your spouse and have a frank conversation about your short-and-long-term goals. That could mean paying down credit card debt, saving up for a new car, or continuing to max-out your TFSA or RRSP so you can retire early.

Agree on the top three or four goals and then rank them in order of priority. We’ll come back to these later.

Step 2: Determine your net worth

You have to figure out where you are now before worrying about where you want to go in the future. Take a snapshot of your current financial situation by creating a net worth statement.

Add up all of your assets and subtract your liabilities. What’s left over is your current net worth.

Step 3: Check your cash flow

One of the keys to building a strong financial plan is to understand how much you spend and save. Use a spreadsheet or app to track what money is coming in (wages, interest, government benefits) and what’s flowing out (rent, debt payments, utility bills).

Fill in all your monthly expenses in one column and your annual expenses in another column. Add up your expenses in both columns and subtract them from total net income on both a monthly and yearly basis. The result is your cash flow deficit or surplus.

Tracking your cash flow can give you a sense of control and confidence that makes it easier to implement financial changes in your life.

Step 4: Match your goals to your spending

You’ve already identified your goals and determined your cash flow. Now it’s time to compare spending to your goals and see how they match-up. The idea here is to look at how well your current spending habits mesh with your goals.

If you have a cash flow deficit you won’t be able to meet your goals, so you’ll have to see if you can free up cash by cutting back your spending in areas that are less important to you. If you have a cash surplus, that’s great! You can start allocating money to meet your goals right away.

Step 5: Review your insurance coverage

Most employer group plans offer minimal life insurance coverage. With some basic calculations you can determine whether you have enough. A good rule of thumb for life insurance is to get enough to pay off any debts owing, plus cover 10 times your income if you have kids under 10 years old, and five times your income if you have kids over 10.

Your workplace coverage should also include disability insurance, but if it doesn’t, get enough to replace at least 60% of your after-tax income.

Step 6: Reduce your taxes

Tax planning can be fairly straightforward for most families and you’re likely already taking advantage of the best tax shelters if you own your home and contribute to your RRSP, RESP and TFSA.

However, if you are self-employed or rely on commission income, rental income, or significant investment income, consider hiring an accountant to help with income tax planning.

Step 7: Create an investing policy

Every financial plan should include an investment policy statement that advises how your portfolio should be invested. An investing policy written down on paper can help you to stay the course with your investments whenever markets get volatile.

The policy can be as simple as stating that you want to invest in low cost, broadly diversified index funds or ETFs that you will rebalance annually to maintain an allocation of 25% Canadian equities, 25% U.S. equities, 25% international equities, and 25% Canadian bonds. Any new money will be added to the lowest valued fund so that you’re guaranteed to ‘buy low’.

Step 8: Create or update your will

Every adult who owns assets and has a spouse or children should have a will. An accurate and up-to-date will is the only way to ensure your assets will be distributed the way you want them to be, and not left up to the courts to decide.

56 percent of Canadian adults do not have a legal will. Now you can create a legal will online in 20 minutes for as little as $99 thanks to Willful Wills.

Final thoughts

While most people could benefit from working with a financial advisor, anyone can go through these eight steps and create their own financial plan.

At the very least, it’s a good idea to take stock of your own finances from time-to-time to see where you stand. Open up the dialogue with your spouse and even with your kids. Talk about your financial goals and get all of your money concerns out in the open.

What you’ll end up with at worst is a basic idea of your financial position and where you want to go. At best, you’ll have a set of guiding principles to lead you to a better financial future.

Canada’s big banks rollout new fee increases every year or two. These fee hikes may seem innocuous at first – 50 cents here and $1 there – but they collectively (and annoyingly) add up to big bucks over time.

My advice for Canadians who want to remain with a big bank but don’t want to pay excessive fees is to downgrade to a basic chequing account, maintain a minimum balance, and use a cash back or travel rewards credit card for everyday spending instead of using debit (which can incur more fees).

But that’s becoming more and more difficult as banks continue to hike monthly fees, increase the minimum balance requirement, tie the account fee reduction to holding multiple (fee-based) products, and in some cases not even offer the option to waive the fee with a minimum balance.

For example, TD’s all-inclusive plan costs $29.95 per month and requires a minimum monthly balance of $5,000 to waive that fee. Their Everyday chequing account costs $10.95 per month and includes 25 transactions. The fee is waived when you maintain a $3,000 minimum balance.

Canada’s largest banks (and others) have all signed a public commitment to offer low cost and no cost accounts. Youth, students, seniors, and RDSP beneficiaries may be eligible for a no cost account that includes basic features.

| Bank / Account Name | Monthly Fee | Maximum number of monthly debit transactions | Minimum monthly balance (for monthly fees to be waived) |

|---|---|---|---|

| BMO / Practical Plan | $4.00 | 12 (in-branch and self-serve transactions) | — |

| CIBC / Everyday Chequing Account | $3.90 | 12 (in-branch and self-serve transactions) | — |

| HSBC / Performance Chequing - Limited | $4.00 | 14 (in-branch and self-serve transactions) | — |

| National Bank / The Minimalist Chequing Account | $3.95 | 12 (includes 2 in-branch transactions) | — |

| RBC / Day to Day Banking | $4.00 | 12 (includes in-branch and self-serve transactions) | — |

| Scotiabank / Basic Banking Account | $3.95 | 12 (includes 4 in-branch transactions) | — |

| TD Canada Trust / Minimum Account | $3.95 | 12 (includes 2 in-branch transactions) | $2,000 |

Consumer advocates will call these fee hikes a money grab (as I did in this Global News column) and they’re right. Big banks get away with increasing fees because they know that most Canadians will begrudgingly accept them. Chequing accounts are ‘sticky’ products and customers simply don’t want to go through the hassle of switching banks, or don’t know that free options exist outside the big bank environment.

I recognize that it’s not practical for some people to hold a basic account with a low number of transactions, or to keep thousands of dollars tied-up in a chequing account just to waive monthly fees. In that case I think you can make one last-ditch effort to negotiate your monthly fee down to an acceptable level (as I’ve done) before you need to seriously consider moving to a no-fee bank account.

For no-fee banking options that come with a debit card I’d look at Tangerine, Simplii, Motive, or a local credit union. You’ll get access to a limited number of ATMs (Scotia, CIBC, or the Exchange network of ATMs) and can typically get unlimited free transactions, including bill payments and e-Transfers.

The one downside to moving away from a big bank environment is the lack of branch access. For example, if you need a bank draft to make an offer on a house you may not be able to get one for 48 hours or more if you deal primarily with an online bank.

Canada’s big banks continue their relentless assault on our wallets by nickel-and-diming us to death with fee increases. It doesn’t have. to be this way. In the age of FinTech, there is a better and cheaper option available outside the big banks in every line of business in which they operate. It’s time to explore those options if you haven’t already.

This Week’s Recap:

I recently shared with readers what’s in my wallet and looked at some excellent rewards credit card options.

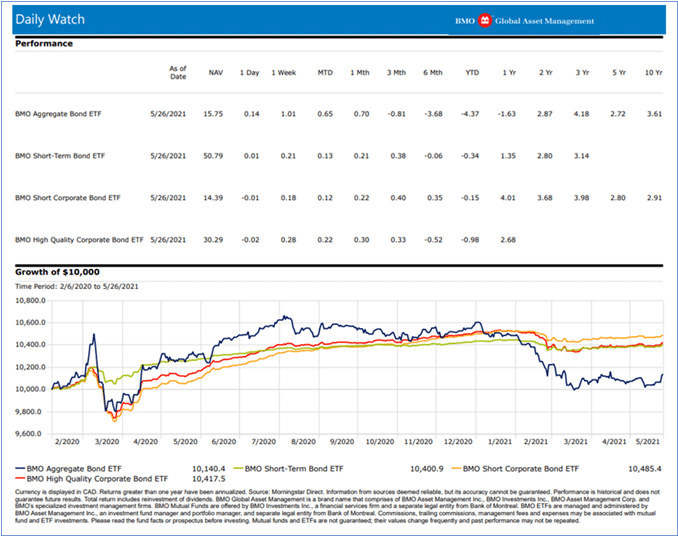

On Wednesday I took a deep dive into BMO’s line-up of fixed income ETFs.

Over on Young & Thrifty I explained exactly how to transfer your RRSP or TFSA to Questrade.

We’re getting our minds back into travel mode (finally) and so here’s my Airbnb versus hotels comparison on Rewards Cards Canada.

Promo of the Week:

Our friends at Credit Card Genius have outdone themselves with this one. Sign-up for Canada’s top cash back credit card – the Scotia Momentum Visa Infinite Card – and you’ll also get a free $100 Amazon.ca gift card.

The card still offers an incredible 10% cash back bonus for the first three months, 4% cash back on groceries and recurring bills, 2% back on gas and daily transit, and 1% back on everything else. All of this, and the $120 annual fee is waived in the first year.

Weekend Reading:

Purpose Investments introduced a new mutual fund for seniors that targets an initial lifetime income payment of 6.15% (for investors aged 65 to 67). It’s an annuity wrapped up in a mutual fund, with a pooled structure that takes advantage of mortality credits to meet its long-term goals.

Fee-only planner Jason Heath shares the top mistakes that do-it-yourself retirement planners most often make:

“Life expectancy is easy to misjudge for a retiree. The current life expectancy is age 80 for a Canadian man and age 84 for a woman. However, those are the average ages of men and women at death. A 65-year-old man has a 50 per cent probability of living to age 89, and for women, it is age 91. For a 65-year-old husband and wife, there is a 50 per cent chance that one of them will live to age 94, so at 65, they should plan for a 30-year retirement.”

Here’s why retirees need to heed the sequence of returns risk in their portfolios.

This Globe and Mail article explains when it makes sense to withdraw funds early from your RRSP.

An interesting post at Money We Have looks at collecting CPP and OAS when retiring abroad.

Michael James on Money explains how to lie to yourself about a stock crash with statistics. This is in a response to a particular advisor who has been beating the drum about a stock market bubble for the past 15 months.

PWL Capital’s Shannon Bender explains how to calculate your investment returns using the Modified Dietz Method:

The Monevator blog explains how self-directed investors can keep their investment portfolios on track.

Nick Magguilli (Of Dollars and Data) explains how we become so obsessed with millionaires?

A Wealth of Common Sense blogger Ben Carlson digs into 200+ years of asset class returns to find some interesting nuggets:

“There is a very good case to be made that returns over the next 50-100 years will be lower than they’ve been over the past 50-100 years.”

If being a landlord is part of your retirement plan, read this first. Agree 100% – I would not recommend owning rental properties in your retirement years.

Finally, here’s the Blunt Bean Counter with a must-read article on estate planning: “My kids will never fight over my estate.”

Have a great weekend, everyone!

This article has been sponsored by BMO Canada. All opinions are my own.

Fixed income doesn’t get enough attention on this blog, mostly because I’m still in my accumulation years and invest in 100% equities across all my accounts. But most investors should hold bonds in their portfolio to reduce volatility and so they can rebalance (selling bonds to buy more stocks) whenever stocks fall.

In this post we’re going to take a deep dive into BMO’s line-up of fixed income ETFs. We’ll see that there isn’t a one-size-fits-all approach to investing in fixed income, and that investors can capture yield using a wide array of products and strategies.

DIY investors should be familiar with BMO’s suite of fixed income ETFs. It’s the largest in Canada with more than $23 billion in assets. At the top of the list is BMO’s Aggregate Bond Index ETF (ZAG) with total assets of $5.86 billion.

Robo advised clients also have BMO fixed income ETFs in their model portfolios.

- Nest Wealth clients hold BMO Aggregate Bond Index ETF – (ZAG)

- Wealthsimple clients hold BMO Long Federal Bond Index ETF – (ZFL)

- Questwealth clients hold BMO High Yield US Corp Bond Hedged to CAD Index ETF – (ZHY)

- ModernAdvisor clients hold BMO Emerging Markets Bond Hedged to CAD Index ETF – (ZEF)

BMO Fixed Income ETFs

Investors are nervous about holding bonds today. Interest rates are at historic lows, and when rates eventually rise, we’ll see bond prices fall – especially longer duration bonds. We’re also seeing higher inflation, which causes interest rates to go up (and bond values to go down).

I reached out to Erika Toth, Director at BMO ETFs to talk about fixed income ETFs and how investors should think about bonds and fixed income today and into the future.

Q: Erika, investors are concerned about low bond returns, particularly from long-term government bonds. How should they think about the fixed income side of their portfolio?

A: Investors should think of fixed income as a ballast in their portfolio. It helps reduce overall volatility (chart below). Correlations between US Treasuries and stocks (represented by the MSCI USA index) have been negative over the last two decades. All that to say, when stocks fall, bonds tend to do well.

From an investor perspective, there are two things at play – FOMO, and fear of volatility. Fixed income still has its traditional value in a portfolio; to offset equity risk.

What we are seeing from some clients is the willingness to take on more equity risk – shifting from a 60/40 balanced portfolio to 70/30 portfolio, as an example.

But you can see the payoff from fixed income using a simple example of Canadian equities (represented by ZCN) and ZAG. Volatility drops materially without costing investors too much return.

| ETF | 10-year annualized return | Standard deviation |

|---|---|---|

| ZCN | 6.21% | 11.8% |

| ZAG | 3.69% | 4.0% |

| 60/40 (ZCN/ZAG) | 5.38% | 7.4% |

| 70/30 (ZCN/ZAG) | 5.61% | 8.5% |

The bottom line: Fixed income keeps investors in the markets during times of distress.

Q: What about a retired investor who typically holds a 60/40 or 50/50 portfolio but is concerned about generating income in a low-yield environment?

A: Such an investor may wish to include ETFs that harness option writing strategies such as covered call writing, put writing, or a combination of the two, to generate a high level of tax efficient monthly cash flow (option premiums are taxed as capital gains and/or return of capital).

With fixed income generating lower yield today, the equity portion of a portfolio needs to make up for the yield shortfall. Covered call strategies are an efficient way to do so and ETFs are a convenient way that allow investors to attain access.

Here are a few examples of these types of strategies. I would include these on the equity side of the portfolio to increase overall level of yield:

- ZWC BMO Canadian High Dividend Covered Call ETF, yields 7.3%

- ZWB BMO Covered Call Canadian Banks ETF, yields 5.84%

- ZWS BMO US High Dividend Covered Call Hedged to CAD ETF, yields 5.94%

Q: I’m a big fan of asset allocation ETFs to make DIY investing as simple as possible. But is it wise to unbundle ZGRO or ZBAL and hold multiple ETFs with the intention of avoiding long-term bonds in favour of shorter duration government bonds or corporate bonds?

A: Part of the appeal of the all-in-one asset allocation ETFs is their simplicity; and they tend to appeal to investors who do not want to get granular in their investment process. The other benefit of a one-line holding is that you are less likely to overthink the underlying components and make reactive decisions when you see something go into the red.

The 0.18 % management fee (0.20% MER) for ZGRO and ZBAL are all-in, there’s no double-dipping on fees. That is basically the cost of underlying ETFs with almost nothing more for the rebalancing. Keep in mind that there is often a trading cost for rebalancing multiple ETFs on your own. For investors with small portfolios, the cost of selling and buying stocks and bonds every year can become proportionally expensive.

Portfolio rebalancing is the maintenance involved in sticking with your asset allocation plan. Your asset allocation plan is what is going to help you meet your goals. One of the biggest pros to portfolio rebalancing is that it keeps risk under control, and sometimes just maintaining a level of risk takes some action.

There is tremendous value to having the rebalancing done systematically. Conservatively, experts say it can add between 0.30% to 0.40% annually over the long term.

For an investor who does not mind doing a handful of trades and rebalancing once or twice a year, the “unbundling” strategy could work. However, if the concern is rising rates, corporate bonds would tend to do better than government bonds.

I would opt for something like ZCS (1-5 year laddered Canadian corporate bonds, all investment grade) over ZSB (which is 2/3 government bond and 1/3 corporates). The MER’s are almost identical at 0.11% and 0.10% respectively.

The downside to switching to a short duration bond ETF is that you would not participate in gains should we revert to another period of falling rates in the future.

Below are the total returns over the last 15 months for ZAG, ZCS, and ZSB. I have also included ZQB (which is only ‘A’ and above rated corporate bonds) for investors who want corporates but only of the best quality (no BBB’s).

Ultimately, the decision to unbundle an asset allocation ETF or not would depend on the investor’s preferences, portfolio size, time limitations, and investment expertise.

In our model portfolios, and in our managed ETF portfolios, we maintain ZAG as a core portion of our fixed income exposure (though we have complemented it with rate reset preferred shares, short-term US TIPS, and corporate bond ETFs to mitigate the impact of rising rates & inflation).

We want to have some duration exposure to provide a hedge in times of equity market corrections. Longer duration bonds provide an offset to equity market risk in a well-balanced portfolio.

Q: BMO has a broad line-up of fixed income ETFs. What’s an under-the-radar option for someone who’s concerned about inflation and falling bond prices?

A: Here are some links to a few recent fixed income resources:

- 3 tools to optimize your fixed income portfolio – discusses ZEF (BMO Emerging Markets Bond Hedged to CAD Index ETF), ZPR (BMO Laddered Preferred Share Index ETF) and ZTIP.F (BMO Short-Term US TIPS Index ETF (Hedged Units)

- Rising rates & ZAG – In this piece, Alfred Lee discusses how allocating 15% of your core fixed income towards ZPR and ZTIP.F can help mitigate the impact of rising interest rates.

- Fixing your bond portfolio – a useful guide on the fixed income portfolio construction process.

Fun fact: BMO has more bond ETFs over $1 billion and over $500 million than any other provider and offers the widest choice of fixed income exposures.

Final Thoughts

Thank you to Erika Toth from BMO ETFs for taking us through BMO’s fixed income line-up and sharing her ideas on how investors should think about bonds in the current environment.

With interest rates at historic lows, we certainly can’t expect the same future returns from bonds as we’ve enjoyed over the last 25-30 years.

Here are my two takeaways from this interview:

One: Investing in a low cost, risk appropriate, broadly diversified, and automatically rebalancing portfolio is a smart choice for the vast majority of investors, regardless of the current market conditions or interest rate environment. You can do this by holding a single asset allocation ETF in your discount brokerage account, or by investing through a robo-advisor.

The longer duration bonds held in these portfolios may not be ideal for this environment, but they can be beneficial if stocks fall sharply (as they did in March 2020).

Two: For investors who prefer to take a more hands-on approach to their investments, particularly on the fixed income side, they’ll find a wide range of options including TIPS, high grade corporate bonds, and emerging market bonds.

Yield hungry investors can also delve into the world of covered call strategies to potentially juice the income on the equity side of their portfolio. This includes products like BMO Covered Call Canadian Banks ETF (ZWB).

Readers, have you changed the way you look at the fixed income side of your portfolio? Let me know in the comments.