House prices across the country continue to soar. The average price for a home in Canada reached $695,697 in April, up an incredible 41.9% year-over-year. Ontario is driving the majority of those gains, as the province’s average price rose 46% during the same period.

Would-be homebuyers are getting into bidding wars and paying several hundred thousand dollars over the ask price to get their desired home. Insanity.

These bidding wars are wild. My house is worth less than what this house sold for over the list price. pic.twitter.com/u4vjZDRHPt

— Boomer and Echo (@BoomerandEcho) May 21, 2021

A reader bid $250,000 over the list price on the above home, but ultimately was not even close after multiple bids came in at an even higher price. The same reader put in two offers on different properties and lost in a bidding war. Houses are selling in just a few days.

“We find ourselves in a market where buying first seems to be the only path, because if I sold first, then tried to buy, I could be homeless! It is so crazy…makes us wonder if we want to play.”

Related: Buyers fed up with blind bidding, other shenanigans in red hot real estate market

Not every region in Canada is experiencing a real estate boom, mind you. The latest episode of the Globe & Mail’s Stress Test podcast featured a 30-something who moved from Toronto to Saint John and bought a house for $99,000.

Prices in my area (Lethbridge, Alta) are up 14% year-over-year but with an average price of $317,222 it’s still well below the national average. Here’s a look at how the provinces compare in average home price and year-over-year change:

| Area | April 2021 | April 2020 | % Change |

|---|---|---|---|

| Canada | $695,657 | $490,082 | 41.90% |

| BC | $943,845 | $733,330 | 28.70% |

| Alberta | $439,319 | $362,851 | 21.10% |

| Saskatchewan | $283,900 | $256,900 | 10.50% |

| Manitoba | $335,812 | $295,518 | 13.60% |

| Ontario | $869,788 | $595,825 | 46.00% |

| Quebec | $448,601 | $338,384 | 32.60% |

| New Brunswick | $257,649 | $182,368 | 41.30% |

| Nova Scotia | $372,534 | $267,110 | 39.50% |

| PEI | $342631 | $239,070 | 43.30% |

| Newfoundland | $286,900 | $265,200 | 8.20% |

Regulators are concerned and will introduce a new stress test June 1st for uninsured mortgages where the borrower must be able to afford mortgage payments at 5.25% (up from the current 4.79%). The federal government will follow suit with the same minimum qualifying rate on insured mortgages.

I’m curious if other readers have been caught up in any crazy bidding wars, either as a buyer or seller. Let us know in the comments.

This Week’s Recap:

Earlier this week I wrote about accepting market returns and adjusting our expectations of future returns. That’s right, double-digit annual returns from a conservative portfolio is not normal.

On Young & Thrifty I wrote a comprehensive guide to Registered Retirement Savings Plans.

From the archives: Addition by subscription subtraction

Watch for new articles in the coming weeks, including an updated look inside my wallet (same $20 bill from last March), and a deep dive into BMO’s fixed income ETF line-up.

Promo of the Week:

I hate paying bank fees and so my banking “system” is set up in such a way that I avoid fees while also maximizing the interest paid on any cash on hand.

I do this by maintaining one joint chequing account at a big bank and maintaining a minimum balance to waive any monthly charges. The rest of my cash is parked at EQ Bank so it can earn interest.

It’s one of the biggest no-brainer moves to make with your money right now. The big banks pay nothing on your savings deposits. EQ Bank’s Savings Plus Account consistently offers an everyday high interest rate at or near the top of the market (currently 1.25%) with no hassles.

Open an account here and fund it with $100 within 30 days and you’ll get a $20 cash bonus for free.

Weekend Reading:

Our friends at Credit Card Genius share the best cash back credit card offers available right now.

Travel expert Barry Choi explains the best and worst loyalty programs in Canada.

There’s a lot of pent-up demand – is it time to book your post-pandemic travel? For me, yes!

Mike Moffatt explains why Ontario real estate prices keep soaring: population growth and a lack of housing supply.

Gen Y Money wants to reach financial independence early and avoid getting trapped in the sandwich generation.

Morgan Housel looks at the limits of investing sanity:

“Every few years there seems to be a declaration that markets don’t work anymore – that they’re all speculation or detached from fundamentals. But it’s always been that way. People haven’t lost their minds; they’re just searching for the boundaries of what other investors are willing to believe.”

Millionaire Teacher Andrew Hallam explains why Cathie Wood’s ARK investors aren’t making much money.

A Wealth of Common Sense blogger Ben Carlson looks at how to lose money when the stock market is at an all-time high.

My Own Advisor Mark Seed joins Tom Drake on The Maple Money Show to discuss financial independence and early retirement.

On his own blog, Mark Seed looks at whether you can retire early on a low income.

PWL Capital’s Justin Bender compares the All World ex Canada ETFs (VXC vs. XAW) in his latest investing video:

The UK blog Monevator shares a thoughtful post on the origins of our money mindsets:

“Your inner child is still trying to pull the purse strings. If you don’t notice how then you will be doomed to misunderstand money all your life.”

Of Dollars and Data blogger Nick Maggiulli looks at whether you should ever invest in a leveraged index fund?

Michael James looks back at what might have been if he mined bitcoins, never sold his Apple shares, or took a managerial role that came with stock options.

Finally, a smart look at the FIRE movement and how it’s not about retirement, it’s about independence.

Have a great weekend everyone!

A few readers have expressed concern about their recent investment performance. In most cases, these investors are holding a sensible, low cost, globally diversified portfolio of index funds ranging from conservative (40% stocks, 60% bonds) to balanced (60% stocks, 40% bonds). One reader said:

“Psychologically, it’s tough to put money in when returns have been so low.”

When you invest in a passive portfolio that tracks broad market indexes you can expect to earn market returns minus a small fee. This is far and away the best and most reliable way to invest for the long term.

But sometimes market returns can be disappointing in the short term. Investors might be experiencing that right now. In fact, if you’ve recently moved away from actively managed funds or stock picking to embrace a portfolio of passive index funds, you might be wondering if that was a wise decision.

Market returns have been dismal this year compared to returns from the previous two years. But context matters. FP Canada’s projection and assumption guidelines suggest future expected returns of approximately 4.78% per year for a global balanced portfolio.

Meanwhile, an actual global balanced portfolio represented by Vanguard’s VBAL and iShares’ XBAL returned about 15% in 2019 and 10.5% in 2020. Even a global conservative (40/60) portfolio returned about 12% in 2019 and 10% in 2020. This is highly unusual.

| ETF Name | Ticker | YTD | 2020 | 2019 |

|---|---|---|---|---|

| Vanguard Conservative ETF | VCNS | -0.82% | 9.41% | 12.10% |

| iShares Core Conservative ETF | XCNS | -0.86% | 10.33% | n/a |

| Vanguard Balanced ETF | VBAL | 1.12% | 10.24% | 14.91% |

| iShares Core Balanced ETF | XBAL | 1.41% | 10.58% | 15.19% |

| Vanguard Growth ETF | VGRO | 3.11% | 10.89% | 17.84% |

| iShares Core Growth ETF | XGRO | 3.01% | 11.42% | 17.96% |

| Vanguard Equity ETF | VEQT | 5.56% | 11.29% | n/a |

| iShares Core Equity ETF | XEQT | 4.76% | 11.71% | n/a |

A reasonable investor adjusts his or her expectations of future returns. After all, a conservative or balanced portfolio certainly won’t continue to deliver double-digit annual returns forever.

Indeed, reasonable investors should accept market returns and not fuss over short-term fluctuations or periods of underperformance.

But if your framing around index funds is about performance chasing rather than diversifying and keeping costs low then it’s going to be hard to wrap your head around accepting market returns – especially when returns have been poor.

This has been my fear all along about persuading so many investors to switch to indexing. Will they calmly stay in their seats when markets inevitably fall? Or will they panic and move on to a different strategy?

Related: Top ETFs and Model Portfolios for Canadians

Let me state this as clearly as I can.

Market fluctuations are normal. Markets fall from time to time. Often by a lot. That’s a feature of your index funds, not a bug.

If you hold an asset allocation ETF, or invest through a robo advisor, your portfolio will automatically rebalance, selling what has gone up and buying more of what’s gone down.

Investors in the accumulation stage should embrace falling prices, since they can pick up more shares with every new contribution.

To quote Warren Buffett:

“If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall.”

Final Thoughts

The strong past performance of conservative and balanced portfolios have clouded our view of what reasonable market returns look like. We’re used to double-digit gains, so now we’re upset that the return on a 50/50 balanced portfolio is flat year-to-date (it’s only May, by the way).

Ignore the urge to do something with your portfolio – like it’s an appliance that needs repair. Stick to your plan.

Impatient investors might try to juice their returns by dialing up the risk and adding more stocks. That’s a mistake. Stocks add more volatility to your portfolio, so if you’re unhappy with flat returns in the short-term, you’re going to really hate it when stocks fall by 20% or more, taking your portfolio down for the ride. See March 2020 for proof of volatility in action.

So, if you’re invested in a low cost, globally diversified, and risk appropriate portfolio, congratulations on a perfectly sensible approach. You’re not doing anything wrong. Be patient, keep adding new money regularly, and try your best to ignore daily market movements.

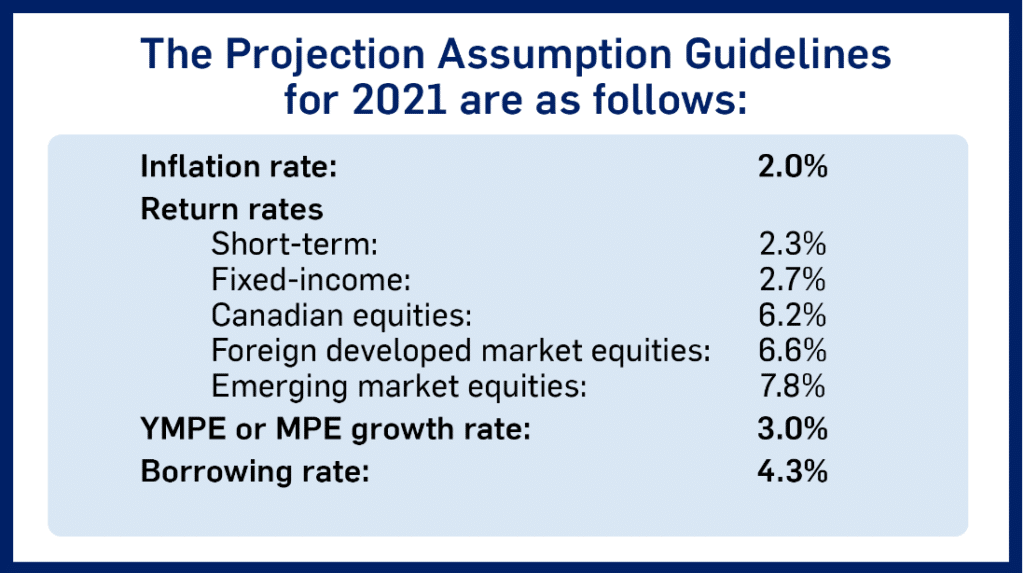

FP Canada issues guidelines every year to help financial planners make long-term financial projections for their clients that are objective and unbiased. The guidelines include assumptions to use for projected inflation and investment returns, wage growth, and borrowing rates. It also includes “probability of survival” tables that show the life expectancy at various ages.

The 2021 Projection Assumption Guidelines were of particular interest because, well, a lot has happened since the 2020 guidelines were published last spring. How should we project inflation and investment returns as we get to the other side of the pandemic and economies start opening up again?

Will we see sustained higher inflation? Should we expect any returns at all from bonds or cash? Should we lower our expectations for future stock market returns?

Remember, these are long-term projections (10+ years). That’s very different than guessing the direction of the stock market for 2021, or predicting whether we’ll see a short burst of inflation in late 2021, early 2022.

The inflation assumption of 2.0% was made by combining the assumptions from the following sources (each weighted at 25%):

- the average of the inflation assumptions for 30 years (2019 to 2048) used in the most recent QPP actuarial report

- the average of the inflation assumptions for 30 years (2019 to 2048) used in the most recent CPP actuarial report

- results of the 2020 FP Canada/IQPF survey. The reduced average was used where the highest and lowest value were removed

- current Bank of Canada target inflation rate

The result of this calculation is rounded to the nearest 0.10%

Projections for equity returns were set by combining assumptions from the following sources:

- the average of the assumptions for 30 years (2019 to 2048) used in the most recent QPP actuarial report

- the average of the assumptions for 30 years (2019 to 2048) used in the most recent CPP actuarial report

- results of the 2020 FP Canada/IQPF survey. The reduced average was used where the highest and lowest value were removed

- historic returns over the 50 years ending the previous December 31st (adjusted for inflation).

Equity return assumptions do not include fees.

Projections for short-term investments and Canadian fixed-income returns included the assumptions from QPP and CPP, the results of the 2020 FP Canada/IQPF survey, but the 50-year historical average rate was removed in 2020 as a data source. This makes sense given that interest rates were significantly higher than they are now and so it would be impossible for bonds to replicate the performance of the last 50 years.

How do you apply these investment return assumptions to your own portfolio? Let’s assume you have a balanced portfolio made up of 60% stocks and 40% bonds. Your stocks are divided up between Canadian, U.S., International, and Emerging markets. We could use Vanguard’s VBAL as a proxy:

- Canadian equities: 18% weight x 6.2% return = 1.12%

- Foreign developed market equities (includes U.S.): 37% weight x 6.6% return = 2.44%

- Emerging markets: 5% weight x 7.8% return = 0.39%

- Fixed income: 40% weight x 2.7% return = 1.08%

Total expected return from this balanced portfolio = 5.03% per year.

Subtract the MER of 0.25% and you’re left with a net expected return of 4.78% per year.

What’s interesting is how the projection assumption guidelines change over time. In 2010, the expected return for fixed income investments was 5%. In 2016 it was 4%. This year it’s 2.7%.

Projected stock returns have also been trending down, although the 2021 guidelines show modest increases for Canadian and foreign developed markets and a fairly significant increase to emerging market returns. This could simply reflect the reality that emerging markets have badly lagged the U.S. market for the past 10 years (though the same can be said for Canadian equities).

These guidelines are a helpful reminder that when it comes to our financial plan we should take a long term view of projected inflation and investment returns. The sensible approach to high stock prices is to lower your expectation of future returns, not to panic and sell while you wait for a crash that may never come. Oh, and make sure you rebalance.

This Week’s Recap:

I wrote about active versus passive investing over on the Young & Thrifty blog.

A few weeks ago I talked about revenge travel and all the pent-up demand to get away once the pandemic is behind us. I want to get ahead of the demand and book some refundable trips using my treasure trove of travel points.

We’ve tentatively booked a week-long trip to Maui in mid-October flying with WestJet and staying at an Airbnb.

And, yesterday I was thrilled to find 4 business class seats from Calgary to Rome in April using Aeroplan miles. We’ll attempt to re-create our cancelled trip from April 2020.

I am fully aware that there’s a large gap from where we are (especially here in Alberta) and where we need to be in order to safely travel. But a guy can dream, right?

Weekend Reading:

Our friends at Credit Card Genius share these last chance credit card offers – get them before they’re gone!

Budget travel expert Barry Choi compares staying at an Airbnb versus a hotel. With a family of four, I’m team Airbnb all the way.

A Wealth of Common Sense blogger Ben Carlson shares why he now leases a car instead of buying. It’s a fair argument. I just don’t care about driving the latest model and prefer not to have a car payment so I can spend more on other things I care about, like travel.

Ben Carlson also declares this the most annoying bull market of all time:

“My biggest worry is the number of young people who are witnessing meme stock gains and joke cryptocurrencies going to the moon are going to develop bad habits and attitudes about the markets that will be impossible to fix.”

Most of us want to retire on our own terms but what do you do when the decision isn’t yours?

Millionaire Teacher Andrew Hallam explains why retirees shouldn’t fear stock market volatility.

Michael James on Money takes issue with having an “explore” part to your portfolio. I agree 100%.

Another useful resource here from PWL Capital’s Justin Bender with a look at how to calculate the adjusted cost base of your asset allocation ETF:

Bender’s Ottawa colleague Ben Felix published a new white paper called, “Buy the Dip“, which looked at investing a lump sum after a market decline and compared that approach to dollar cost averaging and investing the lump sum immediately.

“While it seems appealing to “buy the dip”, the strategy implies that available capital is sitting idle while waiting for the right time to invest. This implication raises an important question about opportunity costs. Does the opportunity cost of waiting for a drop outweigh the perceived benefit of buying low?”

The results? He found that “buying the dip” is a sub-optimal strategy in both normal times and when the market appears expensive. On average, “buying the dip” trails investing a lump sum by a wide margin over 10-year periods.

My Own Advisor Mark Seed and advice-only planner Owen Winkelmolen take an in-depth look at a Millennial couple (35) who want to retire at 50.

Finally, David Rosenberg says that housing is keeping Canada’s economy going and that’s bad news when the bubble pops.

Have a great weekend, everyone!