Some industries are known for their lack of transparency – placing consumers at an incredible disadvantage. The cost of financial advice, a new vehicle, or a cell phone plan (to name a few) can vary widely and it’s not always clear if consumers are getting a fair deal.

Technology has helped balance the scales, offering real-time data and price comparisons to arm consumers with the knowledge they need to negotiate on a level playing field.

But one industry is still stuck in an outdated, predatory, and expensive model. It’s something we don’t talk about enough because the topic is taboo – the cost of dying.

Funeral expenses are the third largest expense in someone’s life, and the number one crowdfunding category. The average cost of a funeral in Canada is $10,000, a cost that is outpacing other consumer services by a landslide.

It needs to change, and consumers deserve transparency and better, more affordable options.

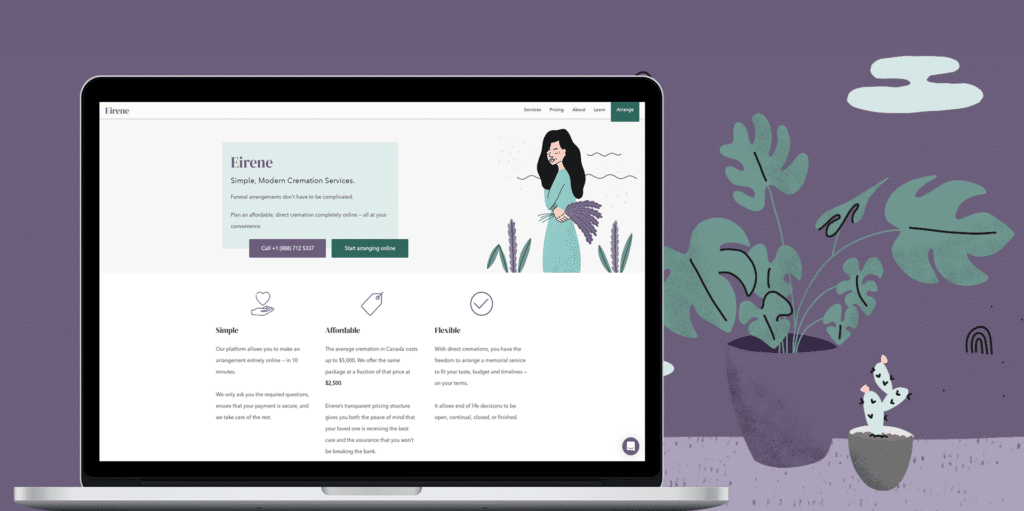

Eirene Cremations

That option is now here, thanks to a new online cremation service called Eirene. Co-founded by Mallory Greene, Eirene allows families to make a cremation arrangement entirely online — from the comfort of their own home.

There’s no shopping around, up-selling or in-person visits required. It’s the peace of mind that you’re receiving the best care for your loved one, with a focus on your experience during an incredibly difficult time.

Eirene currently operates in Southern Ontario, with a team of licensed funeral directors who are on call for you and your loved ones — whenever you need it. They are licensed and regulated by the Bereavement Authority of Ontario, and their industry partners are licensed and vetted to deliver the best service to you.

I had the chance to interview Ms. Greene about Eirene and how it’s disrupting the funeral industry.

Q1). Why did you decide to enter the business of arranging funerals?

MG: This is the first question I get when I share Eirene. Previously, I worked at Wealthsimple as part of their founding team. I worked on everything from marketing to HR to communications. I had an incredible experience there, learning how to build a business from the ground up and create something that could positively impact people’s lives.

But despite the fact that my background has been working in financial technology, I am the daughter of a funeral director. So, unlike most people, death and the conversation around end-of-life has been a massive part of my upbringing and identity. I felt that I was in a unique position to combine my love for technology with my knowledge in an industry that desperately needed transparency and education.

Surprisingly, there are many similarities between the funeral and the financial industry. When Wealthsimple first launched, talking about money was still relatively uncommon. Wealthsimple focused on the accessibility of their product, empowered people to take control of important decisions, and helped them plan for the future. And that’s exactly what I want to do at Eirene in the death-care space.

Q2). Arranging a funeral can be expensive and complicated. How does Eirene change this experience?

MG: At Eirene, we’re focused on providing a better experience to families during an incredibly difficult time.

The traditional process of arranging a funeral is time-consuming and overwhelming. Since many of us aren’t thinking or planning for end-of-life, when a death occurs, we are shocked by the price of funerals and the amount of paperwork. And, keep in mind, this is all while dealing with the death of a loved-one.

Eirene was many years in the making, and after a lot of in-depth research, we discovered that three critical factors needed to exist to create a better experience for families.

Simplicity: The arrangement process is made simple for families during a challenging time. You don’t have to walk into a funeral home and fill out endless paperwork. You can simply go online, enter the required details, and we will handle the rest.

Affordability: Pricing in the funeral industry is opaque, recently highlighted in the most recent Auditor General’s report. It can vary drastically between providers, and pricing that you see on a funeral website’s home page is often not what you end up paying. Eirene offers all-inclusive pricing to ensure that there are no surprise bills or hidden fees.

Transparency: Eirene was founded to bring transparency to the funeral industry and provide education to consumers. We know the importance of planning for major milestones, including end-of-life. We provide free tools and resources to families across Canada to make the best decisions for themselves and their families, whether they use our services or not.

Q3). What is the cost of a typical funeral, and how much does Eirene charge for a similar service?

MG: The average Canadian pays $5,000 for a cremation, with a traditional funeral costing upwards of $20,000. The cost can drastically range, because of the complexity of package pricing, so comparing funeral homes can be quite tricky.

Unfortunately, funeral costs are often a sticker shock to many, which is why funeral fundraising is the fastest-growing crowdfunding campaign category. Many people can simply not afford to die.

At Eirene, we believe that everyone should access affordable, dignified death care, no matter their financial circumstance. We have one cremation package price of $2,500 plus tax. This includes everything you would need to ensure the highest quality of care for the person you love without worrying about finances.

Our package includes the transfer, storage and cremation of your loved one, including hand-delivery of their remains. We also provide 24/7 support from our team of licensed funeral directors, help with all government-related paperwork, and give you access to estate administration tools to help you close accounts, notify the government and credit bureaus.

People often ask how we keep our costs low and wonder if it means their loved one will get a different level of care. The simple answer is that we do not carry the same overhead that a funeral home would because we are a technology business.

This means that we can pass on savings to the families who choose Eirene. It’s the same standard of care that you expect from a funeral home, but at an affordable cost to everyone.

Q4). You help clients plan a direct cremation online. More Canadians are choosing cremation versus a traditional burial. Can you talk about that growing trend and give some insight into why this might be happening?

MG: In the past few years, there have been significant shifts in how people think and plan for end-of-life. They’re creating more individualistic, less traditional ceremonies and seeking to commemorate people in unique ways.

It seems that more Canadians are moving towards cremation because of the price, flexibility and simplicity of the process. Some families have a limited budget that they cannot exceed. That, however, is not the case for everyone. For others, it’s about spending money in a way that makes sense to them. They would rather put the money towards a memorial service or find a beautiful way to memorialize their loved one.

Related: 4 end-of-life strategies your survivors will thank you for

Beyond price, the process of cremation is a straightforward task at the time of passing. There are fewer immediate decisions to make, which eases the process for grieving families. Often, they feel that there is more flexibility and time given to them. You can let remains go that day, or you can have them for six years, sixty years, or pass them on to future generations. You can host a memorial service a year later, scatter the remains at your favourite location or turn them into a diamond. The options are quite endless.

Q5). Your direct cremation service takes care of funeral arrangements from start to finish. Is there anything you can’t (or won’t) do?

MG: As mentioned above, our cremation package includes everything you would need to ensure that your loved one is taken care of and you receive support during a difficult time. We are hyper-focused on supporting families through the tasks that need to be completed immediately following a death. We don’t currently offer any burial or memorial services.

Beyond that, our resources and blog aim to help Canadians find the right providers and services based on their preferences. As we grow, we will expand our offerings and connect families to vetted partners to help them through various end-of-life stages.

We’re starting with a cremation package, as that’s what over 72% of Canadians choose today, but we know that there are many other options that families are seeking.

Q6). Eirene is currently serving Southern Ontario. What are your plans for expanding this service?

MG: We started in the Greater Toronto Area and recently expanded our offering to families across Southern Ontario. We see a real need for our business, and we hope to continue to grow throughout Canada.

Beyond our expansion news, we are launching a pre-need funeral insurance product very soon, an option for families to pre-pay for their funeral package at Eirene. It’s a way for families to put their funeral wishes in writing and alleviate the financial burden at the time of death.

You can sign up for the waitlist here.

Lastly, I’m inspired by the idea of introducing new methods of dispositions, especially those that are environmentally friendly. We are looking forward to expanding our offerings and helping families memorialize their loved ones in unique, new ways.

Final Thoughts

Technology is disrupting industries all around us. Robo advisors offer low cost, evidence-based investing on the cheap. Consumers have access to free credit scores and affordable borrowing options. Rate comparison sites can scan the market to tell us where to find the lowest mortgage rates, or the highest savings account rate. You can even create a Will online.

Yet here we are in 2021, still visiting a funeral home in-person, grieving and armed with practically zero knowledge about the cost of a cremation or burial.

Thankfully, a service like Eirene is now available to shine a light on the cost of dying and help Canadians plan and arrange an affordable cremation online.

Boomer & Echo readers can receive $250 off their package when planning a funeral arrangement online with Eirene.

This year is going to be one of the strangest and (potentially) most complicated years for tax filing. Jobs were lost and hours cut during the pandemic. The federal government responded by introducing the Canada Emergency Response Benefit (CERB) and the Canada Emergency Wage Subsidy (CEWS), among a host of other measures to protect workers and the economy. Furthermore, many entrepreneurial-minded Canadians turned to side hustles and the gig economy to earn more income.

CERB payments are taxable, but taxes were not withheld at the source. Eligibility for self-employed individuals was not clear from the onset, and the CRA has sent out letters asking to confirm eligibility or risk having to pay back benefits.

All of this to say that many Canadians are nervous about filing taxes for the 2020 year. Self-employed individuals, in particular, need assurance to help understand all of the tax deductions and credits that are available to them.

Think of the deduction for home office expenses. Many of us found ourselves unexpectedly working from home, setting up shop in our kitchen, living room, or bedroom. Because of this, the CRA announced it had simplified the way employees can claim home office expenses on their tax return for the 2020 tax year.

Navigating your way through all of the eligible tax credits and deductions can be painful on your own. That’s why tax services like TurboTax are essential for tax filers – especially the self-employed – to find every available deduction and maximize your return, giving you a little lift when you need it most.

I’m amazed at how intuitive these programs have become. Not just the service, but TurboTax has an entire team of tax experts with an average of 10 years of experience at the ready to answer your questions in real time and can even fill and file your return for you.

TurboTax is NETFILE certified and can guarantee you’ll get your biggest refund. NETFILE is the CRA’s online filing service and it allows you to electronically submit your tax return directly to the CRA from your computer.

Before I get into the features of the TurboTax Full Service Self-Employed product, I have a confession to make. Ten years ago, I hired an accountant to incorporate our online business and to figure out the most tax efficient way to treat our business income, retained earnings, and how to withdraw money from the corporation when needed.

I figured once the corporation was set up and we were pointed in the right direction, I would go back to filing my own taxes, both personal and small business.

What I (surprisingly) discovered was that I found great value in paying for tax advice and having a professional take care of our tax filings. That’s right, a personal finance expert pays someone else to do his taxes! Here’s why:

Our situation is more complicated than most. When I worked a full-time job, we were able to stream dividends to my stay-at-home wife to help accelerate our savings goals. Since then, we created a meaningful role for my wife which helped grow the business and stay on-side of the new TOSI (tax on split income) rules. I opened a corporate investment account to invest our retained earnings. Finally, after I quit my day job, we needed advice on whether to pay ourselves a salary or continue to pay dividends.

Your situation might not be overly complicated, but you can still benefit from having sound advice from a tax expert to help make this year’s tax season less stressful than it has to be.

This speaks to the need to have a tax expert on your side. Thankfully, TurboTax continues to make tax filing easy for all Canadians, even self-employed individuals, with their Self-Employed suite of products.

I got to test-drive TurboTax Live Full Service Self-Employed earlier this month to see how TurboTax gives a little lift to self-employed tax filers.

TurboTax Self Employed

I empathize with small business owners and self-employed Canadians who have more complicated tax situations than simply submitting a T4 along with an RRSP contribution. It’s not easy to file your own taxes and know (with confidence) that you’re claiming all of the expenses and getting all of the deductions that apply to you.

And I get it. Not everyone can afford to (or will even have the desire to) pay an accountant to file their tax return and get tax advice every year. But you’re not alone.

TurboTax Self-Employed offers three ways for self-employed individuals to file their taxes.

- Self-Employed (do it yourself) – You complete your own return, and TurboTax will guide you through the process.

- Assist & Review Self-Employed – Get tax advice and a final review of your return from an expert.

- Full Service Self-Employed – TurboTax Live Experts can prepare, optimize, and file your taxes for you.

Seasoned self-employed individuals with a good understanding of their expenses and deductions can file confidently on their own with TurboTax Self-Employed.

Newly self-employed individuals, or those with more complicated situations, might want the assurance of TurboTax Assist & Review Self-Employed. You’ll get access to a team of experts who will listen to and understand your unique situation, answer your questions, give you unlimited tax advice, and, of course, give you the little lift of the best possible tax outcome when you file.

For TurboTax Self-Employed and TurboTax Assist & Review Self-Employed, a business interview guides you through filing your self-employed income and expenses and automatically finds relevant deductions.

TurboTax Self-Employed Full Service

Those looking to free up more time might want to hand off their taxes to a TurboTax Live Full Service Self-Employed tax expert. I tested out this product and came away impressed with the seamless, intuitive, and time-saving process.

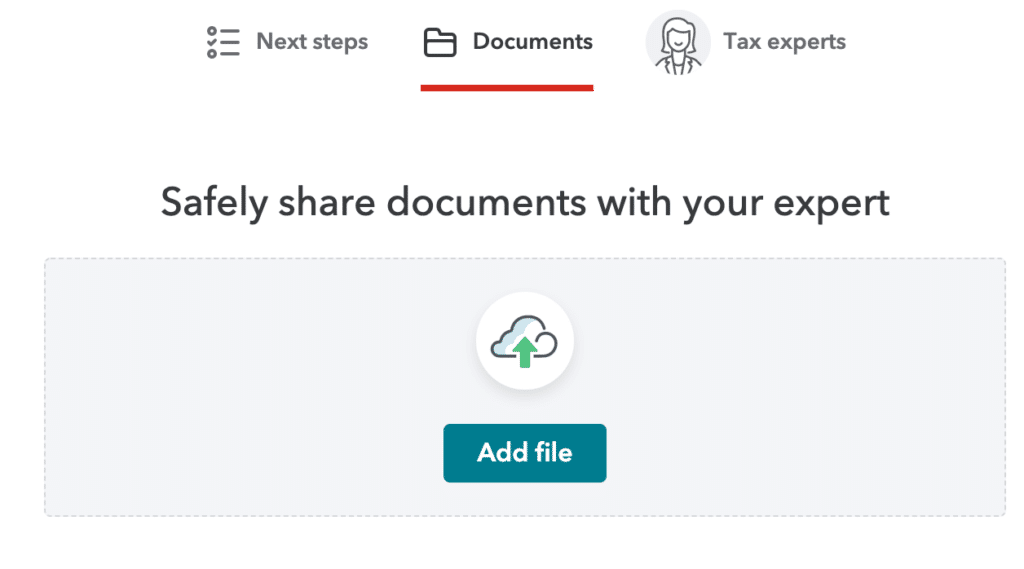

Get started by signing up and completing your profile and granting TurboTax authorization with the CRA. Your TurboTax tax expert will get your documents directly from the CRA and start working on your return. They’ll make sure you get every deduction and notify you when it’s ready for a joint review.

If you’re busy like me, you’ll appreciate that you can schedule time to connect with a tax expert to go through and review your return over the phone at a time that suits you. I was able to connect with my assigned expert, Claire, immediately, but there is an option to schedule a call at your convenience. The call is done through a one-way video call (you can see them, but they can’t see you) and from there, your tax return is filed online to the CRA by a tax expert, and you get a notification that it’s been submitted.

In the documents section I was able to upload all of my relevant files, download anything that Claire sent me to fill out, and upload it again as requested.

Any communication with your tax expert is done through the ‘Tax Experts’ tab. Enter your questions here and your tax expert will respond. The messaging system will keep track of your communication history and you will be notified by email when your expert replies.

Although you could get it all done in a day, the entire process took a few days for me due to some back-and-forth messaging and uploading of files. Email notifications were an efficient way to keep the process moving along. It was really no different than going back and forth with an accountant – and I did it all from my living room.

What makes TurboTax Self-Employed Full Service different?

Full-service customers can get year-round tax advice, tailored for their unique tax situation. Audit Defence puts a tax expert in your corner, who will represent you, defend you, and handle all correspondence with the CRA on your behalf.

You get this service as a part of your purchase, so you know someone has your back, even after they’ve submitted your tax return.

Finally, at $199.99 per return, you’re paying a fraction of the cost of using an accountant (start for free, only pay when you file). You’ll still get your taxes filed by a real tax expert who will make sure you get back every dollar you deserve. And you’ll save yourself a boatload of time.

Final Thoughts

With tax season right around the corner, many Canadians are understandably nervous about filing this year. For self-employed individuals, it can be painful trying to navigate your way through all of the various expenses, credits, and deductions available to you – especially if you’re a new self-employed tax filer or if your situation changed last year due to the pandemic.

TurboTax Self-Employed has three options for self-employed tax filers to choose from to ensure they get the biggest tax refund possible by taking advantage of all available deductions and credits. In these uncertain times, these are the little lifts we all need.

Save time, save money, and file your self-employment taxes with confidence by getting started with TurboTax Self Employed.

TurboTax has kindly provided me with four unique (and FREE) product codes to try any of the three TurboTax Self-Employed products. Leave a comment below to enter to win a free product code and try out the service for yourself this tax season.

This post was sponsored by TurboTax Canada. All opinions and experiences are my own.

I began my career as a young sales manager in the hospitality industry and earned an annual salary of $26,000. Little did I know at the time that my human capital – as in, the present value of my expected future income throughout my working lifetime – would be worth nearly $3,000,000!

I recently did some back-of-the-napkin calculations and was surprised to learn that I had already earned $1.4 million dollars over an 18-year career. I found that incredible, given that I had never earned a six-figure salary and, my wages had been stagnant for several years.

Projecting my income forward using a modest 3% annual growth rate revealed the potential to earn another ~$1.6 million by the time I turn 55.

Human Capital vs. Financial Capital

Put in different terms, however, and you can see that my human capital is shrinking each year. That’s because the value of my human capital peaked the day I started my career (back in 2003) with my entire lifetime of earnings ahead of me. Since then I’ve steadily used up my earning power and the value of my human capital has gradually declined.

The idea of eroding capital doesn’t sit well with me, but that’s where the second form of wealth building – your financial capital – comes into play. See, I’ve been a diligent saver for most of my career, which means converting my human capital (earnings) into financial capital (investments).

Now at the age of 41, I’ve managed to turn $1.4 million of human capital into long-term savings, or financial capital, of nearly $700,000 (ignoring the equity in our home).

I can estimate my financial capital into the future by adding my annual savings rate and multiplying it by the expected rate of return on my investments. So when I do that projection I add annual savings of $18,000 to my existing financial capital and multiply that by an expected 6% return on investment. The result?

By age 55 I’ll have converted $3 million worth of human capital into more than $1.8 million in financial capital.

Interestingly, the two forms of wealth building don’t intersect until age 48 – the point when I’ll have about $1M worth of human capital left (assuming age 55 retirement) and my financial capital eclipses the $1.1M mark.

Is Your Career a Stock or a Bond?

Another way to look at the concept of human capital vs. financial capital is to determine the volatility of your career. A teacher or civil servant likely has rock-solid job security and a relatively known earnings schedule throughout their working lifetime. Their human capital could be considered more bond-like, meaning they can likely afford to invest more of their financial capital in riskier assets like stocks.

Contrast this with someone that works in a boom-or-bust industry like oil & gas, or whose income relies mainly on commissions and bonuses. Their human capital could be considered more stock-like and therefore they can ill-afford to take on much risk in their financial capital and should hold more cash and guaranteed investments to hedge against a volatile profession.

You also can’t discuss human capital without talking about protecting your lifetime earnings with disability insurance, whether that’s through your employer, a private plan, or some combination of the two. One-third of working Canadians will experience a period of disability lasting longer than 90 days during their working lives.

Final thoughts

The concept of human capital is interesting when you consider your lifetime earnings and how to convert that into financial capital to fund your retirement years.

You begin your career with perhaps several million in human capital and likely nothing in financial capital. The goal is for the two to intersect at some point during your working life, hopefully early enough so that your financial capital can provide you with your desired lifestyle in retirement.

$3 million sounds like a LOT of money to earn in a lifetime. But here’s the thing: if you don’t convert even a small portion of your earnings into financial capital then your human capital will eventually run out and you’ll end up with nothing.

As Charles Dickens once said,

“Annual income twenty pounds, annual expenditure nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pound ought and six, result misery.”