Stock markets around the world continue to climb higher after bottoming out on March 23. In what seems like ages ago, markets fell harder and faster than ever before as the world grappled with a global pandemic and stay-at-home orders.

The TSX, as represented by iShares XIU, fell more than 32%, while the S&P 500 (represented by iShares XUS) fell more than 22%. Since then, global markets have steadily recovered and XUS is down just 1.04% on the year while XIU is down a relatively modest 11.5%.

Some people are not happy about this. One article reported that billionaires got $434 billion richer during the pandemic – an absurd claim that ignores the stock market crash leading up to March 23.

Another article claimed that bored day traders were ‘stupidly‘ playing the markets during these uncertain times and are going to ‘get played’ because economic conditions are only going to get worse. That may be true, and I recently wrote about the pitfalls of commission-free trading, but let’s dig into the reasons why this article makes no sense:

1.) The stock market is not the economy. Yes, it may seem strange to see markets rising at a time when economic and employment data is incredibly depressing. But the stock market is forward looking and based on expectations.

Collectively, investors know how bad things are. That’s why markets fell so hard and so fast in March. But it also has some baked-in expectations of both the present and the future. As long as those expectations are met (as bad as they are) there’s no reason to think markets can’t continue to trend higher.

Besides, look at the strength of the five largest companies in the U.S. (Microsoft, Apple, Amazon, Alphabet and Facebook), which continue to thrive and now account for one-fifth of the market value of the index.

However you look at it, historically the linkage between the stock market and the economy is actually pretty weak.

2.) The future is always uncertain. Cynics argue that we shouldn’t invest in these ‘uncertain times’, as if there’s ever a time when the present and future are certain and predictable.

Investing has always been about believing in the power of human ingenuity and progress over time. So even though the cause of this crisis is different than the 2008 financial crisis, or the 1929 great depression, we’ve always found a way to persevere and reach new heights.

If you truly believe this time is different then we have bigger problems to worry about than where to invest our money.

No one knows which way markets will go in the short term. But with history as our guide we know the long term trajectory points up and so it’s best to stay invested.

3.) Young traders with $1,000 accounts aren’t moving the market. Yes, many young investors are going to lose money betting on stocks in their new commission-free brokerage accounts. But young investors have always done this, from the dot com era through the financial crisis. Call it a rite of passage for some investors who believe they can strike it rich investing in the latest fad, from tech stocks, to cryptocurrency, to cannabis stocks, and now (apparently) pharmaceuticals.

Betting on individual stocks is not a smart strategy, period. But it’s not any more stupid today than it was 10 or 20 years ago. In some cases the best thing to happen to these young traders is a quick loss and a lesson learned. A worse outcome might be a series of winning bets, which will lead to overconfidence and misjudging their decision to be good thanks to a favourable result.

This Week’s Recap:

I was please to once again collaborate with a panel of experts to select the top ETFs in 2020 for MoneySense. The list expanded to 42 ETFs (out of 800), but include a lot of overlap such as the asset allocation funds offered by Vanguard, iShares, and BMO.

I managed one post this week, with a list of five investing rules to follow in good time and bad. I’m kicking myself for not including a sixth rule: simplify.

I’ve answered countless reader questions in the last few months about asset allocation, asset location, tax efficiency, U.S.-listed ETFs, Norbert’s Gambit, and comparing similar ETFs across different providers. Most of that stuff doesn’t matter, or at the very least will only improve things at the margins.

To be clear, if you’ve decided on a passive indexing approach then you’re already 90% of the way there. Investors can drive themselves crazy tripping over every decision to fine-tune and optimize their portfolios.

Try this approach instead. Decide between paying slightly more for a hands-off, automatic investing solution (robo advisor), or a lower cost DIY solution (asset allocation ETF through a discount brokerage account).

I’ve seen way too many investors end up with decision fatigue, analysis paralysis, and complexity regret by trying to build and manage their own portfolio of multiple ETFs in each account.

Keep it simple and opt for a fixed asset allocation across all accounts. You can do that easily today by purchasing an asset allocation ETF like VBAL or VGRO in each of your RRSP, TFSA, Individual account, etc. No need to get any more complicated than that.

Weekend Reading:

I mentioned recently how I’ve shifted our credit card rewards strategy to focus more on cash back and free groceries. On that subject, here’s a great look at how to maximize your PC Optimum Rewards.

Wondering when Canadians can start travelling again? CBC’s Sophia Harris shares everything you need to know about travel and travel insurance.

Millionaire Teacher Andrew Hallam has been absolutely killing it lately with his writing. I loved this piece about Netflix and Amazon investors going crazy:

Five burley men stormed my home. They dragged me by the hair to my laptop (I often dream about having hair). The biggest guy’s name was Jeff. He screamed, “Log in to your brokerage account! Sell everything! Then invest the entire proceeds into Netflix and Amazon shares! And if you try to sell them before ten years are up, we’ll come back for your scalp!”

Real estate pricing forecasts are all over the map, with experts predicting everything from a rise of 12% to a drop of 30%.

Half Banked blogger Des Odjick says voting with your dollars has never mattered more. I agree 100%. Like Des, we’re also supporting our favourite local businesses and have even created a nice Friday night tradition of take-out and a virtual wine-tasting while our kids watch a movie.

Behavioural economist Richard Thaler says the law of supply and demand should have eliminated any shortages at the grocery store but it failed to account for one thing: it’s not fair to raise prices in an emergency.

Of Dollars and Data blogger Nick Magiulli explains why failed predictions don’t matter.

The Ritholtz Wealth Management team share their 10 rules for retirement investing:

Do you and your spouse build in some ‘no questions asked’ spending money in your budget? We do. This Pocket Worthy blogger explains how a $500 monthly allowance saved her marriage.

My Own Advisor Mark Seed shares a detailed look into his quest for financial freedom. Well done, Mark!

The Globe and Mail’s Tim Cestnick shares some questions every cottage owner needs to answer.

Here’s an incredible and heartbreaking story from Morgan Housel on the three sides of risk.

Finally, an inside look into King Arthur Flour, the company supplying America’s sudden baking obsession.

Have a great weekend, everyone!

When it comes to money, no one has it completely figured out. We can learn a lot from our own failures and from the mistakes of others. Stories like the one shared by Kind Wealth founder David O’Leary – who filed for bankruptcy at age 25 – highlight the fact that no matter who we are, we’ve all made a mistake or two with our finances. There’s no shame in admitting it, and by sharing our financial failures we can help others avoid potential pitfalls in their own lives.

Humble Dollar blogger Richard Quinn fessed up to 10 big financial mistakes in a recent column, from betting on penny stocks in his late teens, to selling investments at a loss to buy an engagement ring, to borrowing from his retirement account to pay for his kids’ college education. Despite his many money failings, Mr. Quinn still managed to retire comfortably – something he attributes to working for the same company his entire career.

I’ve shared plenty of my own financial mistakes in this blog. I started investing in an RRSP at age 19 when I was earning less than $25,000 per year and still had student loan and credit card debt. I had to cash out my RRSP to pay off my maxed-out credit card.

I got in over my head as a first time home buyer and needed a roommate to help pay the mortgage. When he moved out I once again turned to my credit card to cover my monthly shortfall. Not smart.

I took out a second mortgage – basically a consolidation loan – to pay my high interest debt and clean up my act. Thankfully, it worked.

I bought mortgage life insurance once. Never again.

My investing journey began with high fee mutual funds (I’ll take a pass since it came with an employer-match), turned DIY when I decided to pick individual dividend stocks, before finally coming to my senses and switching to index investing.

I’m still making mistakes and learning as I go. I quit my job last December to focus full-time on writing and financial planning. It was the best decision I’ve ever made for my career and for my family, but now I regret not doing it sooner.

What are some of your financial mistakes? Share them in the comments below.

This Week’s Recap:

I managed one post this week, opening up the Money Bag to answer reader questions about bonds behaving badly, investing USD, active management in a market crash, and how I’m handling my credit card rewards and loyalty points.

In other news, I’ve opened a corporate investment account at Questrade. If you recall, I received an excess cash payout from my pension which means I won’t have to take out any money from our business this year.

My plan is to keep a cash balance of six months worth of projected 2021 expenses (when we will resume paying ourselves), and then invest any remaining funds.

Finally, many thanks to Rob Carrick for including my article on renewing your mortgage in his latest Carrick On Money newsletter.

Weekend Reading:

Credit Card Genius compares five digital wallets and explains why they’re safer than your physical wallet.

A Wealth of Common Sense blogger Ben Carlson describes the five types of investors in this market. Which one are you?

Warren Buffett says he’d disagree violently with the notion that passive investing is dead.

The federal government announced this week that seniors who qualify for OAS will be eligible for a one-time, tax-free payment of $300, and those eligible for the GIS will get an extra $200.

Rob Carrick says seniors deserve help with expenses in the pandemic, but investment losses is another matter:

“It’s not the job of government to backstop individual investing losses. If anyone loses money in the stock market, that’s on them.”

Meanwhile, parents are in financial limbo after spending thousands on sports, arts, and summer camps that have been derailed by COVID-19. Our kids are finishing up their ballet and piano lessons online with Zoom and Skype, respectively. We hadn’t committed to any summer camps because we thought we’d be travelling in the U.K.

Here’s a very good and relevant piece from Jonathan Chevreau on whether retirees should reduce their RRIF payments during COVID-19. The government gave RRIF holders the option to withdraw 25% less than their minimum mandatory withdrawal rate this year.

PWL Capital’s Ben Felix digs into the 4 percent rule in his latest video on how to retire early:

Millionaire Teacher Andrew Hallam shares a stellar post on why Canadians are wasting billions on currency-hedged ETFs.

Michael James reviews the financial documentary, Playing with F.I.R.E. I watched it last week and really enjoyed it as well.

Erica Alini of Global News looks at coronavirus and the housing market, and asks if it’s a good time to buy.

Finally, here’s travel expert Barry Choi on what the future of travel may look like.

Have a great weekend, everyone!

Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

This edition of the Money Bag answers your questions about bonds behaving badly, investing USD cash in a TFSA, active management during a market crash, and how I’m managing my credit card rewards points.

First up is Wendy, who wants to know why her bond cushion didn’t do the job she expected it to do during the market crash. Take it away, Wendy:

Bond Cushion Not Working

Hi Robb,

I am in my early 60s and a regular reader and fan of your blog. I hold bond ETFs in my portfolio, along with some equity ETFs. The 30+% recent drop in portfolio value certainly made me flinch but I never once consider selling. I’m a firm believer in index investing and holding to my plan for the long-term.

However, the bonds have not done the job I’ve expected them to do. Even before the pandemic, my bond holdings have been in the “red”.

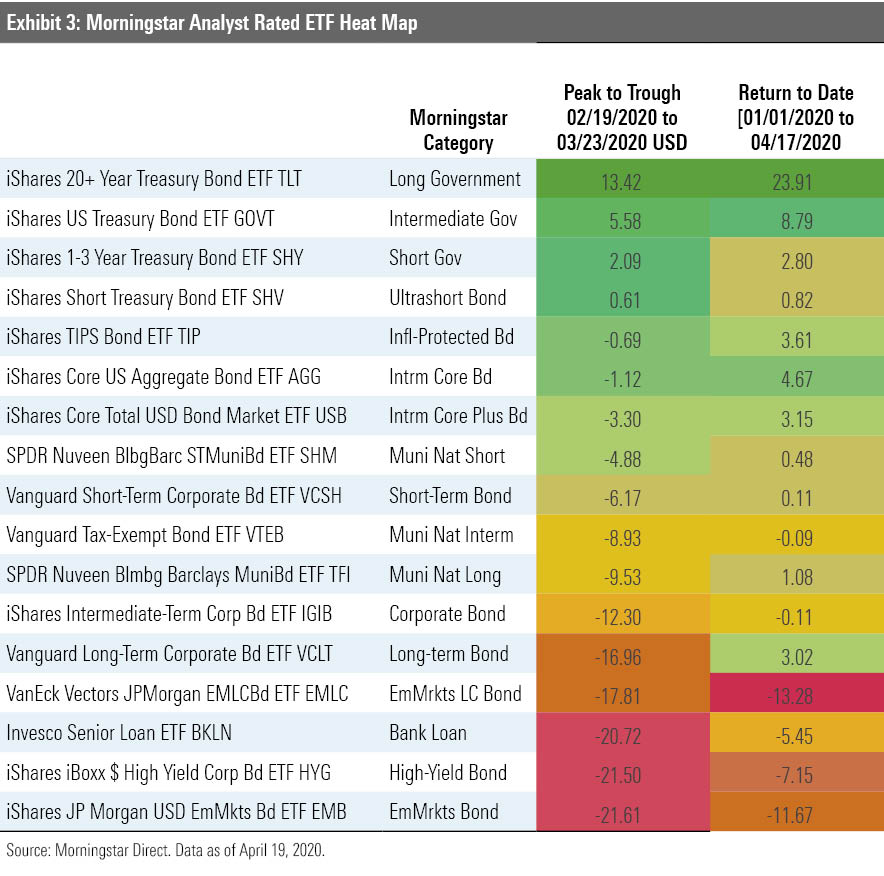

I hold ZCS in my RRIF, which has performed okay with only +/-5% difference, nothing to quibble about. But I also hold ZHY and ZEF in my TFSA. Today they are down -18.4% and -13.9% respectively, twice that a few weeks ago and more than ZLB at -13.28!

Why have the High Yield US and Emerging Market bonds done so poorly since I bought them in 2017?

Hi Wendy,

Corporate bonds can behave much differently than government bonds because they are much riskier assets. Especially ‘high yield’ bonds like ZHY – high yield typically means riskier debt has been issued by companies with not so stellar balance sheets. These bonds took a massive hit during the pandemic as investors flocked to the safety of government bonds.

A more diversified bond ETF like VAB (Canadian aggregate bonds) did much better throughout the crisis, with a return of 2.95% YTD. Here’s a better look at what has happened in the bond market during the coronavirus crisis:

During a crisis, investors look for safe-havens and the bonds issued by the U.S. Treasury Department are backed in full faith by the U.S. government and therefore free from any credit risk. That’s why long-and-medium-term U.S. treasury bonds performed so well, while high yield corporate bonds and emerging market bonds got hammered.

As for what to do, I find investors often get trapped in thinking they’ll just wait for their initial investment to “recover” before selling and switching strategies. But, I’d re-frame that thinking and consider if you had that money sitting in cash right now, would you invest it in the high yield bond funds or would you invest it in something else that had a higher expected rate of return and/or was better aligned with your investment strategy?

Investing USD Cash in a TFSA

Next up is Martha, who wants some advice on how to invest the USD cash in her TFSA:

Hello Robb,

My TFSA contributions are maxed out and is comprised of CAD $52,000 (invested in the Canadian Portfolio Manager Ridiculous Portfolio of 80% stocks / 20% bonds) and USD $16,500 cash.

I don’t want to convert this USD to CAD just yet, but rather prefer to grow it somehow. Do you have any suggestions on specific Canadian listed USD ETFs, GICs or bonds that would be suitable to park my USD?

I put this into my TFSA because of the tax-free nature of the account and all the gains/interest coming back to me. I say Canadian listed because of the foreign withholding taxes eating away at my portfolio. I’m still a newbie to the DIY investing and have to move forward from analysis paralysis.

Hi Martha, thanks for your email. So, I think there are couple of points to clarify here:

1.) There is no such thing as a Canadian-listed USD ETF. There are U.S.-listed ETFs that you can buy with U.S. dollars – such as Vanguard’s VOO, which tracks the S&P 500. And there are also Canadian-listed ETFs that track U.S. or International indexes, such as Vanguard’s VFV, which also tracks the S&P 500. You buy these ETFs with Canadian dollars.

2.) There is no real advantage to investing in U.S.-listed ETFs inside your TFSA. They’re more advantageous, tax-wise, to use inside your RRSP. That’s because you cannot avoid foreign withholding taxes in your TFSA – they’re unrecoverable because the TFSA is not recognized as a retirement account by the U.S.

Since the exchange rate is quite favourable right now (1 USD = 1.41 CAD) why not convert that money to CAD and then just buy one or more of the Canadian-listed ETFs that Justin Bender outlined for TFSAs in his ridiculous model portfolio?

Finally, if you’re still new to this I’d highly recommend keeping things extremely simple with the one-ETF asset allocation ETF like I’ve outlined in my top ETFs and model portfolios.

I’ve seen a number of investors struggle with more complicated portfolios that look great on a spreadsheet but once put into practice become unwieldy to manage on their own. Heck, I consider myself an expert and I just invest in one ETF – VEQT.

Active Management in a Market Crash

Jason wants to know if there’s any merit to the argument that active management can perform better during a bear market:

Hi Robb,

I am a DIY ETF investor and recently had an investment advisor contact me about the value of professional advice. He said in markets like this, where there is a dichotomy between those companies / sectors doing well and those doing poorly, index ETF investors are missing out on active management. How do you respond to that argument?

Hi Jason, thanks for your email. If the advisor is talking about adding value through active management and market timing then you should run the other way.

No one could have predicted with any degree of certainty which stocks would fall and which stocks would perform well. Anyone who claims they can is doing so with extreme hindsight bias (of course Clorox would be up 25%, who didn’t see that coming?)

As far as I’m concerned, investing has been solved. Low cost, broadly diversified index ETFs are the best choice for long-term investors. Gone are the days when advisors can claim to add value by picking winning stocks and timing the market.

Where an advisor can add value is in financial planning, tax management, estate and legacy planning, psychology, accountability, prioritizing short-and-long-term goals, etc.

The bottom line is that investors shouldn’t change strategies based on market conditions. Period.

Have You Changed Your Approach To Credit Card Rewards?

Finally, Amit wants to know if I’ve changed my approach to credit card rewards during these stay-at-home times:

Hi Robb, you’ve written a lot about credit card rewards and travel rewards in particular. Now that we can’t travel for the foreseeable future are you doing anything different with your current credit cards and rewards points?

Hi Amit, it’s a tough time for credit card rewards junkies like myself. For one, we planned to do a heck of a lot of travel this year and take advantage of programs like Aeroplan, Marriott Bonvoy, American Express Membership Rewards, and WestJet Dollars. Not to mention all the perks that come with those programs, like free hotel nights and upgrades, airport lounge passes, and companion travel vouchers.

With our trip to Italy cancelled and our trip to the U.K. likely to cancel next, we’ve got an abundance of travel rewards points and nowhere to use them.

- Aeroplan – 560,000 miles

- Marriott Bonvoy – 136,000 points + 3 free nights

- American Express Membership Rewards – 220,000 points

- WestJet Dollars – $637 + 2 companion travel vouchers

My typical advice is to use your points fairly quickly and not hoard them. Loyalty programs often get devalued and expiry policies can also change at any time. However, in These Times, I believe the major credit card rewards programs and loyalty programs will want to hold onto their members for when we can return to travelling again. Marriott, for example, extended its free night certificates to no longer expire within a year.

Besides hanging onto my travel rewards points, I’ve made the switch to a cash back credit card and have been using the Scotia Momentum Visa Infinite card for everyday purchases like groceries (and MORE groceries). I figured cash back would be more useful in the short-term, and this card had a 10% cash back bonus for spending in the first 3 months. Not bad!

I also use instant-reward programs like PC Optimum and Air Miles Cash to get a quick $10 off a grocery purchase – which comes in handy during a pandemic.

Do you have a money-related question for me? Hit me up in the comments below or send me an email.