It’s no secret that mortgage rates have been incredibly low for an incredibly long time. Even when we think rates couldn’t possibly go lower, a lender tests the waters with another record-low promotion. This time it’s HSBC with an unprecedented 5-year fixed mortgage rate of 1.99%.

But as mortgage broker Dave Larock points out, there’s more for borrowers to consider than just interest rate alone. With HSBC’s offer, for example, the mortgage must be a high-ratio mortgage (less than 20% down so that it comes with borrower-paid mortgage default insurance).

Cheap mortgage rates also tend to come with less flexible terms. That means you may not enjoy the same pre-payment privileges (allowable annual lump sum payments, and double-up monthly payments) as you would with a different mortgage provider.

More importantly, as Mr. Larock points out, five-year fixed rate mortgage terms can be expensive to break if the borrower wants to refinance or is forced to sell their home. He says if a borrower needed to get out of the HSBC 1.99% five-year term after just two years, they’d be charged a penalty of $23,000.

A more flexible lender, in Mr. Larock’s example, currently offers a five-year fixed rate term at 2.13% and would only charge a penalty of $2,000 to break the mortgage after two years.

On the surface, a borrower would save $2,612 over five years by choosing the HSBC 1.99% rate. But is that worth giving up the flexibility (and potentially punitive penalty) of breaking the mortgage at some point in the next five years?

Borrowers by and large prefer five-year fixed rate mortgage terms, often to their detriment. Consider that an estimated 68% of mortgage holders choose a five-year fixed rate term, but more than 60% of mortgages will be paid out or restructured within 36 months. Don’t be one of these all-too-often told news stories about a borrower being forced to pay an obscene amount to break their mortgage.

Mortgage rates are incredibly cheap today, and have been for many years. But as I concluded in this piece about renewing your mortgage, your decision shouldn’t rest solely on getting the lowest mortgage rate. Flexible terms matter, both for paying down your mortgage early, and for the ability to break your mortgage without punitive charges.

This Week’s Recap:

On Wednesday I explained why you should forget everything you’ve heard about asset location and just hold the same asset mix across all of your accounts.

Over on Young & Thrifty I compared investing in real estate vs. investing in stocks.

Promo of the Week:

I still get a surprising number of emails from readers looking for the best high interest savings account. Savings rates have fallen sharply since the pandemic hit and the Bank of Canada made emergency rate cuts. The big banks pay next to nothing on their savings accounts, and even a former market leading online bank like Tangerine has cut its rate to just 0.25%.

I know I keep harping on this but I’ll mention once again that EQ Bank’s Savings Plus Account pays 2% interest with no promos or teasers. It’s a great place to park your short-term cash savings or an emergency fund. And, it comes with some chequing account functionality like e-Transfers and bill payments.

Open an account here and fund it with $100 within 30 days and you’ll get a $20 cash bonus for free.

Weekend Reading:

Sticking with the mortgage and housing theme, Alexandra Macqueen shares six strategies for first-time home buyers.

Stephanie Hughes wrote a great piece summarizing the 2020 CMHC saga – CEO Evan Siddall versus the world.

Ask a real estate agent or mortgage lender if it’s a great time to buy and you can guess the answer. A mortgage agent takes that sentiment one step further, offering this dangerously bad take:

“A $500,000 property you bought today will be worth $873,000 in 10 years. That’s an average of 7.45 percent annual increase, beating a medium-risk investment portfolio.”

Rob Carrick shares five numbers that will douse any high hopes you may have for the housing market.

Credit Card Genius determines which Canadian rewards program is worth the most.

In episode three of SPENT, Preet and Derrick discuss the impact of COVID-19 on the travel industry, and how it will change in the future:

Speaking of travel, The Guardian offers a sobering take on how to reinvent a tourism industry that does so much damage to our culture and climate.

Wealthsimple has introduced a new Socially Responsible Investing portfolio with lower fees and more stringent filters that weed out bad companies and even industries.

Is your ETF portfolio actually diversified? Maybe not if you invest in a market-weighted S&P/TSX Composite index, or S&P 500 ETF.

With post-secondary education looking much different this fall, many high school graduates are weighing the benefits of taking a gap year.

Taking a gap year usually means traveling or working. With travel not looking likely, more young people will be looking for work. Global’s Erica Alini explains who is hiring right now.

This New York Times piece warns that a tidal wave of bankruptcies is coming in the United States:

“The flood of petitions from the worst economic downturn since the Great Depression could swamp the system, making it harder to save the companies that can be rescued, bankruptcy experts said.”

My Own Advisor Mark Seed explains the tricky subject of when to sell a stock after a dividend cut.

With a dramatic rise in day trading, Ben Carlson says it seems crazy that we would see such speculation during the most severe economic crash of our lifetimes. But speculation is as old as the hills.

Finally, a new evaluation of Old Age Security reports that only 17% of Canadians were aware they could defer their Old Age Security pension. Here’s what I wrote about whether to defer OAS to age 70 or not.

Have a great weekend, everyone!

It’s hard to believe that just three months ago we were preparing to travel to Italy. It was one of several trips we had planned for 2020, including a return to the U.K. in July and a trip to Victoria to close out the summer. Then COVID-19 hit and our plans quickly changed.

Italy was cancelled (obviously), but we held onto our U.K. booking until travel and refund policies became more clear. That changed last week when our return flight was cancelled by the airline. That was the sign we needed to cancel the remainder of our trip.

Some countries are preparing to loosen travel restrictions in hopes to welcome international travellers this summer. But the Government of Canada is still advising Canadians to avoid non-essential travel until further notice.

Interprovincial travel is also still widely discouraged, although restrictions vary across provinces. The BC government says, “Now is not the time to travel for tourism or recreation.” That likely spells the end for our planned trip to Victoria in late August.

Our flights to Italy and the U.K. were booked through Aeroplan and so when we cancelled our miles were returned and fees & taxes were 100% refunded by Air Canada. Thousands of Canadians haven’t been so lucky with their cancelled travel plans, as airlines have been issuing travel credits instead of cash refunds.

We booked our flights to Victoria through WestJet, which is likely subject to the travel credit policy should we cancel.

What’s Next for Travel?

We’re prepared to spend summer at home and have adopted a wait-and-see approach to future travel. While we’d love to have a do-over next year and re-book our trips to Italy and the U.K., there’s just too much uncertainty to do anything as long as Canada’s travel advisory remains in place.

We’re also thinking about how the travel experience will change due to COVID-19. Additional screening at airports will make the check-in and arrival process even more cumbersome. Will airlines continue to leave the middle seat open and operate at 70% capacity or less? What impact will that have on airfare? Will we be required to wear masks on-board the aircraft? How will that work on longer flights with meal service?

When it comes to accommodations, would you prefer to stay at a hotel or a short-term rental (Airbnb)? I’m leaning towards Airbnb. Why?

Most hotels are poorly equipped to operate in a COVID-19 world. You have hundreds of travellers arriving from all over the world. There are way too many touch points, including check-in, baggage handling, and the ubiquitous restaurant buffet.

Many Airbnbs offer keyless entry and guests can do their own additional cleaning and sanitization to suit their comfort level.

While we dream of travelling in a post-COVID world, we’ve changed the way we collect and redeem credit card rewards. I switched to a cash back credit card – the Scotia Momentum Visa Infinite card – to earn more money back on groceries and other essentials. We’re also collecting and redeeming more PC Optimum Points.

In the meantime, we’re sitting on 600,000 Aeroplan miles – ready to deploy once it’s safe to resume international travel again.

This Week’s Recap:

Earlier this week I wrote about how and when to rebalance your portfolio.

Over on Young & Thrifty I explained how to invest your money in 2020.

At Greedy Rates – the stock market might crash, but what does that mean for your investments?

I applied for 13 credit cards last year. Here’s what that did to my credit score.

Promo of the Week:

Last week I highlighted EQ Bank as a great place to park your emergency fund or cash savings. Of course, their website was undergoing maintenance last weekend and many of you weren’t able to sign up. So, once again, here’s a plug for EQ:

EQ Bank’s Savings Plus Account consistently offers an everyday high interest rate at or near the top of the market with no hassles. Open an account here and fund it with $100 within 30 days and you’ll get a $20 cash bonus for free.

Weekend Reading:

I enjoyed the first episode of Rob Carrick’s and Roma Luciw’s new podcast called Stress Test. This one looks at how to survive the gig economy.

Erica Alini explains why more seniors are expected to turn to reverse mortgages due to COVID-19.

Jason Heath shares four key things to consider before taking an early retirement package.

Here’s why the bank of mom and dad will need to step in as millennials struggle during the pandemic.

Millionaire Teacher Andrew Hallam smartly explains why emerging market ETFs are a great deal now.

A shocking stat from the Better Dwelling blog shows that the Canadian personal HELOC growth rate nearly tripled in a month.

“Canadians are tapping their home equity very rapidly, and at a time it could be dangerous for them. At the start of the pandemic, the annual growth rate doubled, and nearly tripled for personal use. Considering the abrupt nature of a pandemic, it’s expected to see homeowners tap home equity. That’s what it’s there for. That doesn’t change that higher debt levels make households more vulnerable to shock.”

Trevor Tombe explains why Canada might need a temporary COVID-19 tax and repayment fund.

Wondering what it’s like to fly during the pandemic? The Prince of Travel shows what it’s like in the “new normal”:

My Own Advisor Mark Seed asks an insurance expert whether he should renew his expiring term life insurance policy.

Of Dollars and Data blogger Nick Maggiulli explores the depth of privilege:

“But privilege goes beyond growing up with wealth or having more opportunities than others. Privilege is in the color of your skin, the community you grew up in, and so much more.”

Dale Roberts from Cut the Crap Investing looks at changes made to the TSX 60 Index to explain why index investing works.

Financial advisor Jason Pereira takes a critical look at the self-directed investing platform Questrade and some of its misleading advertising claims.

This Forbes article takes a look at finding your retirement paradise.

Tim Hortons is logging detailed location data of customers through its app — and many may not realize it’s happening at all.

Finally, an investigation into the death of a cryptocurrency founder revealed a Ponzi scheme that cost investors $169 million.

Enjoy the rest of your weekend, everyone!

Setting up the initial asset allocation for your investment portfolio is fairly straightforward. The challenge is knowing how and when to rebalance your portfolio. Stock and bond prices move up and down, and you periodically add new money – all of which can throw off your initial targets.

Let’s say you’re an index investor like me and use one of the Canadian Couch Potato’s model portfolios – TD’s e-Series funds. An initial investment of $50,000 might have a target asset allocation that looks something like this:

| Fund | Value | Allocation | Change |

| Canadian Index | $12,500 | 25% | — |

| U.S. Index | $12,500 | 25% | — |

| International Index | $12,500 | 25% | — |

| Canadian Bond Index | $12,500 | 25% | — |

The key to maintaining this target asset mix is to periodically rebalance your portfolio. Why? Because your well-constructed portfolio will quickly get out of alignment as you add new money to your investments and as individual funds start to fluctuate with the movements of the market.

Indeed, different asset classes produce different returns over time, so naturally your portfolio’s asset allocation changes. At the end of one year, it wouldn’t be surprising to see your nice, clean four-fund portfolio look more like this:

| Fund | Value | Allocation | Change |

| Canadian Index | $11,680 | 21.5% | (6.6%) |

| U.S. Index | $15,625 | 28.9% | +25% |

| International Index | $14,187 | 26.2% | +13.5% |

| Canadian Bond Index | $12,725 | 23.4% | +1.8% |

Do you see how each of the funds has drifted away from its initial asset allocation? Now you need a rebalancing strategy to get your portfolio back into alignment.

Rebalance your portfolio by date or by threshold?

Some investors prefer to rebalance according to a calendar: making monthly, quarterly, or annual adjustments. Other investors prefer to rebalance whenever an investment exceeds (or drops below) a specific threshold.

In our example, that could mean when one of the funds dips below 20 percent, or rises above 30 percent of the portfolio’s overall asset allocation.

Don’t overdo it. There is no optimal frequency or threshold when selecting a rebalancing strategy. However, you can’t reasonably expect to keep your portfolio in exact alignment with your target asset allocation at all times. Rebalance your portfolio too often and your costs increase (commissions, taxes, time) without any of the corresponding benefits.

According to research by Vanguard, annual or semi-annual monitoring with rebalancing at 5 percent thresholds is likely to produce a reasonable balance between controlling risk and minimizing costs for most investors.

Rebalance by adding new money

One other consideration is when you’re adding new money to your portfolio on a regular basis. For me, since I’m in the accumulation phase and investing regularly, I simply add new money to the fund that’s lagging behind its target asset allocation.

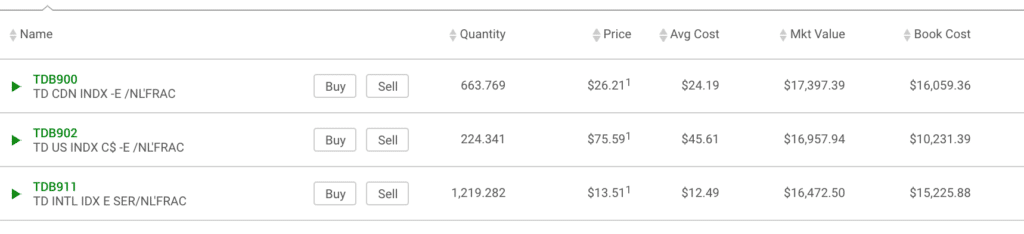

For instance, our kids’ RESP money is invested in three TD e-Series funds. Each month I contribute $416.66 into the RESP portfolio and then I need to decide how to allocate it – which fund gets the money?

My target asset mix is to have one-third in each of the Canadian, U.S., and International index funds. As you can see, I’ve done a really good job keeping this portfolio’s asset allocation in-line.

How? I always add new money to the fund that’s lagging behind in market value. So my next $416.66 contribution will likely go into the International index fund.

It’s interesting to note that the U.S. index fund has the lowest book value and least number of units held. I haven’t had to add much new money to this fund because the U.S. market has been on fire; increasing 65 percent since I’ve held it, versus just 8 percent each for the International and Canadian index funds.

One big household investment portfolio

Wouldn’t all this asset allocation business be easier if we only had one investment portfolio to manage? Unfortunately, many of us are dealing with multiple accounts, from RRSPs, to TFSAs, and even non-registered accounts. Some also have locked-in retirement accounts from previous jobs with investments that need to be managed.

The best advice with respect to asset allocation across multiple investment accounts is to treat your accounts as one big household portfolio.

That’s easier said than done if you’ve got multiple accounts held at various banks and investment firms. The goal in this case should be to simplify your portfolio and, if possible, hold the same portfolio across all accounts to avoid complexity and confusion.

This goes counter to the idea of keeping fixed income in your RRSP, and Canadian equities in your TFSA, for example.

In my experience, the simpler the portfolio, the easier it is to manage and stick to for the long-term. Imagine the nightmare of trying to rebalance multiple portfolios with different asset allocation targets whenever you add new money and as stocks and bonds move up and down.

Related: Top ETFs and Model Portfolios for Canadians

My investment accounts are super easy to manage today, with my RRSP, TFSA, and LIRA all invested in Vanguard’s VEQT. The beauty of these asset allocation ETFs is that they are a wrapper containing multiple ETFs, each representing different stock and bond indexes from around the world. The funds are then automatically rebalanced for you to always maintain their initial target mix.

If you prefer to hold multiple index funds or ETFs in your accounts, aim to keep the same asset mix across all of your accounts to avoid complexity. Follow a rebalancing strategy by date or by threshold and stick to it. And, when adding new money, contribute to the fund that’s lagging behind its target weight.

Ideally, you can avoid rebalancing altogether by using an asset allocation ETF (VBAL, VGRO, etc.), or by investing with a robo advisor where they automatically rebalance your portfolio for you.

Final thoughts

Your original target asset mix is arguably the most important decision when it comes to building your investment portfolio. Over time, as your investments produce different returns, your portfolio drifts away from that initial target, exposing it to risks that might not be compatible with your goals.

Rebalancing your portfolio reduces that risk exposure and increases the likelihood of achieving your desired long-term investment returns. The other benefit of a rebalancing strategy is that it forces you to buy low (i.e. the lagging fund) and sell high (or at least avoid buying as much of the high-performing fund).

Do you have a question about rebalancing your portfolio? Ask away in the comments below: