This is a guest post by Steven Arnott, a fellow reader and author of The Snowman’s Guide to Personal Finance: A simple approach to managing your money. You can find more of Steven’s work at snowmansguide.com or by following him on Twitter (@snowmans_guide).

This article provides step by step instructions to earn between $60 to $150 an hour working for yourself. As the CFO of your personal finances, you can find ways to spend less and earn more. Opportunities include:

- Confirm if each expense is bringing you enough value to continue – ($100 / hour)

- For expenses you value, see if you can negotiate a lower cost – ($60 / hour)

- Negotiate a raise – ($150 / hour)

- Find a new position with a higher salary – ($125 / hour)

- Take any reduced spending or increased earnings from above and pay off debt – ($150 / hour)

- Take any reduced spending or increased earnings from above and invest – ($60 / hour)

With cost of living up (e.g., education, housing, food, childcare) and wages fairly flat, more and more people are turning to side hustles to make up the difference. Side hustles typically involve providing a service (e.g., freelance writing, driving, dog walking) for someone else. But an often-overlooked side hustle that has tremendous potential is to provide a service to yourself. You can earn $60 to $150 an hour serving as your own CFO.

Taking the CFO position

If you were hired as the CFO for a company, you may start with a few of the following tasks:

- Review the financial statements to understand the health of the company (e.g., are they earning more than they’re spending, how much money is in the bank)

- Ask the department heads if there are ways to spend less (e.g., bundling orders, changing vendors)

- Ask the department heads if there are ways to sell more (e.g., a new pricing strategy, cross-selling to existing clients)

If you’re not interested, and potentially not yet qualified to be the CFO of a company, you may be excited to hear that you can make similar money by being your own CFO. The job isn’t much different, however instead of the company benefiting from your hard work, you realize the value. Tasks can include:

- Reviewing your own finances to understand your financial health (e.g., how much you own and owe, how much you earn and spend)

- Revisit your expenses (e.g., negotiate your bills, lower the interest you’re paying on any debt, cancel subscriptions you’re not using enough, minimize the taxes you pay)

- Increase your earnings potential (e.g., negotiate a raise, set aside savings and look to invest)

Your earning potential as CFO

Let’s look at the type of hourly earnings you could expect for some of the activities. Before we begin, I’ll admit that for many, the benefit of a side hustle is to earn money today. Some of the tasks below will provide an immediate return, while others will take time to pay off. Each of the steps you’re able to take will set you up for a more stable financial future, allowing you to spend your time on what you enjoy.

Revisit your expenses

We often spend money out of habit rather than conscious thought. Two ways that you can ensure you’re getting the most for your money are:

- Confirm if each expense is bringing you enough value to continue – ($100 / hour)

- Steps:

- Gather your credit card and bank statements for the last 3 months. (30 minutes)

- Review each expense and reflect on whether it was worth the cost. (1 hour)

- Identify a list of any expenses you’d like to cut back on. (30 minutes)

- Add a description of how you’ll reduce that cost going forward. (1 hour)

- You could share with your friends that you’re saving money the next time they invite you for a dinner out. Or arrange a rotation where you each host a dinner at home.

- Calculation:

- People are often shocked at how much they spend on a monthly basis on small purchases. Dining out and transportation are some of the most frequent areas.

- If you can identify $25 a month in expenses that you can live without and put a plan in place to avoid them going forward, you’ll save $300 a year.

- With an upfront investment of 3 hours of your time, you’ll be well paid for your efforts.

- Steps:

- For expenses you value, see if you can negotiate a lower cost – ($60 / hour)

- Steps:

- Use the same monthly statements from above to identify your recurring payments. Examples include:

- cell phone

- car or home insurance

- internet

- bank fees

- cable – if you haven’t cut the cord just yet

- Research current offers from competitors of your current provider. (1 hour)

- Find or draft a script of what you’ll ask on the phone. (1 hour)

- Remit Sethi, author of I Will Teach You to Be Rich, has championed this idea for years and provides many scripts on his website.

- Call each provider to see if there is a lower cost service, bundle, or loyalty discount they can provide. It’s important here not to add services you don’t already have and need. (2 hours – try to find something else to work on in case you’re placed on hold, but don’t let this discourage you)

- Use the same monthly statements from above to identify your recurring payments. Examples include:

- Calculation:

- There are several ways to lower your costs here. You could:

- reduce the services you’re receiving if a lower package will still meet your needs.

- switch to a competitor for a lower price.

- negotiate a lower rate with your current provider for the same service.

- If you’re able to reduce your monthly costs by $20 you’ll have $240 more each year. This earns you $60 for each hour of your efforts in the first year alone.

- There are several ways to lower your costs here. You could:

- Steps:

An important note is that this job isn’t a one-time engagement. As you adjust to your new spending habits, revisit your expenses again from time to time. The goal is to make sure you’re getting the most from your money, and spending on activities that will bring you the most fulfilling life.

Negotiate your salary

The unemployment rate in Canada is at its lowest rate since the 1970s. A low unemployment rate typically gives employees more power because employers need to compete to attract talent. With job vacancies above 500,000 in Canada, there’s a lot of competition for the right people. Two ways that you can take advantage of this situation are to:

- Negotiate a raise – ($150 / hour)

- Steps:

- Research roles in your field to understand what the market is currently paying. Look at job postings, speak with recruiters and speak with colleagues in the industry. (5 hours)

- Research best practices for negotiating your salary. (3 hours)

- Rehearse how you’ll open the discussion. (2 hours)

- Rehearse your response to common questions or challenges your boss may have. (3 hours)

- Calculation:

- Data from PayScale shows that 39% of those who asked for a raise received what they asked for and 31% received less. This leaves 30% who didn’t receive a raise.

- If you don’t receive a raise, remain patient and ask for a time to revisit the discussion in the future. In addition, ask if there are any specific outcomes your boss needs to see before they’d be able to give you a raise.

- A 10% raise on an income of $40,000 is $4,000. Assuming a 50% chance at receiving the raise, your hourly wage for negotiating your salary works out to $150.

- Steps:

- Find a new position with a higher salary – ($125 / hour)

- First a note of caution. Money is only one piece of the equation when it comes to your job. If you enjoy the people you work with and you’re fulfilled at the end of each day then this option may not be for you. Compare the expected change in salary with the other changes to your lifestyle to see if it’s worthwhile.

- Steps:

- Research roles in your field to understand what the market is currently paying and what roles would align with your skills and interests. Look at job postings, speak with recruiters and speak with colleagues in the industry. (10 hours)

- Research best practices for finding a new job. (2 hour)

- Update your resume. (4 hours)

- Reach out to your network in the industry and directly to recruiters to avoid submitting a cold resume as often as possible. (5 hours)

- Research best practices for interviewing. (2 hours)

- Prepare for interviews. (5 hours)

- Complete interviews with prospective employers where you feel there’s a good match. (5 hours)

- Research best practices for negotiating your starting salary. (2 hours)

- Rehearse how you’ll open the discussion. (2 hours)

- Rehearse your response to common questions or challenges you may face. (3 hours)

- Calculation:

- Data from a 2018 Global News article suggests an average wage increase of 10% to 15% is reasonable to expect when changing jobs (provided you’re past an entry level position).

- A 12.5% raise on an income of $40,000 is $5,000. While going on the job search is a large commitment of time (40 hours or more) the potential payoff is significant. If you can achieve a switch with 40 hours of work, your hourly wage would be $125.

- Remember this calculation is only looking at the first year’s increase in earnings. However, you’ll continue to benefit from your newly earned income well into the future.

Pay off debt

- Take any reduced spending or increased earnings from above and pay down high interest debt – ($150 / hour)

- Steps:

- Calculate any extra money you’ll have on a monthly basis from steps you’ve taken above. (1 hour)

- Sign into your online bank account and set up a transfer to move the amount you calculated above to your loan account (e.g., student loan, credit card) every month. (30 mins)

- Calculation:

- If you have a $15,000 student loan at 5% interest or a $5,000 credit card balance at 15% interest, you’re paying $750 a year in interest costs.

- By applying $50 a month extra towards these debts, you’ll cut down the time to pay them back and the total interest.

- If you increase from paying $200 a month today to paying $250 (the $50 we mentioned), you’d save $250 in interest on the credit card and $750 on the student loan. An hourly wage of over $150 for setting up the transfer.

- Steps:

You can apply this strategy to a mortgage, personal line of credit or any other loan to reduce the interest you’re paying. Any dollar saved is a dollar earned.

Invest your savings

Finally, if you have existing savings, or for the money you’ve identified through steps above, compound growth can provide the financial security you’re after.

- Take any reduced spending or increased earnings from above and invest – ($60 / hour)

- Steps:

- Calculate any extra money you’ll have on a monthly basis from steps you’ve taken above and add it to any savings you have that you don’t need for the foreseeable future. (90 minutes)

- Read the easy way to start investing today. (30 minutes)

- Complete additional research on the options of interest to you. (2 hours)

- Open an account. (1 hour)

- Complete an initial deposit for any savings you have today and set up a transfer to move the amount you calculated above to your new account each month. (1 hour)

- Calculation:

- A reasonable expectation for a medium risk investment would be to earn 5% on average over an extended period.

- If you invest $50 a month for 5 years at 5%, you’d have over $3,400. $3,000 of that you set aside yourself and $400 came from growth on the investment. With 6 hours work to set up an account and transfer, you’ve earned $60 an hour for your efforts.

- Steps:

Closing Remarks

My goal for this article was to provide realistic examples of how to improve your financial situation through becoming your own CFO. While you may feel some examples are worth more or less than I’ve suggested, I hope the underlying message carries through. There are lots of personal finance topics to help you lower your expenses or increase your income. A short list of additional areas to explore includes:

- Lowering your taxes by learning about the Tax-Free Savings Account (TFSA) or Registered Retirement Savings Plan (RRSP).

- Lowering your taxes by understanding common credits and rebates you may be eligible for when filing your taxes.

- Receiving grants from the government to help pay for your child’s education through a Registered Education Savings Plan (RESP).

- Checking with your employer if they offer a retirement plan, and contributing to it if they match your deposits.

Each new article and idea will have an associated return on the time you invest as we’ve calculated for many examples above. If you enjoyed this post and would like to check out more of my work, I’d invite you to drop by snowmansguide.com once you’ve finished up here.

What steps do you take with your money that provide a great return on the time invested?

Questrade is best known for offering rock-bottom commissions for trading stocks. You can buy and sell individual stocks for as low as $4.95 per trade. Questrade even introduced commission-free purchases for any ETF in North America.

You can open your own self-directed investing account with Questrade with as little as $1,000. Unlike the big discount brokerages there’s no annual administration fee for smaller accounts. You’ll even get $50 in free trades when you open an account.

All of these reasons are why I recommend Questrade over any other online platform as the top discount brokerage for beginner investors and for more frequent traders.

I’m not the only one recommending this discount brokerage, check out Million Dollar Journey’s Updated Questrade Review.

We recently received this email from James:

I’ve moved all my investments ‘in kind’ from a financial planner to Questrade. The idea was to cut down on costs and have more control. My strategy is to invest in index funds and have a long term passive strategy (couch potato style).

However I have found the Questrade interface to be very confusing. I’ve never traded before or used a trading site of any kind.

Could you put together a ‘baby steps’ tutorial, right from the basics on how to use Questrade?

It can be tricky to figure out how to use a new trading platform. That’s why I’ve reached out to Laural Adams from Questrade to put together the following tutorial.

Related: How To Use A Stock Screener To Find The Best Stocks

Questrade Basic IQ tutorial

Welcome to online trading. Making the switch from working with a financial planner to doing your own thing can be exciting, but yes, also a little daunting.

Trust me, you’re not the only person looking at the screens and wondering what you should do first. Here’s a quick Questrade tutorial to get you started.

Step 1: Opening the platform

The first thing you need to do is figure out what platform you’ll be using. In other words – where will you be trading from the most? Questrade has four platforms:

- IQ Web – use this on any computer with an internet connection;

- IQ Edge – this is the desktop platform and our most powerful platform;

- IQ Essential – use this with your tablet or netbook (but you can use it on a desktop) and;

- IQ Mobile – this is for your smartphone.

Log into www.myquestrade.com and select either IQ Essential or IQ Web on the upper left corner of the window.

Note: IQ Web requires the installation of Microsoft Silverlight. If you do not have administrative privileges on your computer, IQ Essential is recommended.

If this is your first time accessing the IQ platforms, you’ll be required to fill out a few pages of market data agreements to classify you as either a professional or non-professional trader.

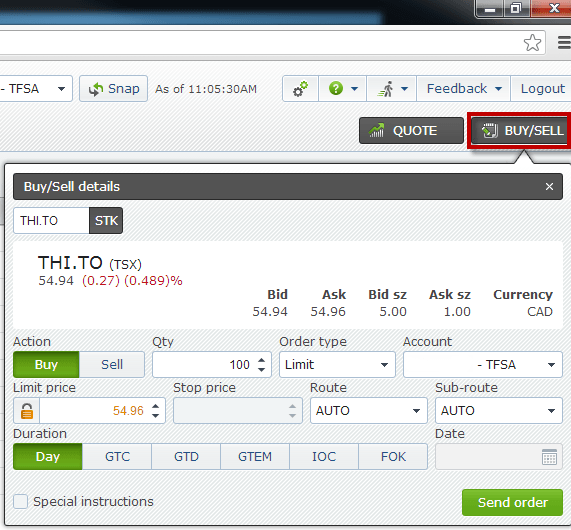

Step 2: Placing a trade

Once you’ve filled out all of this information, you are ready to trade. There are some basic questions you’ll need to be prepared to answer:

Order duration: You must choose the length of time you want your order valid for. For more information on the different order durations available, visit our blog post on order duration.

Order type: Here you can choose between setting a market, limit, or stop order for your trade. More advanced order types such as trailing stops and stop limits are also available for experienced traders.

For more information on the different order types available, visit our Order Entry 101 informational page.

Price: Unless you place a market order which will execute your trade at the best current bid or ask price, you will need to set a price at which you would like your trade executed.

Account: If you have multiple accounts (i.e. margin and TFSA), you can toggle between your accounts within the order entry box. Always make sure you are placing your trade in the correct account.

Related: TFSA vs. Non-Registered Accounts – Which Is Best?

Here’s what the screens look like:

IQ Essential:

To bring up the order entry box and place a trade, click on the buy/sell button on the top right corner of the screen.

IQ Web:

The order entry box can be found at the very bottom of the screen. You have the same options here.

Step 3: Reviewing your account

Beyond buying and selling, you will want to keep track of the activity in your account. Again, where you find this information is different based on the platform you use, but you’re looking for the same information.

IQ Essential:

You will find the following tabs near the bottom of the platform, which will show an overview of your account.

![]()

IQ Web:

You will find your account overview under the Account tab on the top of the page.

Orders: Displays any open or filled orders. You can use this tab to cancel or edit any open orders that haven’t been executed yet.

Positions: Shows all long and short positions within your account, including profit/losses.

Executions: A list of all trades that have been executed on the market.

Balances: Displays all your account balances in CAD and USD.

Activity: Here you can view all intraday activities for all your accounts that under the same login ID. Activities include orders placed and login times/locations.

And then you’re done!

This is just the tip of the iceberg, though. As you become a more advanced trader, you’ll have plenty more questions.

My suggestion: do your research, whether that means reading a blog, testing strategies with a free trial platform, chatting with other traders, or watching a video on Youtube.

Final Thoughts

This (conveniently) brings me to a little plug for Questrade. Open your own self-directed investing account and get $50 in free trades.

If you want to watch some video tutorials, check out our YouTube Channel. If you want to read more about products, services and trading ideas, check out our blog.

We’ve got free practice accounts available at Questrade.com. And, if you want to chat with your fellow traders, you can start a thread on the forums.

Related: Should You Trust Advice From Your Bank?

If you have any other questions, feel free to leave them here in the comments, and we’ll do our best to help you out.

Aloha! We’ve spent the past week in Maui escaping the cold winter back home and taking a much needed break. The past few months have been stressful and anxiety-ridden as I transitioned from a day job + side hustle to full-time entrepreneur.

I’m happy to say that life as an online entrepreneur is going better than expected. I’m getting flooded with fee-only financial planning inquiries and freelance writing assignments. I’ve made a point to stop working at 4pm when my kids get home from school. And three days a week I’ve taken a mid-day break to go to the gym with my wife. Life is good.

The only thing missing has been finding more time to write on my own blogs – both here and on Rewards Cards Canada. I hope to find a more consistent writing pattern as I fine tune my own rhythm and routine.

This trip to Maui has been so helpful because it has allowed me to take a break from the entrepreneurial grind and reflect on how I can spend my time more effectively. I’ve also been taking notes as ideas pop into my head for future blog post ideas. In between pool time, happy hour, and walks along the beach, of course.

It’s our first trip to Maui, even though it seems like everyone from Alberta and BC comes here on the regular. We haven’t been on a tropical vacation since our honeymoon in Mexico almost 14 years ago. First thought – why haven’t we done this before? Second thought – this is absolute paradise!

My personal finance blogger thoughts – Maui is so expensive! We flew here on an Aeroplan flight rewards, and so we only paid a few hundred dollars in fees and taxes. We also rented a car using Aeroplan miles – a first for me. With thousands already saved, we decided to splurge and stay at an ocean-front resort – an Airbnb – for $350 USD per night. Believe me, that was one of the cheaper condos available during this time.

Our flight got in late so we missed an opportunity to load up on groceries at Costco (the wholesale club near the airport is only open til 8pm). I drove 10 minutes to Safeway the next morning to get our groceries and some beer and wine for the week. After the $460 trip I came back cursing the sky-high Hawaiian prices and unfavourable USD to CAD exchange rate.

All good, though. Outside of the Old Lahaina Luau and one trip into town for lunch, we were quite content to spend our days poolside or at the beach, and preparing our own meals at home. It’s easy to see how a Maui vacation budget could quickly spiral out of control if we ate out at restaurants every meal or even once a day.

This was the first six nights of what will be at least 51 days of travel for our family this year. Next up is 18 days in Italy this spring, followed by three weeks in England and Scotland this summer. Finally, we’ve got another six nights booked in Victoria before the new school year begins this fall.

This Week’s Recap:

No posts here from me this week, but I did explain how to get more back on your tax return over at the Young & Thrifty blog.

From the archives: I did the math on your investment fees and the results weren’t pretty.

Over on Rewards Cards Canada – My experience using Airbnb vs. Hotels.

Promo of the Week:

I mentioned using Aeroplan miles to get to Maui and back, plus to rent a car for a week on our vacation. The fastest way to earn Aeroplan miles is typically by signing up for a Aeroplan branded credit card.

The

Weekend Reading:

Is Canada heading for a recession in 2020? Here are common causes and symptoms of a recession, plus eight ways to recession-proof your finances.

A husband and wife have very different risk tolerances. How can they get on the same page when it comes to investing?

How Millionaire Teacher Andrew Hallam fell for a Ponzi scheme while talking to a stranger:

“We all make mistakes when assessing other people. Defaulting to truth is a weakness. But it’s also a human strength. Perhaps, when making financial decisions, we should let the facts speak louder than the salesperson’s face.”

Tesla stock has been soaring lately and Wealthsimple dug into how clients on its Trade platform bought into the hype.

Interesting, because I switched to Wealthsimple Trade for precisely the opposite reason: to get zero-commission trades for my one-ticket ETF portfolio.

A Wealth of Common Sense blogger Ben Carlson shares some thoughts on young people getting into day trading.

An explosive article in the Globe and Mail last week suggested the robo-advisor model has been a massive flop across North America as assets haven’t flowed in as quickly as experts anticipated. Rob Carrick explains why robo-advisors beat these human advisors – sorry, salespeople – any day.

The Evidence Investor shares a lesson still worth learning three centuries later:

“The South Sea Bubble should stand as a reminder that successful investing is not about chasing the most exciting opportunities. It is actually the opposite: be boring. Diversify, keep your costs down, and let the market do its work over time.”

Sequence risk is the risk that investment returns happen in an unlucky order. It can make or break portfolios and this post shows how to protect against it.

Is it smart to hold a single exchange traded fund in your RRSP? Dan Bortolotti explains how to use an all-in-one ETF portfolio.

Here’s a very interesting post on retirement and the non-smoothing of our consumption of leisure.

Jonathan Clements has devoted his entire adult life to learning about money, but there are some key lessons that only came to him recently. Here are 10 things he wishes he’d been told in his 20s—or told more loudly, so he actually listened.

Finally, here’s John Heinzl with a thoughtful article on preparing your portfolio after a spouse is gone.

Mahalo, and have a great weekend everyone!