One of the biggest decisions retirees face is when to take their Canada Pension Plan (CPP) benefits. There’s a case to be made for deferring CPP until age 70, or taking CPP at 60, or somewhere in between (like the standard age 65).

You can view your estimated monthly CPP benefits online using your My Service Canada Account. But the information can be highly inaccurate. For instance, the My Service Canada estimate assumes you’ll continue earning your current salary until age 65. this can make your estimates either too high or too low, depending on your actual future earnings.

But questions abound when other variables are introduced. Like, what happens if you retire early and have a period of five or more years with no (or low) contributions to CPP?

For years Doug Runchey has offered a fee-for-service to help Canadians get an accurate estimate of their own CPP benefits. This business started very small but has since grown into nearly a full-time role for Mr. Runchey. He says that’s mainly because, “Service Canada is doing a terrible job of providing accurate information to many groups of people.”

Mr. Runchey has now partnered with Certified Financial Planner David Field to create a free CPP Calculator to give Canadians a simple and highly accurate way to calculate their Canada Pension Plan benefits.

“View the calculator here at www.cppcalculator.ca.”

I reached out to Mr. Runchey to get his feedback on why he (and partner David Field) created this free CPP Calculator for Canadians and what makes it different from the My Service Canada estimates.

Mr. Runchey said the free CPP calculator is different from the My Service Canada Statement of Contributions and online estimates for two main reasons, as follows:

Key Differentiators for the free CPP Calculator:

Future earnings – Our calculator uses whatever you enter for future earnings, whereas Service Canada pretends that the person is eligible for CPP in the following month, which has the same effect as projecting their average lifetime earnings through until age 65. Depending upon the person’s actual future earnings, that can make Service Canada’s estimates either too high or too low, but rarely is it accurate unless they are very close to being eligible for CPP.

Enhanced CPP changes – Our calculator includes the enhanced CPP increases for earnings in 2019 and subsequent years, whereas Service Canada’s estimates do not. This can make the Service Canada estimates far too low if the contributor will be working several years after 2019.

Variables not considered in the free CPP Calculator (or My Service Canada)

There are also other factors that neither our calculator nor the My Service Canada estimates currently deal with. It is my hope that our calculator will deal with at least some of these situations in the not-too-distant future, although for now they still require my full-service calculations, as follows:

Child-rearing dropout (CRDO) – Neither our calculations nor Service Canada’s estimates include the CRDO. This makes both of our results too low for anyone who can claim the CRDO. This is possibly our highest priority for improving our free calculator.

Post-retirement benefits (PRBs) – Neither our calculations nor Service Canada’s estimates consider the value of PRBs. This doesn’t affect the amount of the regular retirement pension calculations, but it does affect the breakeven analysis.

Combined retirement/survivor’s benefits – Neither our calculations nor Service Canada’s estimates consider the impact of the combined benefit calculations rules. These are quite complex and might never be part of our online calculator. They will remain part of my full-service business though, and they may transition to David’s business line at some point in the future.

CPP disability – Neither our calculations nor Service Canada’s estimates consider the impact of someone previously or presently receiving a CPP disability pension. We hope to include this in some future version of our calculator.

Mr. Runchey hopes the free CPP calculator will succeed so that he can begin to transition to semi-retirement again, and yet hopefully still enjoy an income from CPP calculations.

“Our CPP calculator is presently free, but hopefully once we get it fully up and running, we can start charging enough to cover expenses and realize a bit of profit from it. I have been told that my current full-service fees are quite low, but the eventual fees for our online calculator should likely be considerably lower.”

You can get an accurate CPP estimate using the free CPP Calculator here. For more complicated situations, I highly recommend reaching out to Doug directly for a full-service and personalized CPP estimate (including multiple scenarios and calculations).

This Week(s) Recap

I wrote the following posts over the past two weeks:

My wife’s trusty navigation helped me get over my anxiety about driving in another country. If you’re anxious about managing or investing your money, maybe you need a financial navigator.

This one’s for the anti-RRSP crowd – why RRSPs are not a government tax scam.

Credit card balance protection, mortgage life insurance, and other big financial rip-offs to avoid.

Over on the Young & Thrifty blog I wrote about the best GIC rates in Canada.

I also explained how to transfer a credit card balance wisely.

Weekend Reading:

Our friends at Credit Card Genius always have the most up-to-date list of the best credit card offers, sign-up bonuses, and deals of the month.

Want to know what’s happening with the Aeroplan loyalty program now that Air Canada is set to launch its own program later this year? The Prince of Travel has got you covered in this informative video:

From a former ad-man, why Wealthsimple and Questrade are winning the ad war this RRSP season.

Some index-embracing investors feel the need to ‘graduate’ their portfolio from TD e-Series funds to a lower cost portfolio of ETFs. Michael James explains the trade-offs of switching portfolios.

Des Odjick says the most damaging thing you can do for your money is believe that you’re bad at money.

Behavioural economist Shlomo Benartzi how digital design is helping to drive consumer behaviour.

Nick Maggiulli goes after the FIRE crowd’s cost cutting obsession, calling it the biggest lie in personal finance.

“But none of these things are the actual reason for how they retired early. Because the actual reason is either (1) earning a high income or (2) having an absurdly low level of spending, or both.”

On the flip side, Rob Carrick says it’s time to stop acting like retirement past age 65 is a failure.

An incredibly thought-provoking post by Lawrence Yeo, who says money is the megaphone of identity.

Millionaire Teacher Andrew Hallam wonders if you’ll be ready when stocks lose big.

Mr. Hallam also explained why strategies for happiness boost success and life expectancy.

Speaking of life expectancy, scientists are close to extending a human’s ‘healthy lifespan’. What would you do with 20 extra years?

Four Pillar Freedom breaks down the biggest misunderstanding about compound interest:

“Compound interest actually sucks early on. The magic only arrives in the later years.”

PWL Capital’s Ben Felix digs into the concept of socially responsible investing in his latest Common Sense Investing video:

Some great examples of retirement income and withdrawal strategies to keep more money in your pocket.

A question I hope to be able to answer for myself soon: I’ve maxed out my TFSA and RRSP. Now what?

Canadians used to live in a country that built housing with everyone in mind. What happened?

One answer could be here – How much does homeownership really cost?

Finally, the brilliant Morgan Housel explains why ‘easy’ comes in different flavours.

Have a great weekend, everyone!

I’ve made my share of bad financial decisions over the years, but nothing feels worse than when a salesperson convinces you to buy something that’s not in your best interest. These kinds of rip-offs usually occur when one party has more or better information than the other.

Think about the first time you bought a car or the first time you went to the bank to sign your mortgage documents. Who controlled the conversation? If you were like me, you probably deferred to the “expert” sitting across the desk and happily signed everything they put in front of you.

Related: 10 Fees To Avoid Paying

What you might not have known at the time is that some of the extras, such as extended warranty coverage or balance protection insurance for your credit card, were completely optional and most likely a giant waste of money.

Here are four big financial rip-offs to avoid:

Mortgage life insurance

If you own your home, chances are you were offered mortgage life insurance from your bank. This type of insurance is not a requirement to qualify for a mortgage, but it’s made to look that way by many lenders who suggest it at a time when you’re vulnerable and haven’t shopped around. You’ll even have to sign a waiver form to decline the coverage.

The reality is that it’s generally not a good idea to buy mortgage life insurance from your bank. It’s the one financial product that goes down in value as you continue to pay – also known as a declining benefit. Term life insurance is much cheaper and offers greater protection.

Extended warranty coverage

It’s almost guaranteed that you’ll be asked to buy an extended warranty the next time you purchase an appliance or any high-end piece of electronics. The reason for the hard sell is that retailers have big profit margins on these contracts. Stores keep 50 percent or more of what you pay for extended warranties or service plans, according to Consumer Reports research.

Consumer Reports recommends against buying extended warranty coverage. One reason is that most repairs may be covered by the manufacturer’s warranty, which should last at least 90 days or longer. Their research suggests that if a product doesn’t break while the manufacturer’s warranty is in effect, it probably won’t during the service-plan period.

Related: Gadget Insurance – Is It Worthwhile?

Many credit cards will double the manufacturer’s warranty when you use the card to make the purchase and register the product.

Balance protection insurance

One common telemarketing pitch from banks and credit card lenders is for balance protection insurance.

For a cost of about 99 cents per $100 of the average daily balance (about 1 percent per month) you can protect your credit rating against unexpected job loss or disability.

Customers might agree to add this protection to their credit card thinking that because they pay off the balance in full each month they’ll avoid the fee. Not so. The fee can based on the amount owing on your statement due date, or on your average daily balance, depending on the card issuer.

Not only that, the “protection” is riddled with exclusions, making it difficult to make a claim should you become ill or lose your job.

A CBC Marketplace investigation revealed how bank employees mislead and up-sell consumers on pricey credit card balance protection insurance. I’ve had personal experience with this, as CIBC added the insurance protection to my credit card account last year without my permission. More recently, my wife signed up for a card with TD and upon activation the customer service agent pushed balance protection coverage. When my wife declined, the agent persisted and asked, “why not?”.

Balance protection insurance is aggressively marketed to unsuspecting customers and should be avoided like the plague. You’re much better off protecting yourself with a small emergency fund, proper term life insurance and disability insurance.

Door-to-door sales pitches

It may be tempting to sign up for a home security system, or switch to a new energy supplier to save a few bucks. But always be cautious about door-to-door sales pitches. They may use deceptive pitches or questionable tactics and sell substandard, but expensive products or service contracts.

Related: City Councils, Please Ban Door-to-Door Sales

A reputable business shouldn’t require your signature at the door. Take your time and read the documentation at your leisure. If the sales pitch has a limited time offer attached to it, ask the salesperson to leave immediately and close your door.

Shop around for competitive quotes from businesses offering similar services. Contact the Better Business Bureau to investigate the company or to get a list of businesses offering similar service.

Before you sign any contract, take the time to read the fine print. Don’t get pressured into signing a contract on the spot.

Final thoughts

I’ve fallen for the extended warranty pitch a few times before and I’m guilty of signing up for mortgage life insurance on my first mortgage term. These days I’m a lot more cautious and borderline skeptical of any sales pitch that comes my way. I can spot a rip-off or a scam a mile away.

Related: Why Do People Fall For Telemarketing Scams?

What other rip-offs should you watch out for?

“I don’t invest in my RRSP anymore because I’ll have to pay tax on the withdrawals.” This type of thinking around RRSPs has become increasingly common since the TFSA was introduced in 2009.

The anti-RRSP crowd must come from one of two schools of thought:

- They believe their tax rate will be higher in the withdrawal phase than in the contribution phase, or;

- They forgot about the deduction they received when they made the contribution in the first place.

No other options prior to TFSA

RRSPs are misunderstood today for several reasons. For one thing, older investors had no other options prior to the TFSA, so they might have contributed to their RRSP in their lower-income earning years without realizing this wasn’t the optimal approach.

Related: The beginner’s guide to RRSPs

RRSPs are meant to work as a tax-deferral strategy, meaning you get a tax-deduction on your contributions today and your investments grow tax-free until it’s time to withdraw the funds in retirement, a time when you’ll hopefully be taxed at a lower rate. So contributing to your RRSP makes more sense during your high-income working years rather than when you’re just starting out in an entry-level position.

Taxing withdrawals

A second reason why RRSPs are misunderstood is because of the concept of taxing withdrawals. The TFSA is easy to understand. Contribute $6,000 today, let your investment grow tax-free, and withdraw the money tax-free whenever you so choose.

With RRSPs you have to consider what is going to benefit you most from a tax perspective. Are you in your highest income earning years today? Will you be in a lower tax bracket in retirement? The same? Higher?

The RRSP and TFSA work out to be the same if you’re in the same tax bracket when you withdraw from your RRSP as you were when you made the contributions. An important caveat is that you have to invest the tax refund for RRSPs to work out as designed.

Future federal tax rates

Another reason why investors might think RRSPs are a bum-deal? They believe federal tax rates are higher today, or will be higher in the future when it’s time to withdraw from their RRSP.

Is this true? Not so far. I checked historical federal tax rates from 1998-2000 and compared them to the tax rates for 2018 and 2019.

The charts show that tax rates have actually decreased significantly for the middle class over the last two decades.

Someone who made $40,000 in 1998 would have paid $6,639 in federal taxes, or 16.6 percent. After adjusting the income for inflation, someone who earned $59,759 in 2019 would pay $7,820 in federal taxes, or just 13.1 percent.

Minimum RRIF withdrawals

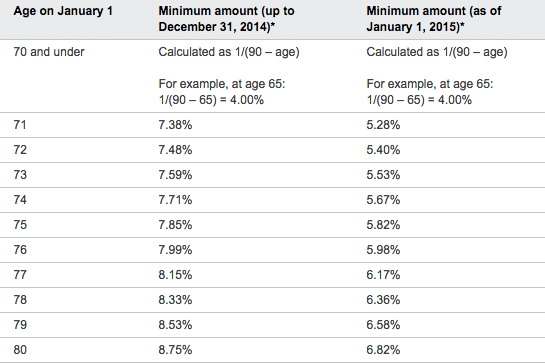

It became clear over the last decade that the minimum RRIF withdrawal rules needed an overhaul. No one liked being forced to withdraw a certain percentage of their nest egg every year, especially when that percentage didn’t jive with today’s lower return environment and longer lifespans.

In 2015 the federal government made changes to the minimum RRIF withdrawal table, bringing it more in-line with today’s reality:

The dreaded OAS clawback

Canadians who receive Old Age Security and have annual income between $75,910 and $123,386 will have all or part of their OAS pension reduced. This clawback is especially concerning for retirees whose minimum RRIF withdrawals push them over the income threshold.

Canada Revenue Agency uses the following example on its website:

The threshold for 2018 is $75,910.

If your income in 2018 was $86,000, then your repayment would be 15% of the difference between $86,000 and $75,910:

$86,000 – $75,910 = $10,090

$10,090 x 0.15 = $1,513.50

You would have to repay $1,513.50 for the July 2019 to June 2020 period.

This is a legitimate concern for retirees. No one wants to lose out on benefits that they’re entitled to receive. An advisor or tax accountant can help you determine a strategy that best optimizes your retirement withdrawals.

One such strategy is to make small withdrawals from your RRSP between the ages of 60-70 and delay taking CPP and OAS until age 70. This reduces the size of your RRSP for when you are forced to convert it into an RRIF and make mandatory withdrawals. It also increases your CPP and OAS benefits by 42 percent and 36 percent, respectively.

Related: CPP Payments – How Much Will You Receive From Canada Pension Plan

Canada Child Benefit

Parents with children aged 17 and under can be eligible to receive a tax-free monthly payment from the Canada Child Benefit. The CCB is a means-tested program, so the more income your household earns the less money you receive from this government program.

The Canada Child Benefit is completely phased out when your income is between ~$157,000 and ~$206,000, depending on the number of eligible children in your family.

The government uses adjusted net family income to determine how much you’ll receive from the program. Since RRSP contributions reduce your net income, it could be wise for young families to prioritize RRSP contributions ahead of TFSA contributions to reduce their net family income and help them receive more from the Canada Child Benefit the following year.

RRSP Matching

Some lucky employees work for companies that offer a matching program for your RRSP contributions. This is the best deal out there for savers. A guaranteed 100% return on your contributions. In fact, one could argue that contributing up to the maximum of your company’s RRSP matching program could be prioritized over paying off a credit card balance at 19% interest. It’s that valuable.

A company match will typically have some limits or restrictions. For example, your employer could match contributions up to 5% of your salary with the caveat that you must contribute to a group RRSP plan at a particular bank or investment firm.

It’s important to note that, even if the investment options are terrible high fee mutual funds, you should still contribute the maximum and take advantage of these generous matching dollars. You can always transfer the money over to a low fee indexing portfolio at some point in the future.

Final thoughts on RRSPs

RRSPs aren’t a scam; they’re a still a critical tool for Canadians to save for retirement. They’ve just got a bad rap over the years because of some misguided thinking around withdrawals, taxes, plus the introduction of a new and seemingly better (re: tax-free) savings vehicle.

RRSP contributions are still a key component of my financial plan. I’ve caught up on all of my unused contribution room and so now my goal each year is to max out my contribution limit (which is reduced by my pension contributions).

Related: TFSA Contribution Limit and Overview

TFSAs are great, and they get filled up next. In fact, when we paid off our car loan a few years ago we started catching up on our unused room and maxing out our TFSAs.

Both accounts are valuable parts of our financial plan and, along with my pension, will make up the bulk of our income in retirement.