When To Be Selfish and When To Be Generous In Retirement

Prospective clients come to me when they're on the cusp of retirement and looking for answers to key questions like when can I retire, how much can I spend, how long will money money last, and, ultimately, am I going to be okay?

I gather information about their current situation (income, account balances, asset allocation, expected income from a pension and/or government benefits, property value, debts, etc.), and ask them to list their financial goals and burning questions.

Then I plug those numbers into my financial planning software to model out my interpretation of their current situation and future goals to see what's possible. Your numbers are going to tell a story, whether there are obvious opportunities to take advantage of or red flags to consider.

I use conservative assumptions for life expectancy, rates of return on savings and investments, and assume spending will increase annually with inflation.

One common observation I notice is that the early retirement years can often be financially precarious. That's when new retirees want to spend the most money on travel and hobbies. It's also a period of time that often overlaps with the desire to help children through post-secondary and into early adulthood.

Throw in a new vehicle and a home renovation into the mix and you can easily see the financial stress signals mounting.

Meanwhile, early retirees haven't yet taken their government benefits, so they may be drawing significantly from their own savings (RRSPs, TFSAs, non-registered accounts) to make all of this work.

Not to mention poor stock market outcomes causing sequence of return risk.

I call this the retirement risk zone.

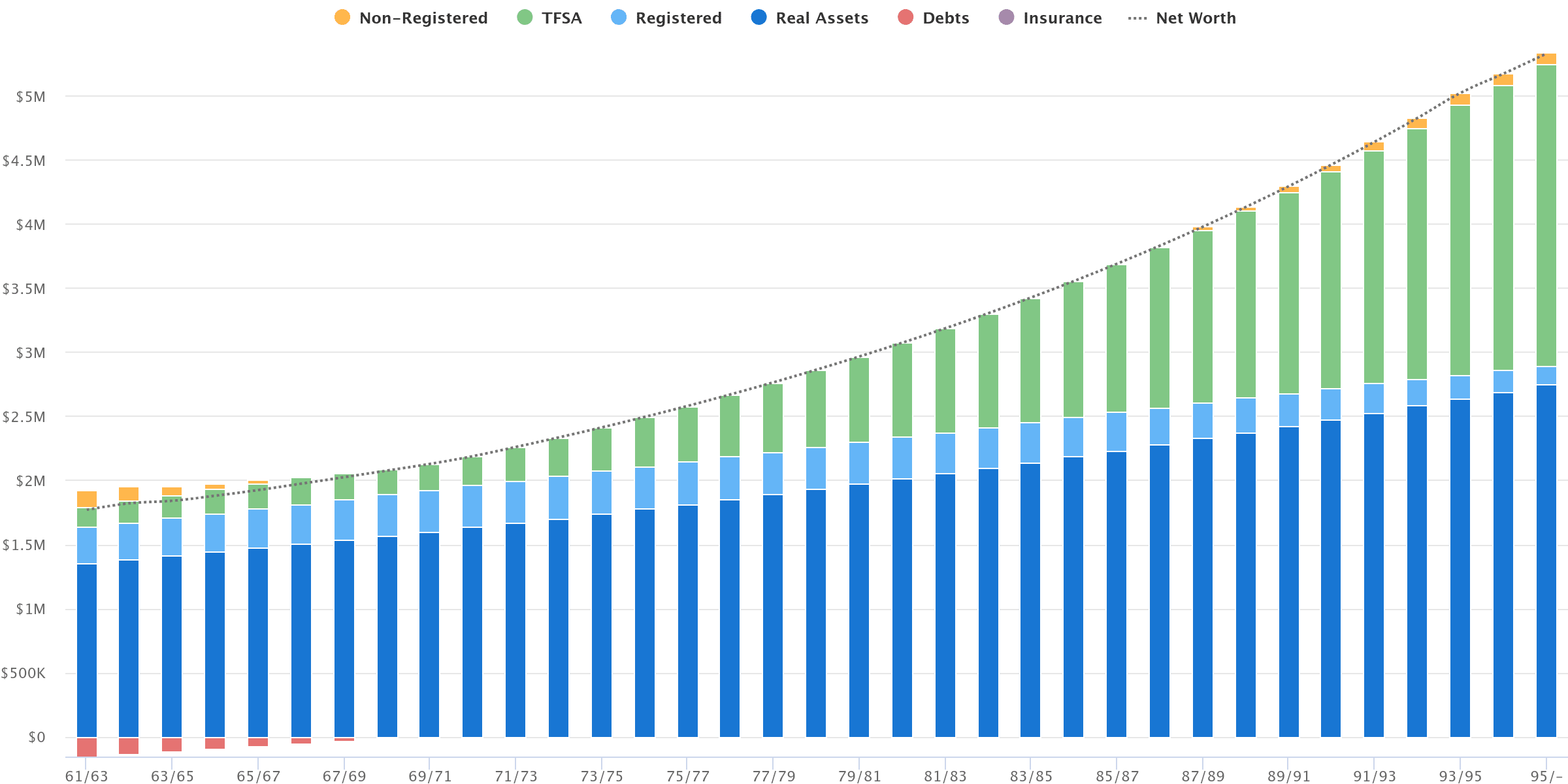

This can be a frustrating time for seemingly well-heeled retirees because they might see their retirement projections look something like this:

Your numbers tell a story, and the story here is a couple retiring with a net worth of $1.8M. Sounds great, except for the bulk of net worth is tied up in their home ($1.3M). And while they have about $600,000 in savings, they also still have a mortgage balance of $100,000 as they enter retirement.

See the dilemma? The couple sees their net worth taking off in their 70s and beyond (once CPP and OAS are fully kicked-in for the couple) and wants to pull some of that forward to spend more now.

But that's not possible without tapping into home equity (downsize, sell and rent, or borrow on a line of credit). That solution is not appealing for this newly retired couple.

It might be tempting to take up their CPP benefits early (ages 61 and 63, respectively), but they'd be giving up a permanent reduction in their benefits and a lifetime loss of income. Instead, they'll wait and take their CPP at age 66 along with OAS at age 65.

With the home equity release strategy off the table for now, the couple must spend carefully in these early retirement years to make sure their savings will last.

That means being “selfish” to ensure they can meet their desired spending needs over the next 5-10 years of early retirement (their go-go years).

Selfish because this does not appear to be the time to hand out large financial gifts to their children. Put on your own oxygen mask first before assisting others, as the saying goes. Take your own bucket list trip before emptying your TFSA to fund a child's down payment.

But, as your CPP and OAS benefits kick-in and boost your guaranteed income floor, and as the go-go years of spending wane, you might find yourself in an annual surplus and even contributing to your TFSAs again.

That, and you might re-consider selling the home as you age – which will top-up your savings buckets.

If your spending needs are being met, you have a surplus of cash flow, and you have an appropriate backstop of home equity and TFSA funds, then it makes perfect sense to explore an early giving approach with your child(ren). Give with a warm hand, before the will is read.

Indeed, rather than continuing to max out your TFSAs while your own spending declines in real terms and you're still sitting on a pile of home equity, consider your 70s as a time for generosity.

Think about it. Your kids might be in their late 30s, or early-to-mid 40s. A gift of $100k is arguably more valuable and significant at that age than an inheritance of $500,000 when they're in their 60s and already retired.

It doesn't have to be $100k – whatever you can reasonably afford in the context of your plan. It could be something as small (yet meaningful) as an agreement to fund your grandkids' RESPs annually ($2,500/year). What an incredible gift and a relief for young parents trying to balance competing financial priorities in their own lives.

Your generosity could be in the form of buying more time together as a family. One retired couple I've worked with pays for the entire family to go to Hawaii for a week each year – covering the airfare and accommodations so that their two children and their families can come together for a relaxing vacation.

The point is, you can scale your generosity to match your financial capacity and values (of course, respecting the needs of your children and their independence).

The key is to talk about it so everyone is on the same page and expectations are properly set.

So, rather than just filling up your TFSAs each year as your own spending declines – I'm making the case for some level of generosity into your 70s and beyond to prevent an overly large final estate and to help give with a warm hand.

You can still leave yourself with a reasonable margin of safety (home equity + TFSA balance) without getting too carried away with growing the pile.

The time to do that is not in your early 60s, when finances are a bit more precarious, but in your 70s and 80s as your personal spending slows down and your net worth starts to climb once again.

Retired readers: Are you providing financial assistance to your adult children in any capacity? How do you balance this in relation to your own retirement plan and resources?

What about a reverse mortgage?

I would consider a reverse mortgage later (75+) if you indeed want to stay in your current home and need to top-up your savings or income.

We did give our kids a substantial gift when we were in our mid-60s (our kids were in their early 40s) because we had more than we needed for our retirement. And we definitely understood that the money we gave them would make a huge difference in their 40s (a long-wanted house reno for one and help paying down a mortgage for the other). If they’d have to wait for an inheritance, they could be waiting up to 30 more years!

That’s fantastic, Tracey! Thanks for sharing.

Couldn’t agree more with providing financial assistance to children and grandchildren when it is needed. My wife and I are fortunate to have excellent defined benefit pension plans. I recently turned 70 and started CPP and OAS. My wife will do the same in 2 years. We know our monthly income will be the same and increasing with COLA for the rest of our lives. TFSAs are maxed, I emptied my RRIF by age 70 and the goal is to do the same for my wife.

Our kids have, and are, benefitting from our support now. 2 different sets of grandkids have $195K in an RESP and $97K and none are older than 13. We helped with down payments initially, have helped at times to pay down their mortgages. We have financed family holidays. We have supported charities now rather than as part of our wills. As you have indicated, we will still have our home as an eventual part of our estate.

Hi Bruce, thanks for your comment. What an incredible way to give back to your kids, grandkids, and your favourite charities. This is how it’s done!

I faithfully read your letter every week, very useful info.

Thank you,

Alfred

Thanks for the kind words, Alfred!

We have been doing as you suggest,

I am 69 and have over 1.00mm in my rrsp as well as over 500k in spousal rrsp. We have been drawing down spousal rrsp for tax planning/income splitting purposes and not needed for our expenses. We have maxed tfsa’s. We also have some non registered funds generating dividend income.

( as an aside,I have not contributed to my rrsp since in over 30 years so it is all compound growth)

When our son graduated from University we made a deal that we would match dollar for dollar his down payment…. That was five years ago. But requested that he lower the amortization period and maintain payments as if he had not received our help. He liked the idea and executed on it. He also made double payments on the mortgage and after 5 years he had reduced his amortization to about 15 years. He has shown he has both the discipline and financial literacy that we would hope for. A key thing was buying a house much LESS than the bank said he could afford. He has what I call lots of financial margin in his life.

My spouse and I did the same thing when we were young. We ended up paying off our house in about 6 years and my wife only worked the first 3 years of our marriage. I did not have a big salary….was making perhaps 45k at the start. We bought a small house……but upgraded after 4 years.

So…..this leads me to today. Literally this morning we decided that we will give our child 20k when his mortgage comes up for renewal (he has bought a different property and now married). This will allow him to save about 1k per year interest plus reduce amortization to less than 15 years PLUS they continue to put an extra amount on the mortgage each month. He informed that each payment reduced their amortization by about 2 months…..I think they will have it paid for in less than 10 years easily. Good for them and I am thankful they are both on the same page. The other add on is that they do not use debt to buy anything…..they just wait and then buy!

We have been fortunate to be able to do this gift. But it is a joy to see that the “kids” understand the benefits of financial literacy. That is a legacy gift. Hopefully they will be generous with others as they move forward in life…..

Just one families journey.

Hi Dale, thanks for sharing this – a very creative and educational way to support your son that will pay dividends (pun intended) for the rest of his life.

Hi I am retired in Calgary . My recent experience makes me really sceptical about assuming retirees can use the value of their home to fund their retirement until the very end of life in a long term care. We are finding that a newbuild replacement bungalow of similar features and half the size of our existing home will actually cost us about 20% more than we will get for our existing home. This make it hard to figure out if we can give any funds to our daughters.

Hi Ian, thanks for sharing the other side of this. I am also noticing that downsizes aren’t yielding the windfall that many hoped. Unless you’re moving to a lower cost of living area, you may find the move is more lateral or even an upgrade. A tricky situation, indeed.

My wife received an unexpected inheritance from her older brother. She gave almost all of it to our kids (34 and 38). 250k each. We expect to give them a bit more in 5-7 years, but the good news it hasn’t dampened the go-go stage of our retirement as we were expecting before the windfall.

The unfortunate thing is that even with that early inheritance, they with both still struggle to afford a house.

Hi Tom, thanks for your comment. I have seen this type of “pass-thru” inheritance before and it makes perfect sense if your own retirement plan is secure.

You’re right that housing is still a struggle in many pockets of the country. $250k will certainly go a long way to help!

Robb,

What a great topic! I swear you are following my personal timeline with some of your recent columns and especially this one. As a recently retired, soon-to-be 66 year old, together with my wife, we have been contemplating exactly this scenario of how to help out without endangering our own fiscal well-being. The funding of family holidays is one of our current go-tos, having completed a joint Alaska cruise last August. “Building Memories” with our son, his wife and our granddaughter is an endeavour we hope to continue as long as we are physically able.

Thanks also to other posters for sharing other ideas and experiences.

Cheers,

Alan

Hi Alan, haha – maybe I am!

I really love the idea of funding family holidays. It ticks all the boxes for getting to spend time with loved ones while also giving your kids a well deserved vacation that they might not be able to afford on their own in the early years of raising a family. Well done!

Robb,

As always a great topic. This is good if both are on the same page. I would like to help our grandchildren. My husband is afraid we will run out of money so does not want to be generous now. I have looked at our numbers and think we could be more generous now. Any suggestions on how to persuade him. Perhaps it’s our age difference I am 77 and he is 71 but I am in better health.

Mary

Hi Christine, this is exactly where a financial planner can help. Showing you what’s possible, including the ability to support kids and grandkids without running out of money yourselves – and even running multiple scenarios to show you a comparison of the “generous” scenario versus the “selfish” scenario to help you see the trade-offs.

I know you’ve run the numbers, but sometimes it’s helpful just to get an outside view from an objective third party.

My mother-in-law gave us a 2 million dollar house that she inherited upon her sister’s death 8 years ago. We were mid 30s at the time. We had done well and had around 1.3 million net worth when this happened. We decided to sell our primary residence, renovate the inherited home- move and live there.

The gift was life changing for us because we got to move to a higher cost of living area and still have a large house. In our case, we saw no greater value and urgency than growing our family- so we had 3 babies really close together.

Interestingly, we are both still working and trying our best to maintain what we were given so we can pass it to our children.

Inheriting the house opened up so many possibilities for us and I’m so grateful we were given this freedom so early.

It is interesting reading everyone’s comments on how they have approached giving with a warm hand. My husband and I are both retired and in our early 70s. We both have decent indexed defined benefit pensions and collect CPP and OAS such that it is enough for us to live the way we want. As a result, all our investments are not ‘needed’ for our day to day living expenses and most will ultimately go to our children, either with a warm hand or a cold hand. Although our pension income is more than we spend annually we tend to gift the excess to our children and grandchildren. Our problem, if you can call it that, is that we have 4 children who are married, each with 3 children of their own. That makes for a family of 22 people – it’s hard and expensive to plan family trips with that many people. We have done so, but unfortunately not everyone has been able to get away to come. Also, our children are at different financial levels. They are all gainfully employed in good careers and financially literate, but one has accrued more than their siblings, making our monetary gifts more useful to the three others. None of them expect us to give money to them and are most appreciative when we do. We tend to give to the more ‘needy’ ones but struggle with the fairness of that. Ultimately our cold hands will distribute whatever is left equally but I would like to hear what you and your readers think about an unequal gifting of cash now. Anything we have ever given was given with the understanding that it was not expected and we don’t need to talk about it with siblings. Not that it was a secret, but that way they didn’t know if we were giving anything or how much we might be giving to their siblings. Things we have done are, for example, we supplemented income while on maternity leave to the tune of monthly $1000 deposits until their salaries kicked back in, in a year to 18 months time. We have paid for hockey for the grandchildren or summer camps. We have paid for courses the adults may be taking and gifted money for home improvements. We have babysat daily to eliminate daycare costs. The thing is although over the years, we have done these sorts of things for all of them, we haven’t done it equally, because their situations are different and their needs are different and it is this imbalance that we struggle with.

On Monday our FA told us that approximately half of his clients have shared their blessings with their family, like you did. Helping them out and taking them on vacations.

The other half have the money but haven’t and don’t share it.

Don’t worry about your family. I doubt that they are keeping a running total and neither should you. You saw the need and responded in kind.

Doing childcare is invaluable for the kids and for you.

My wife was always all about “even Stephen.” I felt debt a free university education was enough and launched them.

But now, some of our kids are better off: one with a mortgage at zero percent, another with a mortgage but earning more on the invested money so hasn’t paid the mortgage off, and the third, good jobs but a bigger mortgage having moved upwards.

So guess who’s getting some help when the mortgage comes up for renewal?

It’s all good and so are the memories.