The Canada Pension Plan Investment Board manages $392 billion in assets on behalf of some 20 million Canadian contributors and beneficiaries. Operated at arms-length of the federal government, the CPPIB is the 11th largest sovereign wealth fund in the world (Norway’s trillion dollar pension fund leads the way).

While questions about Canada Pension Plan solvency abound, the fact is the CPP is rock solid, with an independent review by Chief Actuary of Canada determining its assets are sustainable to at least 2090. That’s a conservative estimate when you consider the projected annual real rate of return used in the review is just 3.9 percent.

Related: Where does my CPP money go after it gets deducted from my paycheque?

Meanwhile, the CPPIB has achieved 10-year annualized net real returns of 9.2%. It also posted an 8.9 percent net return for its most recent fiscal year, which included the challenging fourth quarter in 2018.

One area of concern raised by experts is the rising costs associated with managing the massive pension fund. Altogether the CPPIB spent $3.27 billion last year, an increase of $74 million from the previous year. Total costs work out to a management expense ratio of around 0.83 percent.

The reality is that our Canada Pension Plan fund is well managed, sustainable, and absolutely should be considered part of your retirement income plan. The average monthly payment amount for new beneficiaries in January 2019 was $723.89. That’s nearly $8,700 per year in pension benefits, indexed to inflation and payable for life.

The maximum monthly benefit for those eligible is $1,154.58 ($13,855 per year), and beneficiaries can increase their eligible amount by deferring CPP to as late as age 70.

This Week’s Recap:

I managed to post one article this past week, a comprehensive review of KOHO – the prepaid and reloadable VISA card that offers a full-service suite of banking services on its mobile app. Check it out.

Our trip to Scotland and Ireland is less than a month away (!) and we’re looking for some things to do in and around the places we’re staying, which include:

- Edinburgh (5 nights)

- Inverness (7 nights)

- Kilkenny (14 nights)

- Dublin (5 nights)

While in Edinburgh we plan on visiting Rosslyn Chapel and taking a trip out to St. Andrews. We’ve also scheduled family pictures with a company called Flytographer, a Canadian-based startup that connects travellers with a community of hundreds of local photographers in 275+ destinations around the world.

If you’re interested in checking out Flytographer for an upcoming vacation you can use this link or enter my referral code ROBBENGEN to save $25 on your first photo shoot.

From Inverness we have booked a day tour of the Isle of Skye, and may venture down to Fort William to take the Jacobite steam train.

Our plans are less set in Ireland and so we’re looking for ideas for day-trips from our home-base in Kilkenny, as well as some must-see attractions in Dublin. Let me know if you have any suggestions!

Long Weekend Reading:

Sticking with the Canada Pension Plan theme, here’s Alexandra Macqueen to explain how to understand your CPP Statement of Contributions.

Check out Rob Carrick’s new Real Life Money Launcher, a tool designed for young people to set up their savings after they start working.

TFSAs were supposed to help low-income Canadians save for retirement. It’s not working:

“Too many are not getting the advice they need to shed their RRSPs — and some are still, wastefully, saving in them.”

Here’s Global News money columnist Erica Alini on what happens if you die with too much money left in your RRSP.

Another stunning case of investor harm and lack of advisor oversight on behalf of Investors Group. This time, two clients over 90 years old were sold DSC funds with seven-year redemption schedules. In both cases, the clients died less than two years later and their estates were obliged to pay DSCs.

Is moving $1 million out of segregated funds and into ETFs a good idea? I’d say it’s a no-brainer.

This investor is paying 2.32% in fees and wants to know if that’s too much. Again, no-brainer.

“For an investor who owns mutual funds and works with an adviser, an average MER of more than 2 per cent is typical. Is it fair? Well, I’m sure the firm and its advisers think so. But for an investor, it will take an enormous bite out of long-term returns.”

Andrew Hallam explains how a Ponzi scheme can lure so many victims.

An Ontario man says he is “fuming” after losing 370,000 Aeroplan miles that he was saving for his retirement.

Meanwhile, an RBC customer had $1,734 stolen during an e-transfer. A weak password was blamed, as the victim’s security question to her friend was: “Who is my favourite Beatle?”

Here’s a strange one – Expedia charged a man almost $6,200 for a 1-night stay at a Holiday Inn.

Million Dollar Journey blogger Frugal Trader explains how to maximize the Canada Child Benefit.

My Own Advisor Mark Seed shares a great post on how to draw down a portfolio using Variable Percentage Withdrawal.

Mark also shared an update on his financial freedom target of age 50. The dream is becoming reality!

The psychology behind why few of us feel rich. Most people have a blind spot when it comes to money — we only compare upwards to people who have more.

Should you withdraw the commuted value of your defined benefit pension? Michael James answers with an emphatic no.

Finally, there has been a lot of talk about the Latte Factor and spend shaming in the media lately. Yet, Financial Uproar’s Nelson Smith says we aren’t talking about a potentially more destructive habit – the booze factor. We certainly spend more on wine than we do on coffee.

Enjoy the rest of the long weekend, folks!

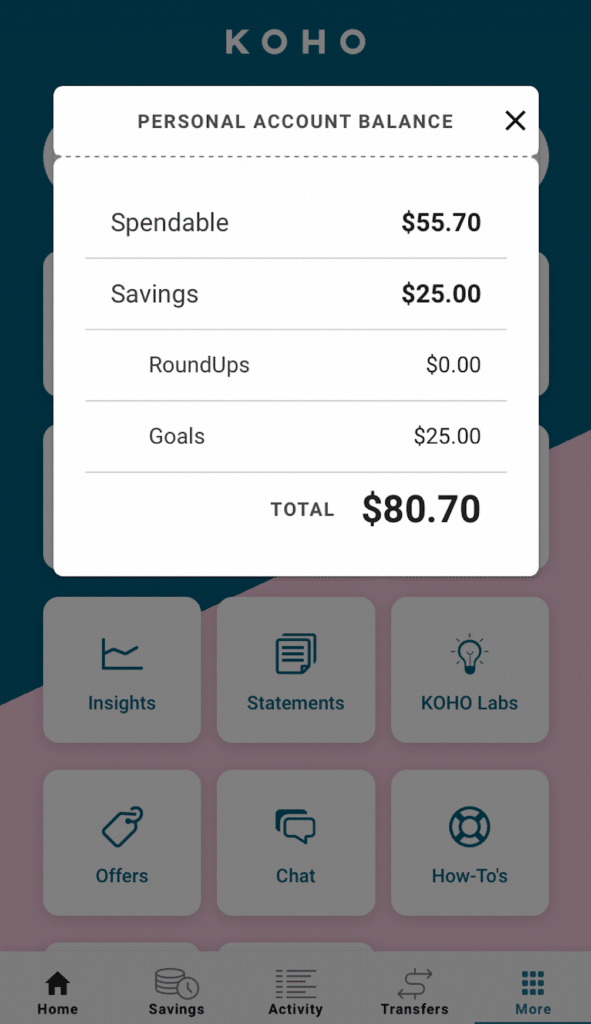

KOHO is a prepaid, reloadable VISA card, plus an app that can be used to access full feature banking services to help manage your finances right from your mobile device. While a prepaid credit card doesn’t sound all that special, KOHO takes it to the next level (and then some) with a product that is absolutely loaded with cool features designed to help save you money.

Let’s cut to the chase: If you’re interested in the KOHO card you can use my referral code BOOMECHO to get up to 1.5% cashback when you activate your card and make your first purchase. You can also earn another 0.5% cashback when you set up Payroll Direct (direct deposit with an employer).

Use this link to join KOHO and enter the referral code BOOMECHO to get up to 1.5% cashback.

I signed up for KOHO shortly after launch and have enjoyed using it for my miscellaneous spending every month, as a complement to my regular rewards credit card usage. Others have told me KOHO has become their go-to card for ALL spending – they love it that much.

Before you sign up make sure to read my full KOHO review here to determine whether the card and its app and features are a good fit for your money situation.

KOHO Review

I’ll reiterate that KOHO is NOT a credit card. Instead, it’s a reloadable, prepaid VISA card and can be used wherever VISA is accepted. A prepaid card won’t help you improve your credit score, but on the flip side, you can’t go into debt by spending money you don’t have. You can only spend what’s in your KOHO account.

With that out of the way let’s get into the many features and benefits that KOHO has built into this excellent product.

No account fees

KOHO doesn’t charge account fees or have minimum balances for its account. There’s no maximum number of transactions needed either to keep your account open and active. KOHO users can also withdraw money at any ATM free of charge, although users may still be dinged $2-3 from an out-of-network ATM. With KOHO you’ll also get free and unlimited Interac e-Transfers.

Compare that to the average monthly fee at one of the big banks in Canada where you’ll pay $15 per month for unlimited transactions. KOHO also compares favourably with many credit cards where customers pay annual fees of $120 just to earn some cash back or travel rewards.

Finally, you won’t pay NSF fees either. Instead, you’ll get a friendly notification if there aren’t enough funds to fulfill a transaction. Or, if you have the money tucked away in a Savings Goal (see below) the app will pull from there. Most banks charge NSF fees of up to $45 when a cheque or transfer bounces.

Cash back

When you use your KOHO card you’ll earn 0.5 percent back on every purchase (up to 1.5% cashback when you sign up through a referral). This is called a PowerUp. Your PowerUps accrue separately from your spendable balance. When you want to cash out, just select ‘PowerUps’ and then ‘Cash Out’. Your PowerUp balance will be loaded into your spendable balance.

Other Banking Features

KOHO doubles as an everyday account where users can set up Payroll Direct and have their paycheque automatically deposited onto KOHO. You can also:

- Pay bills

- Send e-Transfers

- Connect to PayPal to either send or receive funds

- Make online purchase using your KOHO card or Virtual Card

- Connect to and fund an investment account.

RoundUps

KOHO can help you save by rounding up your purchases to the nearest $1, $2, $5, or $10. Once you turn on this RoundUps feature, KOHO will automatically whisk away the “rounded up” portion of every transaction and put it into your savings.

Cashing out is the same as with your PowerUps – just select ‘RoundUps’ and then ‘Cash Out’. You can also review your RoundUps history and see how much you’ve cashed out all-time.

RoundUps have proven to be a popular feature and research from the behavioural psychology community views these small and automatic ‘nudges’ as a great way to get people to save more.

Behavioural insights

Speaking of nudges, KOHO not only offers spending insights to let you know how and where you spend your money – including monthly, weekly, and daily breakdowns – it wants to offer even better behavioural insights in the future.

Within the app is something called KOHO innovation labs. With it KOHO wants to use technology to bring you new features in the future – like the ability to pay a bill by just taking a photo of it.

It’s in the data gathering stage and so the little robot asks you to take a picture of a bill and upload it to the lab for analysis. It correctly guessed that my bill was from TELUS.

Savings goals

KOHO’s savings goals feature is very useful and intuitive as it helps you squirrel away a bit of money each day to help you reach your goal. It can automatically and virtually move your daily goal contribution (i.e. $5) from your spendable to your goal savings. You can cash out your goal savings at any time.

Creating a savings goal is simple:

- Step 1: Go to Savings à Create Savings Goal

- Step 2: Name your Goal

- Step 3: Enter the amount you want to save

- Step 4: Pick the date you need the money by

- Step 5: Add funds to your goal (optional)

- Step 6: Review your Savings Plan. Here you can edit your goal and adjust the savings frequency and contribution amount

One thing I like about KOHO’s savings goals is the visual separation between your spendable, your RoundUps, and your Savings. Let’s say you have $100 in your spendable and decide to move $25 to your savings. Your total available balance is still $100, but in the app you’ll only see $75 in your spendable and $25 hidden away in your savings. Another behavioural trick successfully applied!

Foreign exchange fees

One of the main reasons I signed up for KOHO was to save money on foreign exchange fees, especially for upcoming trips to the U.S. and abroad. KOHO charges a 1.5 percent fee on foreign transactions vs. a 3.5 percent fee with the big banks and credit card issuers. KOHO doesn’t profit from the FX spread.

One side note on using KOHO for travel – here are some tips to help get the most out of your KOHO card:

- Before you leave, use KOHO to save up for travel –> set a goal with the $ amount (your “travel budget”) and the date, then cash it out when you’re ready to travel. No more putting travel on credit.

- Loading money – if you didn’t use KOHO to save up for travel, load the card by e-Transfer.

- Taking money out – use any ATM with a Visa Plus sign, or at any merchant that accepts Visa.

- Real-time notifications – it can be hard to know how much you spend on vacation due to the exchange rates. With KOHO you’ll get real-time notifications in Canadian Dollars. Specifically, if you’re using a budget, this is such an easy way to stay on track. To stay “on-budget” you could move the money that was already in your general Spendable (before you cash out), into a savings goal to keep it separate until you get back.

- List of blocked countries are here. Unfortunately, you can’t use KOHO here for fraud protection reasons.

- Joint account for travel – it’s so much better than tools like Splitwise. If you’re going on a trip with one other person, open a free joint account and each load whatever amount of money you want into it. Then use that for that trip!

- Fees – there is a 1.5 percent FX fee (% of transaction value), vs. 3.5 percent for the big banks. There are usually ATM fees of $2-3 (charged by the merchant or bank), so you can save a bit of money by using cash and doing larger, less-frequent withdrawals.

- Apple Pay – don’t forget to use it abroad, too!

The newest KOHO features

KOHO users have come to expect new features and updates to their card and app over time. Here are the latest and greatest features that KOHO has to offer:

Joint Accounts

Now KOHO users can easily share finances with not only their spouse but also with a roommate, sibling, or friend. No romantic involvement necessary.

KOHO’s Joint Accounts are a free and easy way to share expenses with anyone you want – making joint spending and saving easier than ever before.

Joint Accounts offer all the same spending and saving features, including a no-fee account with a Virtual Card, bill payments, pre-authorized debits, free e-Transfers, and instant money transfers to other KOHO users.

To invite someone to create a Joint Account with you, select the ‘More’ tab à ‘Joint’ à ‘Create a Joint Account.’

Simply enter their email address – they do not have to be a current KOHO user. They’ll get an email invitation with information on how to join.

Each partner will receive a separate ‘joint card’ in addition to their own personal card. This is designed so your personal spendable and savings goals stay separate from your Joint Account partner. Only joint related activity is visible to your joint partner.

Apple Pay

KOHO is now compatible with Apple Pay. Now you no longer need your physical card to make purchases in-store.

To set up Apple Pay simply tap into your Apple Wallet, select the + sign to add your card, take a photo of your physical card or manually add your Virtual Card number, and you’ll be all set to make purchases wherever Apple Pay is accepted.

KOHO Premium

Launched in May 2019, KOHO Premium includes the following benefits (in addition to what users get with a regular KOHO Account):

- 2 percent cash-back on groceries, eating & drinking and transportation. Groceries includes both small merchants and large chains. Eating & drinking includes all restaurants, food delivery, bars, coffee shops and more. Transportation includes public transportation, Uber/ Lyft, taxis, gas, highway tolls, parking and more.

- No fee on foreign exchange transactions. The big banks charge 3.5 percent per transaction and KOHO’s non-Premium product charges 1.5 percent. KOHO uses Visa’s stated exchange rate (with no spread) for the currency translation, so they don’t profit off these transactions.

- Free financial coaching. Users will get weekly money tips and can set up sessions with a CFA, FPSC L1 financial coach to create a budget or ask any questions they have about taxes, investing, debt and more.

- Price-matching, whereby users can send in recent past receipts made online with KOHO and KOHO will search to see if they could have gotten a better deal. If so, KOHO will credit the difference in price to their account.

- Higher “velocity” limits, meaning that users can now take out $400 at an ATM per transaction, for a max of $800 per day. Their account balance can also be $40,000 instead of $20,000.

- Cost – Free for 30 days $9 per month, or $84 per year (saves $24).

KOHO’s Referral Program

Sharing is caring. Through KOHO’s referral program you and a friend can both receive a cash bonus of up to $60.

To refer a friend simply select the “Get $60” button at the top right-hand corner of your KOHO app to see your referral code. Tap on the code to copy and paste it or click the ‘Share Invite’ button to send the code directly by text or email.

Get a bonus of up to $60 – $20 when they make their first purchase, and $40 more if they set up Payroll Direct. You’ll both get a notification when the bonus hits your account.

You can get started by signing up for KOHO and entering my referral code – BOOMECHO – to get up to 1.5% cashback.

Final thoughts

KOHO has put together an incredible banking tool that is poised to help thousands of Canadians manage their money. Investors think so, too, as KOHO’s latest round of funding raised $42 million dollars – a deal that puts the company’s valuation at more than $100 million.

Use KOHO confidently for your everyday banking needs as it toggles seamlessly between chequing account, savings account, and credit card functionality.

Or, use it like I do in tandem with your favourite rewards credit card to manage your miscellaneous or variable spending without going over budget.

Either way, my KOHO review is positive and I’m looking forward to watching this new Canadian FinTech start-up grow and prosper while helping Canadians do the same.

This stuff makes me sick. A Toronto advisor got a slap on the wrist – a $65,000 fine and 30 day suspension – for making unsuitable recommendations for two retired clients. The advisor implemented extensive “double” leverage through the use of a margin account and borrowed funds from home equity lines of credit to invest in mutual funds with deferred sales charges.

“She referred to a leveraged strategy as a “no brainer” and minimized any risks associated with it.”

Furthermore, the advisor convinced her clients to transfer the commuted value of their pensions and invest in DSC mutual funds.

Perhaps most egregious, the advisor used her personal email address to communicate with the two clients, stating that she had difficulty remotely accessing her work email. In reality this protected her unsuitable recommendations from any employer oversight. In fact, she conveniently deleted several emails including the one in which she recommended her client borrow to invest.

These disgusting and shameful acts are all too common in an industry clinging to a commission-based model that’s clearly lacking in regulatory controls and oversight. We’ve heard the arguments not to paint the entire industry with the same brush, or that misconduct only happens with “a few bad apples”, while the rest of the industry is full of good guys and gals looking out for their clients’ best interests.

Bullshit. This doesn’t happen by accident. It’s the preferred playbook of unscrupulous advisors.

- Invest in deferred sales charge mutual funds

- Churn those mutual funds annually to generate commissions and trigger a new seven-year DSC schedule

- Encourage leverage through a margin account and/or home equity line of credit

- Encourage clients to take the lump sum commuted value of their pension and invest in a LIRA

- Encourage taking early CPP and invest the monthly benefits

- Discourage any other financial planning strategy (i.e. mortgage pay down) that doesn’t involve investing

Victims are not limited to seniors and immigrants who don’t know any better. It’s not surprising to find ordinary investors trapped in costly financial relationships with their “trusted advisor”.

That’s the problem with conflicted advice. Your advisor’s interests (his or her compensation) is not aligned with your interests (improving your financial situation). The end result is you get sold funds that may be “suitable” for you but might not be the best or most optimal for you and your wallet. You’re also told to invest above all else, which may or may not be the right advice for your personal situation.

This Week(s) Recap:

I’ve been busier than usual with financial planning and freelance work so I only managed one post here last week. I wrote about mental accounting and how we spend money.

Over on Rewards Cards Canada I revealed that I applied for 13 credit cards last year. Here’s what happened to my credit score.

Finally, many thanks to Rob Carrick for including my article on why I don’t pay off my mortgage in his Carrick on Money newsletter.

Promo of the Week:

Last year we partnered with Canada’s leading robo-advisor Wealthsimple to offer a free portfolio review and check-up with one of their portfolio managers. It proved to be overwhelmingly popular, and based on the feedback of my post earlier this year on how to transfer your RRSP to Wealthsimple, you guys are craving more info how to work with a robo-advisor.

That’s why we’re pleased to offer Boomer & Echo readers another chance to book a 15 minute call with a Wealthsimple portfolio manager.

Are you curious about moving over to a digital advisor but have some questions? Wealthsimple isn’t only suitable for a millennial audience:

- 32% of their clients are > 35 years old with a quickly growing % of clients with > $250k of assets under management

- Retirees are one of their fasting growing segments – hundreds of Canadian retirees are currently working 1:1 with the Wealthsimple team

- Their portfolio managers have conducted hundreds of financial planning calls + Portfolio Reviews

- They have a combined 80+ years of experience (average 10 years each)

- Team members hold CFA, MBA, CIM, CFP and PFP designations

- They are a fiduciary so they’re obligated to give you actionable feedback that’s in your best interest, not theirs.

- Wealthsimple Black ($100k+ deposits) and Wealthsimple Generation ($500k+ deposits) can qualify for additional benefits including even lower fees (0.4%) and more hands on financial planning sessions as well as Tax loss harvesting, tax efficient funds, Asset location and additional perks including a VIP airline lounge pass and Medcan discounts

Book a 15 minute call with a Wealthsimple Portfolio Manager.

Weekend Reading:

An honest and refreshing look from an advisor on why financial advisors should leave portfolio management to the experts and focus instead on financial planning. <— YESSSS!!!

In one of the more ridiculous surveys I’ve come across, this USA Today feature says we spend $18,000 per year on “non-essentials”. It goes on to list these items, which include three types of ‘dining out’ on restaurant meals, take-out, and buying lunch, along with personal grooming and ride sharing. In my world we don’t call these items “non-essentials” – we call them ‘miscellaneous’ spending, as in if you have your savings and fixed expenses covered then who the hell cares how you spend the rest of your money?

Frugal Trader explains what happens to your RRSP and TFSA after you die.

The maximum OAS a couple can get is $19,600. Here’s how to get all of it.

Recently retired Michael James on Money explains his bucket strategy for retirement spending.

We’re a long way from maxing out two RRSPs and TFSAs, but once we do we’ll want to start investing in taxable accounts. My Own Advisor Mark Seed has you covered with this post.

Jason Heath explains the tax implications of transferring between registered accounts – such as from a LIRA to an RRSP.

You can’t compare rent to a mortgage payment. Ben Felix explains why this way of thinking about the rent versus buy decision is extremely flawed in his latest Common Sense Investing video:

Don’t blame the government. Here’s what the Bank of Canada says is the real reason for the housing slowdown.

Respectfully interacting with people you disagree with, and other useful and overlooked skills from Collaborative Fund’s Morgan Housel.

Here’s Nick Magguilli on the necessary conditions for successful market timing:

“How do you know when a market decline will be 20% (or greater) before it happens? You don’t. You have to go off some feeling that this decline is “the big one” and not one of the smaller declines that happen more periodically.”

And here’s Nick again on cumulative advantage and how to think about luck – or why winners keep winning.

How about a double shot from A Wealth of Common Sense blogger Ben Carlson? First up he explains why you’ll never invest in the next Big Short.

Ben goes on to list some financial superpowers, including the ability to witness your neighbour getting rich or buying stuff without getting FOMO.

Finally, if you’re not following Sam Cooper’s stellar investigation into B.C. casino money laundering then you’re missing out. His latest expose reveals how organized crime first made its way into B.C.’s casinos.

Have a great weekend, everyone!