When should you take your Canada Pension Plan (CPP) benefits? Like many personal finance decisions, the answer depends on your unique circumstances. In general, it makes sense to defer taking CPP until age 70. The caveat is that you need to have other resources to draw from while you wait for your CPP benefits to kick-in. After all, who wants to delay spending in their “go-go” retirement years just to shore up their income in their 70s and beyond?

I’ve written before about when it makes sense to take CPP at age 60, why taking CPP at age 65 is never the optimal decision, and why taking CPP at age 70 can lead to $100,000 or more lifetime income.

But one question I often receive from readers and clients is when should early retirees take CPP? Here’s a reader named Keith, who decided to retire at the end of last year at age 60:

“My understanding is that since I won’t earn any income from now to 65, those five years will add to the CPP average calculation and potentially lower my eligible monthly amounts. If that’s the case, should I apply for CPP right away, or choose to defer it to 65 or 70? If I apply today, will those five years of zero income still be included in the average CPP calculation?”

It’s a great question. CPP is a contributory program based on how much you contributed (relative to the yearly maximum pensionable earnings) and how many years you contributed between ages 18 to 65.

To receive the maximum CPP benefit at age 65 you would need 39 years of maximum contributions. You can drop-out your eight lowest years (more if you are eligible for the child rearing drop-out provision) from the calculation.

Related: How Much Will You Get From Canada Pension Plan?

You can see the problem for early retirees. They’re going to have more “zero” contribution years which will reduce the amount of their CPP benefits.

Not so fast.

You will always get more CPP by waiting, even if you’re not working.

CPP expert Doug Runchey says that your “calculated (age-65) retirement pension” may decrease if you’re not working between age 60 and 65, but the age-adjustment factor will always make up for that decrease, and then some.

“In that situation I use the expression that you will receive a larger piece of a smaller pie if you wait, but you will always get more pie,” he said.

CPP checklist for early retirees

Here’s what to do if you’re in the early retirement camp and want to know when to take your CPP benefits. Log into your My Service Canada Account online and click on “Canada Pension Plan / Old Age Security.”

Scroll down to the “contributions” section and click on “Estimated Monthly CPP Benefits.”

You’ll see your expected CPP benefits at age 60, age 65, and age 70.

Now take that calculation and throw it in the garbage because it’s completely useless. That’s right. The CPP estimates you see here assume that you continue contributing at the same rate until age 65. That’s problematic if you plan to retire at age 58 or 60 and will no longer be contributing to CPP.

Go back to the previous screen and click on your CPP contributions. There you will find a web version* of your Statement of Contributions – a history of your contributions dating back to age 18. Right click on this page and “save as” (format: webpage, HTML only).

*Note you can request a copy of your Statement of Contributions in the mail, but you won’t need that for the next step.

Now visit www.cppcalculator.com and sign up for the website with your first name and email address. You’ll receive a confirmation email from the site founder David Field (co-created by Doug Runchey) to activate your account, followed by another email to login to the site and run your own unique CPP calculation.

Upload the statement of contributions that you saved earlier (or manually enter your pensionable earnings year-by-year). The beauty of the CPP Calculator website is that it allows you to manually enter future years, including future “zero” years if you plan to retire early.

I ran this calculation for myself because, as of right now, I am paying myself dividends from our corporation and not making CPP contributions (it’s a decision I continue to wrestle with, as I’d have to switch from dividends to salary and then pay both the employer and employee portion of CPP each year).

The estimate I shared above from My Service Canada is my own estimate based on 15 years of max contributions, plus another eight years of lower than max contributions. I did not contribute to CPP in 2020 or 2021, but it looks like Service Canada assumes I will continue making contributions until age 65.

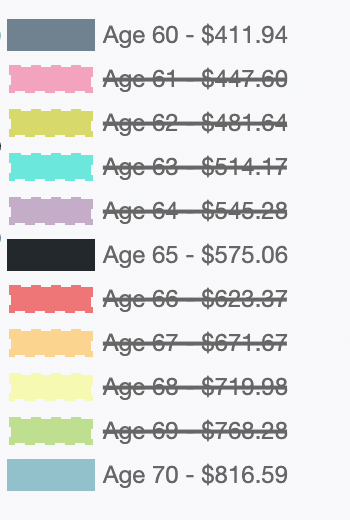

When I ran the numbers in CPP Calculator I assumed no more contributions to CPP from age 43 to 65. Look at the difference that makes for my CPP at ages 60, 65, and 70:

Instead of receiving $1,086.95 per month at age 65, I should only expect to receive $575.06 per month. That’s almost a 50% reduction in expected benefits. In other words, it’s a huge difference.

Final Thoughts

When should early retirees take CPP? There’s no definitive answer, but having the right data will help inform your decision.

The My Service Canada estimator assumes you work until 65. Use the CPP Calculator website and manually enter “zero” years if you plan to retire earlier than 65. That will give you a more accurate estimate of your CPP benefits.

Remember that you will always get more CPP by waiting, even if you retire early. Your calculated age-65 CPP benefit may decrease, but that will be more than offset by the age-adjustment factor or deferral credit (7.2% per year from 60 to 65, and 8.4% per year from 65 to 70).

Disclaimer: If at any time you stopped work to raise kids or recover from a disability, or you have been widowed, divorced or separated then the CPP Calculator will not provide you with an accurate calculation. It is recommended that you have your benefit amount manually calculated by Canada Pension Plan expert Doug Runchey, who charges a nominal fee but guarantees the accuracy of your estimate.

In previous articles I’ve looked at reasons to delay taking CPP until age 70, along with explanations why you might want to take CPP earlier at age 60. But in this article I’m going to explain why you shouldn’t take CPP at age 65.

The most compelling reason to defer CPP is the increase or enhancement of your benefit – 0.7% for every month you delay past 65. Wait until age 70 and you’ll receive 42% more CPP than if you took it at age 65. Taking CPP early can also be an attractive option for those with a reduced life expectancy or for those who simply need the money right away.

Once you’re close to age 60, Service Canada will mail you an application form, along with an estimate of your CPP benefits. Curious, since this behavioural “nudge” may influence you to take CPP early at a reduced rate, rather than waiting until the standard retirement age of 65.

Finding out the optimal age to take CPP requires a break-even analysis and depends on a number of factors, including how much you’ve contributed and for how many years, plus a guess on how long you’ll live. Also playing a role is your current and future tax bracket, your income needs now versus in the future, plus the impact that taking CPP early has on means-tested benefits such as GIS and OAS.

What’s interesting about the break-even analysis for CPP is that the standard retirement age of 65 is never the optimal age. Let me explain:

Why Not Take CPP At Age 65?

In I post I wrote years ago about taking CPP early or late, Canada Pension Plan expert Doug Runchey shared with me the interesting fact that taking CPP at 65 is never the optimal choice from a payout perspective.

Indeed, Aaron Hector, a financial planner at Doherty & Bryant Financial Strategists, expanded on that fact with an interesting analysis on optimal CPP starting ages.

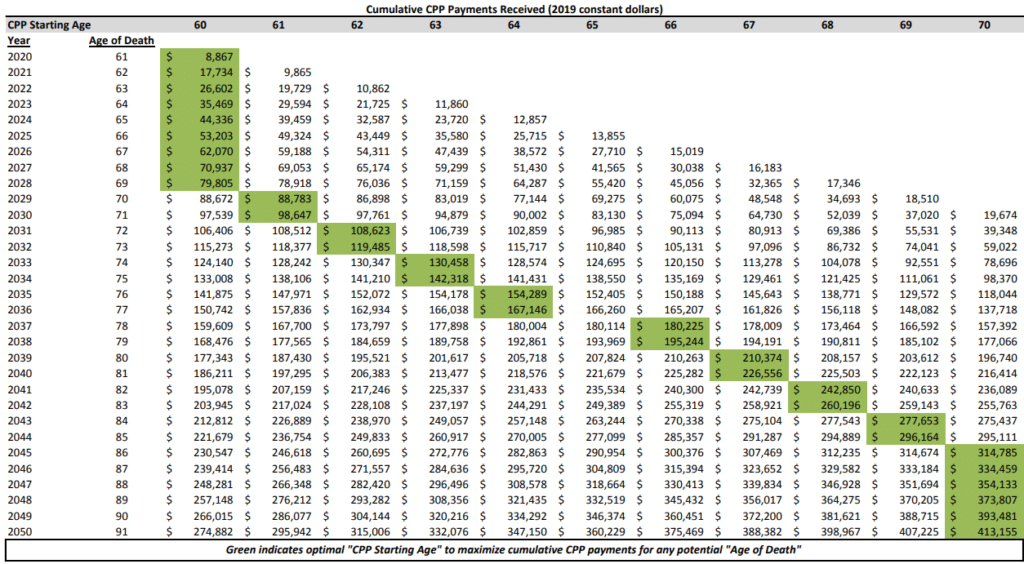

Hector looked at two scenarios; one in which the retiree spends all of his or her CPP benefits, and one in which the retiree invests their CPP and earns a 3% real return after taxes.

What he found was that taking CPP at age 60 was best for those who live only until age 69 (when CPP was spent), or until age 71 (when CPP was invested). Taking CPP at age 70 was optimal for those who live until age 86 and beyond.

As you can see, age 65 is never the optimal starting age to take CPP. That said, you could argue that 65 is the sweet spot between the two extremes of taking CPP early or late.

It’s helpful to know that the normal life expectancy at 60 for a Canadian is 25 years. So, if you don’t have any reason to believe you’ll have a shorter or longer life expectancy then 85 is a good age to use as a benchmark for your own break-even analysis. In this case, the optimal age to take your CPP payments and receive the most money is age 69.

Taking CPP early and investing

There’s a mindset among some retirees that they should take CPP as soon as possible and invest. The idea being that the longer their investments can compound, the better off they’d be versus delaying CPP beyond age 65.

But Hector’s analysis should put a damper on any expectation that taking CPP early and investing will lead to a better outcome. This could be due to overconfidence in one’s investing ability, over over-optimism about the expected rate of return. In any case, as you’ll see below, taking CPP at 60 and investing the entire amount only improves the optimal outcome by two years.

It’s hard to beat a guaranteed 7.2% a year increase in CPP benefits just by delaying your application. There’s also a practical argument against this approach. Is the object of the game to amass the largest bank account before you die? Or is it to spend and enjoy what you worked so hard to earn in retirement?

In my mind, it’s not a rational argument that a retiree will invest every single dollar of CPP benefits. At some point we’re going to spend our money.

Final thoughts on taking CPP at 65

The standard retirement age of 65 is embedded in our society and triggers most Canadians to take their CPP benefits at that age – like a rite of passage for retirement. But what I’ve explained here clearly shows that it’s never optimal to take CPP at age 65, from a purely financial perspective.

If anything, this analysis and research should at least give us pause before automatically applying for CPP at age 65. Look at your family history – are they leading long and healthy lives, or is there a trend of illness or disease? Beyond that, what kind of shape are your finances in today? Where will your retirement income streams come from? Do you fear you’ll outlive your money?

All of these questions should play a role in your decision as to whether to take CPP early, late, or somewhere in-between.

Our net worth crossed the million-dollar mark at the end of 2020, but that included about $300,000 in home equity. This week I noticed the total amount we had invested across our RRSPs, corporate account, RESPs, and my LIRA had surpassed the $1M threshold for the first time. We’re managing a million dollar portfolio!

- RRSP – $331,400

- LIRA – $219,900

- RESP – $112,000

- Corporate – $372,000

- Total = $1,035,300

I started my DIY investing journey back in 2009 with about $25,000 from a group RRSP at a former employer. I bought a handful of dividend stocks and thought I was pretty, pretty, pretty good at this whole investing thing.

Little did I know that a rising tide lifts all boats and my stocks just happened to be soaring because the entire market was on fire coming out of the depths of the global financial crisis.

While it was cool to see a 30%+ return on my investments that year, the growth meant little due to the tiny size of my portfolio. In fact, my own savings contributions added more to my portfolio balance than market returns did that year.

Indeed, in the beginning your savings rate matters the most. Contributing $10,000 to a $25,000 portfolio makes a bigger impact than earning a 10% return on that same investment ($2,500).

Fast forward 15 years and more than $1M later, and market movements have a much larger effect on our portfolio balance. Now, a 10% gain on our investments means growth of $100,000 (although the reverse is true as well).

The stakes are much higher now, and there’s more room for error. That’s why I’ve largely removed my own judgement and decision making from our investment management.

No more picking individual stocks or trying to guess which sector, country, or region will outperform. Just buy the entire global market for as cheap as possible and move on with my life.

Related: How I Invest My Own Money

The beauty is that it’s a strategy you can embrace whether your portfolio is worth $25,000 or $2,500,000.

This Week’s Recap:

In the last edition of Weekend Reading I explained the federal government’s proposed changes to the capital gains inclusion rate, which will move from 50% to 66.67% inside of corporations and trusts, while remaining at 50% for the first $250,000 of personal capital gains and then moving to 66.67% of the gains in excess of $250,000.

From the archives: Here are eight overlooked ways to save taxes in retirement.

Our mortgage renewal at Pine Mortgage is almost complete and should be in place this week. So far, so good with Pine – so if anyone’s in the market for a new mortgage just let me know and I can pass along our contact.

Promo of the Week:

With all of my credit card wheelings and dealings (and with us in the market for a new mortgage lender) I tend to keep a close eye on my credit score.

I’ve seen it dip below 700 after a credit card sign-up spree (13 cards in one year), and reach as high as 820 thanks to diligent bill paying, low credit utilization, a long history, and no new inquiries.

My credit score was 804 when I last checked before switching mortgage lenders. It dropped 30 points after that hard inquiry and one new credit card sign-up (I couldn’t help myself!).

Your credit score can vary widely depending on when you check, and with whom.

I get my Equifax credit score for free from Borrowell. It won’t affect your credit score and Borrowell uses bank-level encryption to ensure your information stays safe. Get your free credit score here.

Weekend Reading:

Preet Banerjee’s latest Globe and Mail column argues that biases around house-rich cash-poor homeowners are impacting financial planning for retirement. What is your home equity release strategy?

On Kiplinger, here are five ways to make retirement a little less scary:

The most important thing about retiring “to” something is that you know who you are. Remember: “Retired” says only what you don’t do. Make sure you know what you do do.

Happy 71st birthday! You now must convert your RRSP into a RRIF. Here’s what you need to know.

Like me, Jonathan Clements is forever an optimist and not scared of bears (bear markets, that is). But the future isn’t limited to two alternatives, either continued economic growth or economic apocalypse.

Investors in ARKK have experienced dramatic ups and downs, with an emphasis on downs for most investors. The question anyone still holding these funds must be asking – or should be asking – is whether it will recover:

I like this idea from Michael Kitces about reframing retirement risk away from Monte Carlo style success/failure and towards over-or-under-spending:

The Monte Carlo success/failure framing, in essence, focuses only on minimizing the risk of overspending, hiding a bias towards underspending by calling it a “success”. Or, put another way, a 100% probability of success is exactly a 100% probability of underspending.

Tomas Pueyo shares why he doesn’t invest in real estate and explains why real estate won’t continue to go up forever.

A Wealth of Common Sense blogger Ben Carlson explains why convenience is a form of wealth.

Finally, a loyalty points lesson on why credit card reward charts rarely provide good value for economy class flights to Europe.

Enjoy the rest of your weekend, everyone!