It isn’t what we say that makes a difference in the world. It’s what we do.

There has been high interest and significant growth in socially responsible investing – also known as ethical investing – especially among younger investors and women.

But, even though the trend is growing, it’s not new.

Socially responsible investing has existed since the 1700’s when religious groups such as the Quakers avoided “sinful” investments such as those participating in the slave trade.

More recently, in the 1960s – 1970s, investors were mainly concerned with contributing to causes such as women’s rights, civil rights and the anti-war movement.

Between the 1970’s and 1990’s, companies, pension funds, and individuals stopped investing in South Africa due to apartheid – racial segregation and other human-rights violations. Socially responsible investing was used as a tool to dismantle apartheid in 1994.

Currently, awareness has grown over global warming, climate change, and human rights.

Is socially responsible investing the right choice for you?

Modern ethical investing has become more complex because there are hundreds of investment products and fund managers putting their interests towards a wide spectrum of social issues.

Many socially responsible fund managers rigorously screen their holdings and avoid businesses involved in tobacco, alcohol, gambling and the development of weapons. “Green” investing focuses on environmental protection.

Nearly every major financial institution offers socially responsible funds, as well as mutual funds companies such as Phillips, Hagar & North. Some products are available for purchase through a discount broker. Others are only purchased through financial advisers (Ethical Funds).

Do your research

Don’t be sidetracked by the word “sustainability” in a fund’s name or description. A check of a couple of popular sustainable funds showed little difference between them and their regular counterparts. For instance:

RBC Janzi Canadian Equity Fund (RBF302)

Holdings: 36% financials, 18% energy, 46% other

Top ten holdings: RBC, TD, BNS, CNR, Suncor, Brookfield Asset Mgmt, BMO, Canadian Natural Resources, Manulife, BCE

MER: 2.09%

Returns:

RBC Canadian Equity Fund (RBF269)

Holdings: 39% financials, 21% energy, 40% other

Top ten holdings: RBC, TD, BNS, Suncor, Canadian Natural Resources, CNR, BMO, Brookfield Asset Mgmt, Enbridge, TransCanada Corp.

MER: 2.06%

Returns:

iShares Jantzi Social Index ETF (XEN)

Holdings: 34% financials, 17% energy, 49% other

Top ten holdings: RBC, TD, CNR, Suncor, BMO, BCE, CIBC, CPR, Telus, Sun Life

MER: 0.56%

Returns:

iShares Core S&P/TSX Capped Composite Index (XIC)

Holdings: 35% financials, 20% energy, 45% other

Top ten holdings: RBC, TD, BNS, CNR, Suncor, BMO, BCE, Enbridge, TransCanada Corp, Canadian Natural Resources

MER: 0.06%

Returns:

If you want to invest in companies that follow environmental sustainability, social responsibility and corporate governance (ESG), you should do your own research.

Check Sustainalytics, an investment research firm that provides research on different companies and countries. For a mutual fund or ETF evaluation, Morningstar rates how well the companies held in over 2000 funds are managing their ESG risks and opportunities.

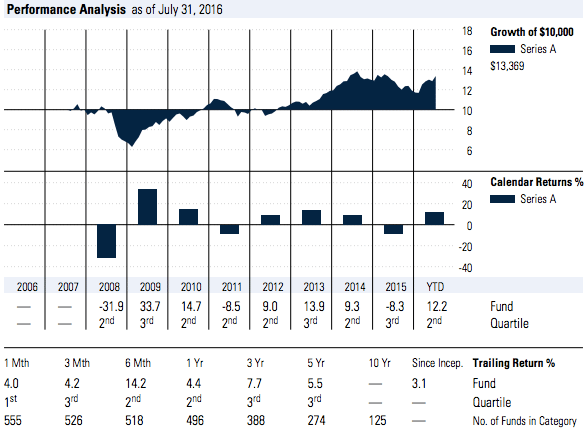

How are the returns on SRI funds?

The bad news with socially conscious investments is that they’ve had a history of poor returns. They don’t produce nearly the same returns as their unethical counterparts.

For decades, investments such as the Barrier Fund (formerly the Vice Fund) which invests in companies involved in defense, gaming, tobacco and alcohol, have significantly outperformed benchmarks such as the S&P 500 and all ethical funds.

But, don’t avoid socially responsible investing because of poor returns. The key, as in other investing, is to judge the company and fund as an investment first and not become so enamoured by its social responsibility record that you can’t see whether or not it is over-priced.

High fees can eat up more of your portfolio than underperforming markets. Understand what you’re paying and whether it’s worth it to you.

An investor must still assess the financial outlook of any investment. Give thoughtful consideration to the investment’s history, management, and future direction.

Final thoughts

Many investors believe that social responsibility should be a primary consideration in making investment decisions.

The good news is that the Canadian socially responsible funds market has been gaining increasing momentum and influence over the past few years. This increase can be attributed to large pension funds adopting new social and environmental screening policies.

Even robo-advisors such as Wealthsimple and ModernAdvisor have designed portfolios specifically around socially responsible investing.

If this is an investment strategy you want to pursue, begin by examining your own personal values and what you consider ethical and unethical. Follow your own guidelines to make the most meaningful use of your money.

Socially responsible investing is about choosing to make a financial commitment to your conscience and investing where you feel your money is the most useful.

Try to balance your social concerns with long-term results.

I consider my financial freedom 45 plan to be aggressive, yet attainable. Reaching financial independence at a relatively young age requires discipline, sacrifice, and a lot of savings mixed in with a dash of frugality. But my plan pales in comparison to certain members of the financial independence / early retirement crowd who aim to leave the workforce in their early-to-mid thirties.

That’s the story behind CBC’s profile of Kristy Shen and Bryce Leung, authors of the Millennial Revolution blog. The couple ditched the idea of home ownership in pricey Toronto and instead used the $500,000 they saved to pursue their own idea of financial freedom – travelling the world and working on projects that inspire them.

Much like Sean Cooper, who paid off the mortgage on his Toronto home in three years, Kristy and Bryce drew the ire of readers who criticized the couples approach as ‘selfish’.

In a strange twist it turns out their financial advisor is notorious Canadian housing bear Garth Turner, who says he’s now fielding a bunch of phone calls from Millennials who are looking join the Millennial Revolution. There’s only one problem:

“I don’t create millionaires out of latte-sucking entitled kids craving retirement and work-life balance. Stop calling.”

Money Boss J.D. Roth, who achieved financial independence when he sold his Get Rich Slowly blog for millions, says we should be celebrating these success stories, not denigrating them.

“This young couple made some out-of-the-box choices. They acted as money bosses. The decision paid off. Sure, they enjoyed good fortune with their investment results, but so did many of us from 2010 to 2014. This couple’s story ought not be unique; it ought to have been the norm for personal investors during that time span.“

A Wealth of Common Sense blogger Ben Carlson weighed-in on what it takes to retire early. He says you either need to save lots of money or have very little need for lots of money.

“Unless you inherit a boatload of money, there really is no secret for early retirement. There are no life hacks that will make it easier. It takes sacrifice and it’s certainly not for everyone.”

Perhaps what some of us really need is to give ourselves permission to make a big life change. We’re too cautious when it comes to big changes, but studies show that we’re generally happier when we take a leap of faith. That’s why Carl Richards is taking his family to New Zealand to live and work for the next 12 months.

This Week’s Recap:

On Monday I explained why I chose a 2-year fixed rate mortgage.

On Wednesday Marie wrote about the dollar store boom and what items cost less at places like Dollarama.

And on Friday I explained why University students should probably get a credit card.

Many thanks to Josh O’Kane for including my advice in his Globe and Mail column about whether to pay off student loans or save for a downpayment.

Weekend Reading:

These Money Pros liked how I acted as my own mortgage broker and shopped around before negotiating renewing with my existing bank.

The case against home ownership? Rob Carrick interviews an author who says renting is a beautiful thing.

Death to the single family home? A UBC sociology professor says single family homes are overrated and harmful to health of the city.

This blogger says debt motivates her in a way that savings never could.

Here’s how to cut your phone bill (and your clutter).

The latest Carrick Talks Money: How can I tell how good my workplace pension is?

Two Alberta men turned their layoffs into opportunities, each creating their own business.

Tim Cestnick explains four ways to transition out of business ownership.

What investors need to know about the active versus passive management debate.

This scoreboard may have you thinking twice about holding actively managed funds.

A classic math vs. behaviour decision. Investing a lump sum – should you do it all at once or over time?

Jon Chevreau on why he won’t defer his OAS past age 65.

It’s harder now to save for retirement – so we have to invest smarter.

Frugal Trader answers a reader question: I have $1M networth – what’s next?

Adam Mayers talks to one driver who received a $600 car insurance surprise.

The Greedy Rates blog shows how to increase your credit card rewards by ‘stacking’ two cards.

Finally, Squawkfox blogger Kerry Taylor is known for making frugality and consumer savvy sexy, delicious, and fun. She’s also battling depression and wrote a courageous post after her psychologist asked if there were any positives that came from her depression. Thanks for writing this, Kerry.

Courage, it couldn’t come at a worse time.

Enjoy your weekend!

As students head back to university this fall, one question is whether or not to get a credit card. They probably should. Credit cards are practical and useful and managing them is a fact of life. So the sooner young adults learn to use one responsibly and begin building a credit history, the better.

There are advantages to getting a card before the student arrives on campus because it avoids the pressure of a campus kiosk. It also gives students a chance to talk about credit with their parents and allows plenty of time to ask the right questions of lenders.

Worried parents who are asked to co-sign can keep the credit limit low until they’re confident their child can handle it.

The best deal for students is a credit card that has no annual fee and rewards each purchase with cash back or discounts on things they need. The rewards should be useful, though: earning points toward a new car or a fabulous holiday might sound good, but chances of spending enough to earn the points are out of reach for most students. You’d have to spend far beyond your means to get the reward.

All the big banks offer student cards, but BMO, Scotiabank, MBNA (owned by TD), and RBC have the best deals. The cards all offer a number of similar features. Most have a high interest rate, but come with no annual fee and the chance to earn rewards.

BMO SPC Cashback MasterCard

One student credit card that stands out is BMO’s SPC Cashback MasterCard. It gives 1 percent cash back with every purchase, plus offers discounts at hundreds of retailers. The SPC program offers up to 15 percent off at places such as Boston Pizza, Gap and First Choice Haircutters.

Students will likely start off with a $500 credit limit with the chance for an increase if they keep their account in good standing. Earn $30 cash back on $3,000 a year in spending, plus all the other SPC benefits are included free (the SPC card bought on its own costs $10). For a limited time you’ll get a $60 cash welcome bonus when you sign up for the card.

Scotia SCENE Visa

Scotiabank’s SCENE Visa card also fits the bill as a no-fee credit card that offers useful rewards for students. Get one SCENE point for every dollar spent on the card, and 5 SCENE points for every dollar spent at Cineplex theatres or on Cineplex.com.

Apply before October 31st and get 4,000 bonus points on your first purchase — good enough for four free movies at Cineplex.

Related: Why SCENE rewards is one of Canada’s hidden gems

MBNA Studentawards MasterCard

MBNA’s Studentawards MasterCard is another option for students. Earn 1 percent back with each purchase, plus 1,000 bonus points on your first purchase and another 1,000 points each year on your card’s anniversary.

Spending $3,000 a year will get you $50 back in the first year and $40 a year thereafter.

Avoid annual fees

Student credit cards that come with an annual fee should be avoided, no matter what kind of perks they include. Students simply don’t spend enough for the rewards to offset the fee.

For example, RBC’s Signature Rewards Visa gives you 1 percent cash back, but the $39 annual fee will wipe out all of your earnings and then some. Note that RBC student banking customers can get this card free.

A better option is RBC’s Cash Back MasterCard, which is a no-fee card that pays up to 2 percent back on grocery purchases and up to 1 percent back on everything else.

Final thoughts

While credit cards are a necessity for many students, first-time credit users need to manage their spending carefully. Carrying a balance, even for one month, can lead to major debt problems down the road. Trust me, 19.9 percent interest compounds quickly!

Students need to understand that credit cards should be used for purchases that can be paid off each month and they should not abuse their credit limit. Putting recurring expenses, such as a cell phone bill or Netflix subscription, on your credit card while making sure to pay the balance in full every month is a great way to establish credit history and learn some financial responsibility.