We’ve all had times when we’ve dreamed about our eventual retirement when we’ll have all the free time available to pursue whatever we want to do. We don’t have the time to do everything while working full-time, so we have a long list of things we’d like to do later on.

But why wait until you retire? Here are five things you shouldn’t put off until retirement.

1. Travel

Travel is often number one on the list of activities people want to do when they retire. They will finally be free to see the sights they’ve dreamed of all these years.

But, why not make plans to go on that long awaited trip now? Travelling with your family can create a bond and memories that last a lifetime.

Many travel experiences are easier when you’re younger – and cheaper too.

Related: How to visit Europe on a budget

It’s much more difficult to travel when you have certain health conditions and physical limitations. Even if you’re still healthy and in great shape you probably won’t have the same level of energy and endurance.

Older people tend to want more comfort – and that can be costly. You may not have the money if your portfolio takes a downturn, or living expenses are higher than expected.

2. Downsize your home

One way to trim expenses is to sell your oversized home and move to a smaller, more efficient place now rather than waiting for retirement. Relocating to a more affordable area is also a great option. If your kids are out of the house, you don’t need the extra space, and costly home maintenance it taking over your weekends, why not downsize now?

Check out “active living” or “adult lifestyle” communities where ownership starts as low as age 45.

Not only can this slash your housing costs now, it’ll free up cash for you when you finally do retire.

3. Exercise

Exercise is one activity that’s typically put off when we’re busy, but lack of exercise is a major cause of many chronic diseases that we can become susceptible to when we age. Incorporating an exercise program of at least 30 minutes a day leads to a healthier lifestyle once you retire.

Retired life will be more enjoyable if you’re not dealing with health problems, and medical expenses can be greatly reduced.

4. Living on a reduced budget

Once your major expenses of children and home mortgage have disappeared, why not start living within your future means with a reduced budget that would reflect your lower retirement income?

Run the numbers. You can determine a realistic view of your cash flow and be prepared to make significant changes if you need to.

5. Hobbies

People tend to put off their hobbies and personal interests. They have a low priority when you’re busy with work.

Try out new hobbies or other activities to see if you find them enjoyable before you jump in whole-hog at your retirement.

If you wait you may find some activities harder to master.

Barry had always been interested in fine woodworking and was looking forward to this new hobby once he retired. But, as he got older, his eyesight started to deteriorate so he was no longer able to see the fine detail work clearly. He became frustrated and quit.

Final thoughts

Don’t postpone your life until you retire. Making retirement your lifelong primary goal could end up in disappointment once you get there.

Make the best life you can right now and at retirement you’ll have a different kind of fun.

Charitable giving is often an important part of a sound financial plan. In fact, philanthropy is one of the top four characteristics of wealthy people (the others are – spending wisely, investing for the future, and having multiple streams of income).

Many people have a cause they care deeply about – specific charities, research organizations, educational institutions, amateur athletics, animal shelters, etc. Charitable giving is a great way to make a difference.

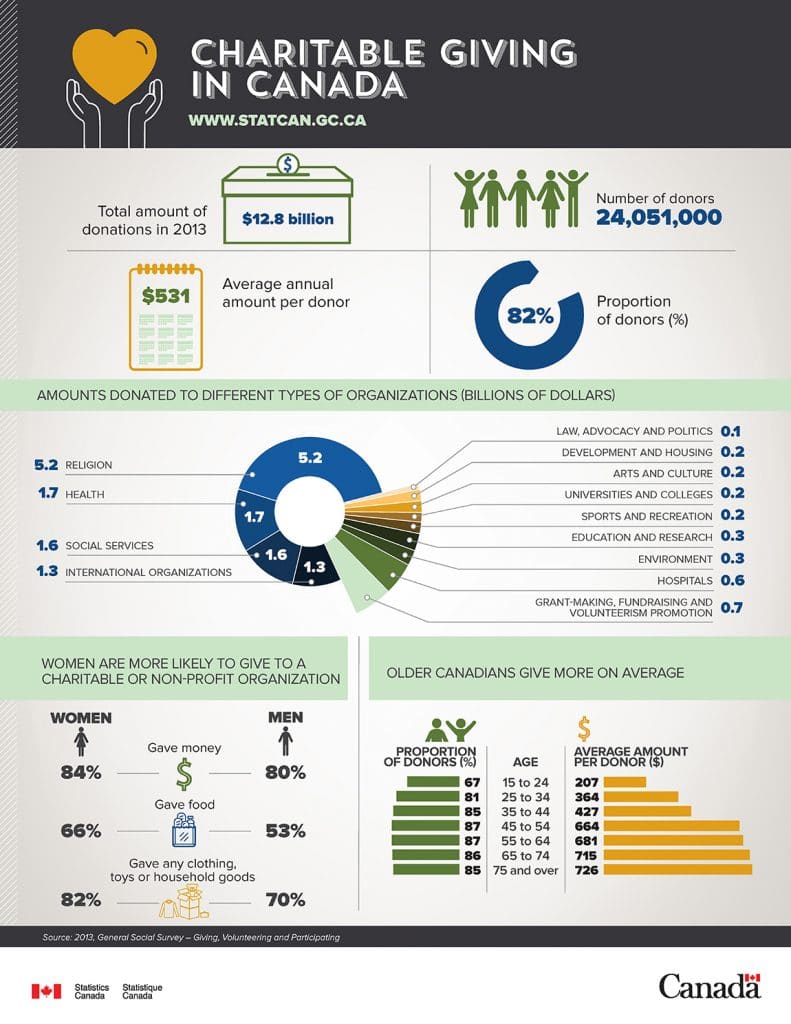

Charitable Giving in Canada

Giving can often be a challenge when money is tight. But, philanthropy is not just about giving money. You can give away unwanted items from around your house. Many people give goods such as toys, clothing, furniture, and food. In general, don’t expect a tax receipt for these donations. You may, however, be able to get a receipt for more valuable items.

People often drop a few coins into a collection jar at the cash register, or buy cookies, chocolate covered almonds or various other items as part of a fundraiser.

Volunteering is another form of donation. According to an Ipsos Reid survey, 25% of Canadians say they volunteer at least four hours a month.

Tax advantages

Donations to a registered charity are eligible for both federal and provincial tax credits for up to 75% of your net income for the year.

The federal tax credit is 15% for the first $200 and 29% for donations over $200. Provincial tax credits vary by province. The credit can be claimed by either spouse, or can be split. It can also be delayed and claimed in any of the five years following the one in which you donated.

A number of tax incentives have been introduced to encourage giving:

- There is a new high-rate for the federal tax credit of 33% for taxable income over $220,000 in 2016, which applies to donations made in 2016 or later.

- First time donors can claim an additional 25% “super tax credit” on the first $1,000 they donate, which supplements the usual tax credit. Only donations of money qualify. This credit is temporary and will not be available after 2017.

- There can be significant advantages to donating marketable securities as opposed to cash. In this case, the CRA will not tax capital gains.

Planned giving

The eligible donation for tax credits is 100% of net income in the year of death and the preceding year and is claimed on the final return.

Related: Leave a legacy before the will is read

Donations can be bequeathed in a will, or a person could designate a qualified charity as the beneficiary of an RRSP, RRIF, TFSA, or life insurance policy.

Final thoughts

There are a lot of good reasons to make donations to charity, but the simple fact is that giving makes you feel good. Many studies have shown that charitable giving creates greater satisfaction and happiness.

What do you think?

I was 19 years old when I first started investing. I diligently set aside money every paycheque, starting with $50 every two weeks and eventually increasing that to $200 per month, to save for retirement inside my RRSP. Sounds like I was off to a great start, right? Wrong!

Even though my intentions were in the right place, my first attempt at investing was a complete disaster. Here’s why:

I didn’t have a plan

It’s good practice to save a portion of your income for the future, even at a young age. The problem for me was that I was still in school and didn’t have a plan – I had no clue what I was saving for.

I had read The Wealthy Barber and The Millionaire Next Door and so I knew the earlier I started putting away money for retirement, the longer I’d have compound interest working on my side, and the bigger my nest egg would be.

Unfortunately, I was saving for retirement at the expense of any other short-term goals, like paying off my student loans, buying a used car, or saving for a down payment on a house.

I didn’t have any short-term savings

Speaking of RRSPs, what was a 19-year-old kid doing opening up an RRSP when he’s only making $15,000 per year?

There were no real tax advantages for me to save within an RRSP when I was in such a low tax bracket. I’m sure I blew my tax refunds anyway, so what was the point?

Granted, the tax free savings account hadn’t been introduced yet, but I would have been better off using a high interest savings account for my savings rather than putting money in my RRSP.

I didn’t have a clue about fees and tracking performance

Like a typical young investor I used mutual funds to build my investment portfolio. I was encouraged by a bank-advisor to select global equity mutual funds because, as I was told, they would deliver the highest returns over the long term.

What the bank advisor didn’t tell me was that the management expense ratio (MER) on some of those mutual funds can be 2.5 percent or more, and high fees will have a negative impact on your investment returns over the long run.

Bank advisors also don’t tell you which benchmark these funds are supposed to track (and attempt to beat) so when you get your statements in the mail it’s impossible to determine how well your investments are doing compared to the rest of the market.

I drained my RRSP early

I didn’t have a good handle on my finances in my 20’s and often resorted to using credit cards to get by. Without a proper budget in place, and no short-term savings to fall back on in case of emergency, I had no choice but to raid my RRSPs to pay off my credit card debt and get my finances back on track.

Taking money out of my RRSP early meant paying taxes up front. Withdrawals up to $5,000 are subject to 10 percent withholding tax, while taking between $5,000 and $15,000 will cost you 20 percent, and withdrawals over $15,000 will cost you 30 percent.

Your financial institution withholds tax on the money you take out and pays it directly to the government. So when I took out $10,000 from my RRSP, the bank withheld $2,000 and I was left with $8,000. In addition to the withholding tax, I also had to report the full $10,000 withdrawal as taxable income that year.

While I can’t argue with my reasons for selling, my dumb decisions beforehand cost me a lot of money and left me starting over from scratch.

Final thoughts

We all make investing mistakes – some bigger than others. If I had to do things over again today I would have done the following:

- Create a budget – A budget is the foundation for responsible money management. Had I used a budget and tracked my expenses properly from an early age I would have lived within my means and kept my spending under control.

- Open a tax free savings account – Yes, the TFSA wasn’t around back then but for today’s youth it makes much more sense to save inside your TFSA instead of your RRSP like I did. You can put up to $5,500 per year inside your TFSA and withdraw the money tax free. You contribute with after-tax dollars, so you won’t get a tax refund, but you’ll likely be in a low tax bracket anyway, so contributing to an RRSP won’t give you much of a refund either.

- Make a financial plan – We all have financial goals and even at a young age I should have identified some short-and-long term priorities to save toward. I’d take a three-pronged approach where I’d use a high interest savings account to fund my short term goals, my TFSA to fund mid-to-long term goals, and eventually open an RRSP to save for retirement. No doubt I’d be much further ahead today if I took this approach earlier in life.

- Use index funds or ETFs – Now that I understand how destructive fees can be to your portfolio, I’d look into building up my investments using low cost index funds or ETFs. The advantage to using index funds is that you can make regular contributions at no cost while achieving the same returns as the market, minus a small management. Some brokers also offer free commissions when you purchase ETFs.

Did you make similar mistakes when you first started investing? How did you overcome them?