We’ve reached the halfway point of 2016 so it’s once again time to take a deeper look at my finances and update my net worth.

This year has been fairly quiet on the financial front. I continued to simplify our investments, this time by transferring a small RRSP account from Tangerine over to our TD Direct account where the rest of our investments are held.

Paying down our line of credit remains a top priority. I’m also counting the days until our car is paid off (three more months!) so we can allocate those dollars towards our TFSAs.

My main frustration is that I haven’t seen a raise in three years. Unfortunately it looks like that trend will continue into 2017. That means more pressure to ramp up efforts with our online business so that we can withdraw enough income to at least keep up with cost of living increases.

That said it’s satisfying to still be on track with our financial goals despite it being years since I’ve seen any significant salary growth.

Here’s a look at the numbers:

Net worth update: 2016 mid-year review

Total Assets – $738,605

- Chequing account – $1,500

- Savings account – $5,000

- RRSP – $118,866

- Defined benefit plan – $138,845

- TFSA – $4,359

- RESP – $20,035

- Principal residence – $450,000

Total Liabilities – $261,934

- Mortgage – $242,947

- Home equity line of credit – $18,987

Net worth – $476,671

A few questions that I often get asked after posting a net worth update:

Banking

We funnel all of our spending onto the Capital One Aspire Travel World Elite MasterCard. The card pays 2 percent back on every purchase and its new no more tiers redemption program makes it easy to cash in points.

We have no-fee chequing accounts at Tangerine, which we use for bill payments, email money transfers, and the odd debit purchase.

The rest of our banking is done at TD, including our mortgage, line of credit, and investments.

Pension

Each month I contribute roughly 12 percent of my salary to a defined benefit pension plan that my employer matches. The amount listed above is the commuted value of the pension if I were to leave the plan today.

The plan pays 2 percent of your highest average salary multiplied by the number of years worked. So that means if I retired at 60 with an average salary of $100,000 I’d receive $60,000 per year from the pension plan.

RRSP / RESP

The right way to calculate net worth is to use the same formula consistently over time to help track and achieve your financial goals.

My preferred method is to list the current value of my RRSP and RESP plans rather than discounting their future value to account for taxes and distributions.

I consider a net worth statement to be a snapshot of your current financial picture, so when it comes time to draw from my RRSP and distribute the RESP to my kids, net worth will decrease accordingly.

Principal residence

We bought our home nearly five years ago and, even though the market has gone up, I’ve continued to list the value at purchase price. Last year I factored our basement renovation into the equation and increased our home value by $25,000.

Final thoughts

I check in on my overall financial health twice a year to make sure I’m still on track to meet my goals – both short and long term. There are a few big picture goals in mind:

First, I want our net worth to surpass $500,000 by the end of the year. Second, I want to hit the million-dollar mark by the end of the year in which I turn 41 (2020). And finally, I want to become financially free by 45.

To me financial freedom means no more mortgage payments, or other debt obligations, and the income earned from our online business and personal investments exceeds our living expenses.

We’re on track to reach these goals and I can’t wait to get there!

Happy Canada Day weekend! We spent Friday exploring the beautiful Waterton Lake area and took a boat cruise across the International border to Goat Haunt, Montana.

Canada and the U.S. have an interesting way to separate their borders along the 49th parallel – by clearing a section of forest 10 feet on either side of the dividing line:

Canada Child Benefit

This month the federal government will officially replace monthly UCCB and CCTB payments with the new Canada Child Benefit, a tax free monthly payment for parents with children under 18 years of age.

The first CCB payment will be made on July 20th and parents can use Canada Revenue Agency’s child and family benefits calculator to determine their monthly payment amount.

The government claims 9 out of 10 Canadians will receive more money under this program and that is certainly true in our case as we’ll receive an estimated $115 more per month than we did under the previous program (and, it’s tax-free!).

T.E. Wealth has compiled 4 key planning points to consider with the new Canada Child Benefit. It’s definitely worth a read.

This Week’s Recap:

I reached out to seven travel experts to answer a very specific question from a reader: How would you spend 52,436 Aeroplan miles? Check out some of the great tips and advice on how to make the most of your travel points.

On Monday I described the right way to calculate net worth. Look for my mid-year net worth update tomorrow.

On Wednesday Marie continued her series on financial planning for couples with a look at how couples should deal with debt.

And on Friday I talked about Brexit and the impact it has on your investment strategy (hint: none).

We’ve put together a free eBook on how to manage your money at any age and stage – from teen years all the way until your 70s. Click here to download your free copy.

Weekend Reading:

The youngest employee in a 50-person department dishes some straight-talk to Millennials on retirement.

This Quartz article argues that the myth of Millennial entitlement was created to hide their parents’ mistakes.

Kyle Prevost from Young & Thrifty put together a great resource with the complete guide to Canada’s best online banks.

Tangerine launched its Moneyback credit card this year and has opened over 75,000 credit card accounts. Here’s an in-depth Q&A with Scott Lapstra, Tangerine’s head of credit cards.

Can the marriage between a saver and spender possibly last? Rob Carrick and Leslie Scorgie explain how to get on the same page:

What are these new financial regulations everyone is talking about? Wealthsimple explains everything you need to know about CRM2.

In addition to CRM2, Canadian regulators are also looking at the possibility of banning mutual fund trailer fees as early as this fall.

The Economist describes the slow-motion revolution and why the rise of low-cost managers like Vanguard should be celebrated.

Morgan Housel explains what to do when stocks give you nothing.

Mark Seed looks at the crossover point for investors – or when your investment income meets or exceeds your monthly expenses.

Jason Heath with some great advice on RESP investing for your teenager.

Jon Chevreau on how he retired at 60 without ever being rich.

How to pass on the family cottage without destroying your family in the process.

Nothing to see here. The mortgage industry says there’s no housing bubble in Canada.

B.C. Premier Christy Clark says the government is ending self regulation for the B.C. real estate industry:

“The real estate sector has had 10 years to get it right on self regulation and they haven’t,” said Clark

Finally, as home prices climb, taking 30 years to pay off mortgage is becoming new norm in Toronto and Vancouver.

Have a great weekend, everyone!

The long term economic and cultural fallout over Brexit is still very much up in the air. What is crystal clear, however, is that investors, economists, and market pundits overreacted (again) to the news of Britain’s departure from the European Union.

Stock markets took a sharp decline late last week and investors were treated to headlines such as; 5 things investors need to know after Brexit, post-Brexit market strategies Canadian investors should know now, why Brexit could take 10 years (and what investors should do), and the four Brexit outcomes smart investors need to prepare for.

But just a week later and markets are right back where they started before the Brexit vote even happened. Imagine that.

Stocks now higher than they were a week before Brexit. As you were.

— Morgan Housel (@TMFHousel) June 30, 2016

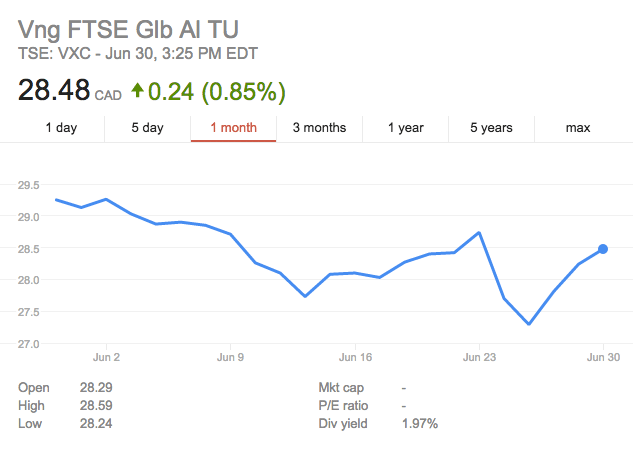

Indeed, when you look at the 1-month chart for Vanguard’s All World ex Canada ETF (VXC) – which holds over 8,000 stocks from around the globe – you’ll see a big drop last week followed by a steady path higher until markets closed Thursday.

I maintain that when faced with the latest ‘shocking’ world event or market turmoil investors would be better off taking a week-long nap instead of acting on the advice of pundits and ‘smart money’. The smart move is to do nothing except stick to your plan.

(And, yes, that includes advice about ‘buying on the dip’. Investors don’t need another reason to make emotional decisions or to become more active with their portfolios).

Buying on a market dip can be good advice, but dips happen all the time. How do you decide when it’s time to buy, and where do you get the money to make these bargain contributions?

Take a look at the 5-year chart for VXC. The Brexit sell-off is barely a blip on the radar, and certainly not the biggest drop in the last five years.

Final thoughts on Brexit

We haven’t scratched the surface of Brexit hot-takes this year. My take is simple: Ignore the noise and stick to your plan. Keep your costs low, broadly diversify across the globe, pick the right mix of stocks and bonds based on your age and risk tolerance, make regular contributions, and rebalance periodically.

Related: Is my two-ETF portfolio too simple?

Notice that none of this advice includes reacting to short-term market moves or Jim Cramer yelling about something on Mad Money. It requires something much harder for investors, and that’s the discipline to do nothing when everyone is screaming at you to do something.