No, I’m not talking about investing in dividend paying stocks. Been there, done that, not going back. I’m referring to paying myself non-eligible dividends from my corporation instead of paying myself a salary.

A quick explanation: My wife and I incorporated our online business back in 2012, while I was still working a 9-to-5 job and Boomer & Echo was just a side hustle. As the business grew, we paid a modest dividend to my wife, who was a stay-at-home mom at the time, and left any remaining funds in the corporation to defer taxes.

Fast forward to 2019 and I quit my day job to focus on financial planning and freelance writing full-time. I took the commuted value of my pension, with the bulk of it going into a LIRA and the remainder paid out as taxable cash. That meant I did not need to take any money out of the business in 2020, while my wife took a small dividend that year.

We paid ourselves an equal amount of non-eligible dividends in 2021 and 2022 to meet our personal spending and savings goals, and to keep our finances simple. But I’ve always wrestled with the idea of whether to pay ourselves a salary, pay ourselves dividends, or to pay a mix of salary and dividends.

The downside of dividends is that you don’t generate new RRSP room, you don’t pay into CPP, and dividends are not a deductible business expense. One further downside is that when we decided to build a new house and apply for a mortgage, our personal income appeared to be much lower than it would have been if we paid ourselves a salary – which may have affected how much we could borrow from the bank.

On the plus side, non-eligible dividends are taxed at a much lower rate than salary. On $80,000 of dividend income I’d pay taxes of about $10,500 this year (13.1% average tax rate). On $80,000 of salary, I’d pay taxes of about $17,100 (21.4% average tax rate). I’d have to pay myself about $90,000 in salary to get the same net pay – and that doesn’t factor in paying the employee portion of CPP ($3,754).

Some business owners consider it a plus not to have to pay into CPP. I disagree. A guaranteed, inflation-protected, paid for life income stream is a wonderful addition to any retirement plan. The trouble is having to pay both the employer and employee portion of an expanding program (costing more than $7,500 per year). If you elect to pay yourself dividends just to opt-out of CPP, you better make sure you have robust savings elsewhere.

My hybrid solution is to pay ourselves a salary up to the CPP maximum ($66,600 this year) and top-up our income with dividends to meet our desired personal spending and savings goals. My plan is to make this switch in 2024, once we get through this complicated year of buying a new house and getting settled.

This Week’s Recap:

Last week I shared the why it’s important to retire with purpose.

Many thanks to Rob Carrick for linking to my tax deductions versus tax credits explainer in his latest Carrick on Money newsletter.

The sale of our house officially went through this week as the buyer’s financing condition was removed. We did it!

Now we have three weeks to get packed and organized for the big move. Fortunately, we have about a week between taking possession of our new house and the new buyer’s taking possession of our house.

Remember, one of my main financial goals for this year was to set aside $50,000 from the sale of our house for landscaping, window coverings, and some furnishings. No “some day, maybes”. That will leave us with about $100,000 in cash, which will either go towards the new mortgage, back into our TFSAs, or a mix of both.

Given where interest rates are today, I’m leaning towards the mortgage.

Promo of the Week:

My DIY Investing Made Easy course shows you exactly how to take control of your own investments by opening your own self-directed investing account, funding the account with new contributions, transferring over your existing accounts, and how to buy an all-in-one ETF that can reduce your investment fees by up to 90% or more.

Nearly every one of my clients who have taken this approach (firing their expensive mutual fund manager and investing in an all-in-one ETF) have told me they were surprised it was so easy to implement.

No more being scared to break up with your advisor. This is your step-by-step guide to moving your underperforming funds over to a self-directed account so you can invest in a globally diversified, risk appropriate, and easy to manage ETF.

Weekend Reading:

Gen Y Money discusses food inflation in Canada and lists some good tips to help stop the bleeding.

Why understanding your money scripts can be key to developing a healthier relationship with money and achieving your financial goals.

Not all loyalty point redemptions are the same. Travel expert Barry Choi explains how to calculate their value.

Deanne Gage lists four overlooked deductions to include in your tax return.

How the ‘tax’ on singles has people who live alone feeling the pinch.

Jesse at The Best Interest blog looks at overconfidence in investing:

“Instead, the “perfectly confident” investor knows how diversification, dollar cost averaging, and staying the course will help them in the long run…but doesn’t try to time the short run.”

Markus Muhs on why the vast majority of investors aren’t going to get rich by constantly jumping into “the next big thing”.

Last Week Tonight’s John Oliver nails this piece on timeshares, including how people get into them and why it’s so difficult to get out:

How to have the most tax-efficient retirement income plan without letting the tax tail wag all of your decisions.

Millionaire Teacher Andrew Hallam explains how much retirees can withdraw from their investments each year.

A first-person account from The Globe & Mail: How do I ‘do’ retirement and find the recipe for a happy, fulfilling life?

Finally, Jonathan Clements shares a wish list for how he’d like to spend his time in his 60s.

Happy Easter, everyone!

Much has been written about the financial side of retirement – do you have enough saved, how much can you spend, will your money last a lifetime? But retirement is part financial and part psychological.

More than just a number in your bank account, retirement is also how you feel about moving on to the next chapter of your life. Indeed, it’s not what you’re retiring from, but what you’re retiring to.

A few weeks ago, financial planner Mark McGrath shared an absolutely gut-wrenching story about his father – a long-time business owner who sold his business, retired, and lost his identity and purpose. The story does not have a happy ending, but Mark felt it was important to share the lessons he learned from this heartbreaking experience:

“We learn about the financial side of retirement but not enough about its emotional and psychological aspects. About how our identities can be intertwined with our careers and our businesses.”

Make sure you know what you’re retiring to.

This was a hard post to write.

I almost didn’t write it in fact. I’ve started and trashed this story many times.

But I believe there are important lessons in this story we can learn from.

Warning: this does not have a happy ending.

— Mark McGrath (@MarkMcGrathCFP) March 14, 2023

The story hit home for many people and has been viewed an incredible 5.1 million times on Twitter. Mark later stopped by the Rational Reminder podcast to talk about the emotional story and why people need to start thinking about retiring with purpose.

I’m grateful that Mark was brave enough to share this cautionary tale as it has forced me to think about my own retirement plans and helped shape conversations I will have with my retired or soon-to-be retired clients.

This Week’s Recap:

You might also remember Mark from this excellent guest post here – 8 overlooked ways to save tax in retirement.

Earlier this week I wrote about building if/then statements into your financial plan.

We had an eventful week – first getting a firm possession date on our new house for the end of April, and then accepting an offer to purchase our existing house.

The timing could not have worked out better, as we’ll have about a week to move and clean-up our house before the new owners take possession.

That beats the last time we moved, when we had to sell early to secure funding for the new house and ended up renting for three months in between.

The financial planner in me has been craving certainty in our situation for more than a year. I can’t wait to get settled in our new house, tally up the final costs, and then get back to our other financial goals – including filling up our TFSAs again and contributing to our corporate investing account.

Promo of the Week:

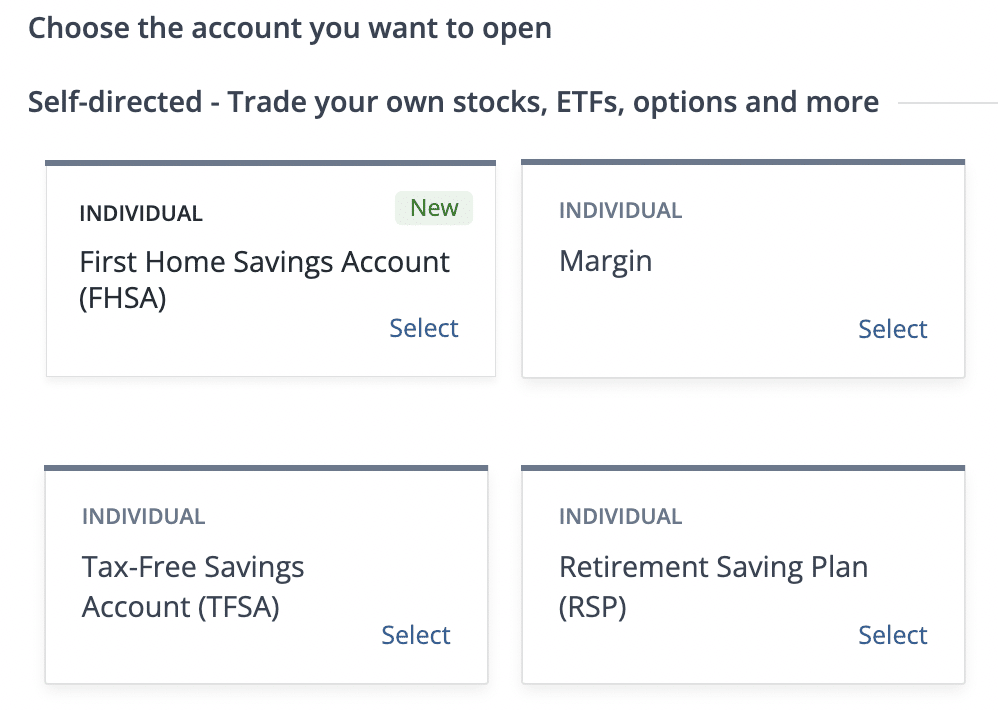

In case you haven’t heard, the new First Home Savings Account launched today. While most banks aren’t ready to administer the accounts yet, Questrade got a head-start on the competition and has the FHSA available to open and fund today.

Remember, the FHSA combines the best of the RRSP (tax deductible contribution) with the best of the TFSA (tax-free withdrawal for a first home purchase). Contribute up to $8,000 per year, to a lifetime limit of $40,000.

Many of my clients have been eagerly awaiting the account to launch, to either use for themselves or to gift money for their adult kids to start saving towards a first home.

Questrade is the first out of the gate if you want to open and fund a First Home Savings Account today.

Weekend Reading:

Speaking of the FHSA, financial planner Anita Bruinsma explains everything you need to know about the new account.

Erica Alini shares how the CRA resuming child benefit clawbacks has some parents scrambling.

An inside look at how the Bank of Canada sets interest rates. A really good read.

I’ve enjoyed Fred Vettese’s Charting Retirement series in the Globe and Mail. His latest looks at whether older retirees should trust their financial judgement:

“The results show that as people age, there is a decline in their ability to make good financial decisions that is not consistent with their own confidence in managing their money. This suggests the need to automate retirement planning as much as possible, especially after 75.”

Canada Pension Plan expert Doug Runchey explains whether it makes sense to contribute to CPP after age 65 if you’re still working.

Why Canadian bank stocks might not be as special as we think.

A Wealth of Common Sense blogger Ben Carlson answers a reader question about consumption smoothing and whether young people should be saving less.

Prompted by french pension protests, economics professor Trevor Tombe answers the question: How secure is the Canada Pension Plan? The answer: Very.

Finally, the always brilliant Morgan Housel compares the Silicon Valley Bank run to fears about the Brooklyn Bridge collapsing back in 1883:

“You never know what the American public is going to do, but you know that they will do it all at once.”

Have a great weekend, everyone!

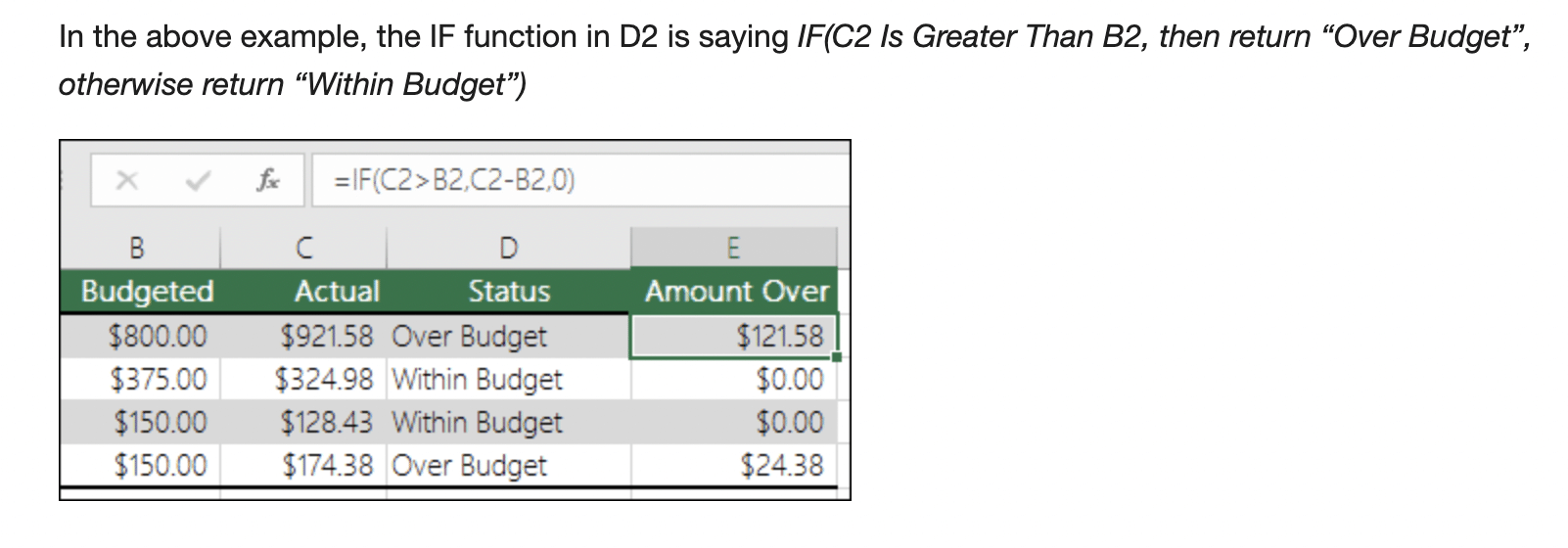

Anyone familiar with Microsoft Excel knows how useful “if/then” statements can be to make comparisons under certain conditions. An IF statement can either be true or false.

An if/then statement can be extremely useful in financial planning. Here are three examples of how to build “if/then” statements into your financial plan.

When your income is variable

Many of my financial planning clients are conservative in their income projections because a good chunk of their compensation comes from a bonus or from working overtime.

I think it’s reasonable to be conservative with your future income projections (i.e. using cost of living adjustments), but you should strive to be as realistic as possible within the current year to help guide your financial decision making.

Adding an if/then statement helps determine how much you can save or spend for the year. For instance, if your income is $100,000 then you might aim to contribute $10,000 to your RRSP. If your income increases to $120,000 due to a bonus, then you might aim to contribute $20,000 to your RRSP.

In reality, you might be saving for more than one financial goal at a time. This is true for most of my financial planning clients.

In many cases, we aim to optimize RRSP contributions at the marginal tax rate, maximize TFSA contributions up to the annual limit, and then prioritize another goal such as extra mortgage payments, saving towards a short-term one-time expense, investing in a taxable account, or increase spending on a fun category like travel or hobbies.

So, here’s an “if/then” statement in action:

If my projected gross income equals $100,000, then I will contribute $10,000 to my RRSP and $6,500 to my TFSA.

Total taxes plus CPP/EI deductions comes to ~$25,000, leaving me with $58,500 for personal spending.

If my projected gross income equals $120,000, then I will contribute $20,000 to my RRSP and $6,500 to my TFSA, plus an extra $5,000 lump sum payment onto the mortgage and $5,000 to top-up our vacation budget.

Total taxes plus CPP/EI deductions still comes to ~$25,000, leaving me with $58,500 for personal spending plus an extra $10,000 to allocate towards other goals.

The if/then statement allows you to maintain a good savings rate at your base income level and allows you to accelerate those goals (or add others) as your income increases.

When variable income means variable spending

One mistake I see people making when it comes to variable income is they have the tendency to base their spending rate as if they’ll always earn a full bonus or high variable salary.

I get it. When you’ve made bonus for three years in a row it’s tough to envision a year in which you don’t reach your targets and earn a bigger cheque.

But anchoring your spending to an unrealistically high income can cause major cash flow problems if your Christmas bonus ends up being a one-year membership to the Jelly of the Month Club.

The trouble arises when you lock yourself into fixed payments like a bigger mortgage, bigger car loan, private school or expensive activities for the kids, etc.

That’s why an if/then statement should also apply to your spending.

The if/then statement in this case might be:

If I receive my full bonus this year, then 20% of it will go into a high interest savings account as a “just in case I don’t get my bonus next year” fund.

Doing this allows you to smooth out lifestyle consumption so you don’t get used to living on a full bonus every single year.

By the way, this also applies to saving.

Imagine planning to contribute $30,000 per year to your RRSP because you’re sure you always make around $200,000 after bonus. So, you automate a $2,500 per month contribution to your RRSP.

Then September comes around and you’re wondering why there’s no money in your chequing account to pay off your credit card bill. A quick calculation shows you’re only on pace to earn $160,000 this year and there’s no bonus chance of a year-end bonus. Meanwhile, you’ve already put $20,000 into your RRSP, severely impacting your cash-flow for daily living expenses.

The lesson is to set an if/then statement for your savings with a lower income base in mind:

If my income is $160,000, then I’ll contribute $18,000 to my RRSP.

Now you’re only committing to $1,500 per month.

If income increases, then increase RRSP contributions via lump sum later in the year (or before the deadline).

Retirement spending floor and ceiling

Most of my retired clients want to enjoy the same standard of living they had in their final working years, if not enhance it a bit with extra money for travel and hobbies, or to help out their adult children.

But one of the best ways for retirees to reduce sequence of returns risk (receiving poor investment returns early in retirement) is to have a variable spending strategy.

What that means in practice is determining a comfortable spending floor and a safe spending ceiling.

That comfortable spending floor might be exactly how you lived in your final working years.

Consider a year like 2022, with rising and persistently high inflation and rising interest rates crushing stock and bond returns. Those years will happen from time-to-time and when they do it might feel better to skip the extravagant vacation, the home renovations, or the new vehicle upgrade.

No need to withdraw more from your portfolio than necessary in a year like that.

In a normal year (is there ever a normal year?), you might boost spending by $5,000 to $10,000 to take that trip, or remodel the bathroom, or upgrade your appliances.

And in really good times, where perhaps you’re sure you won’t ever touch your TFSA for your own consumption needs, you might give your kids an early inheritance gift of $50,000 to $100,000 to use for a down payment or to start a business, or take a dream vacation yourself.

An if/then statement for retirement spending might look like this:

If last year’s investment returns were negative, then I’ll only make minimum RRIF withdrawals in addition to any pension or government benefits, and withdrawals from non-registered savings and investments – and I won’t contribute to my TFSA.

If last year’s investment returns were between 0% to 6%, then I’ll increase withdrawals from my RRIF and/or non-registered accounts to boost spending – and I will contribute the annual maximum to my TFSA.

If I’m comfortably meeting my retirement spending needs, and I’m confident I have more than enough resources to last a lifetime, then I’ll use the proceeds from my TFSA to give an early inheritance to my kids / take the family to Hawaii / fund my grandkids’ RESPs / renovate the house / buy a new car / travel more, etc.

Final Thoughts on if/then statements

Life is surprising and doesn’t always move in a straight, predictable line. We often have variable income (up or down), lumpy spending needs, years of poor investment returns, years of strong investment returns, or periods of higher interest rates and/or inflation.

Building if/then statements into your financial plan can give you a playbook for how to treat unpredictable times in your life.

If/then statements can help you accelerate your goals and ensure appropriate balance in your life when it comes to saving and spending.

If/then statements can help save you from setting your spending (or savings) bar too high and getting into trouble with your day-to-day cash flow.

Finally, if/then statements are crucial for your retirement plan to help plan your expected withdrawals from year-to-year. Setting a comfortable spending floor and a safe spending ceiling allows you to make the most of your available resources in a responsible way throughout your retirement.