The internet was all atwitter about the stock market this week, more specifically about the performance of GameStop stock, short-selling, hedge funds, and Robinhood (a free stock trading app in the U.S.). Financial journalists, pundits, and amateur investors all offered their hot takes on this ‘Reddit-fuelled’ market frenzy. My inbox also lit up with friends and blog readers wondering just what the heck was going on.

Many of these explainers were bad or flat-out wrong – a reminder that not everyone needs to have an opinion on the news of the day. The GameStop story is a fun distraction from the mundane stay-at-home routine. The stock is up 8000% over the last six months, causing short-selling hedge funds to take a huge bath on their trade.

Meanwhile, passive investors like me watch from the sideline with great amusement.

Passive investors spent more time today making their morning toast than worrying about an individual stock

— Ramit Sethi (@ramit) January 28, 2021

Rob Carrick summed up the story nicely when he said:

“But if you’re wondering what the GameStop story means to your future investing, the answer is nothing. Enjoy the show – but don’t take notes.”

If you’re simply curious about what exactly happened with GameStop stock and how it affected Wall Street hedge funds who were betting against the company, watch Preet Banerjee’s excellent explainer on the GameStop short squeeze:

And what exactly is Robinhood’s role in the GameStop saga? Vox explains why the popular stock trading app restricted trading on GameStop, Blackberry, AMC, and other supposed ‘meme-stocks’. Robinhood now faces a class-action lawsuit saying it manipulated the market by restricting trades.

Think the GameStop short-squeeze is the greatest ever? Not even close. Of Dollars and Data blogger Nick Magguilli tells the story of Piggly Wiggly and how one man took on Wall Street all alone.

Wealthsimple Trade

Here in Canada, our only zero-commission trading platform is Wealthsimple Trade. They took a different approach than Robinhood – rather than gamifying stock and option trading (only to restrict those trades due to ‘volatility concerns’), Wealthsimple allowed its users to trade GameStop and other meme stocks freely.

They sent out an education email with a useful explainer and warning about trading volatile stocks. They also included pop-up warnings to users through the app when they searched for GameStop and other volatile stocks.

Wealthsimple Trade became the number one app on Apple’s App Store this week as the company saw a 50% increase in sign-ups. My Wealthsimple Trade review was the number one visited article on the blog this week.

This Week’s Recap:

No new posts from me here this week as I caught up on financial planning work and freelance writing projects.

I’ve also changed email delivery providers, so if you subscribe and receive new posts by email please double-check that this article was delivered to your inbox on Saturday. If you want to join 10,000+ email subscribers and get notified whenever I get around to publishing a new article, you can enter your email in the subscription box located at the top-right of the website.

Over on Young & Thrifty I shared the best blue-chip stocks to buy in 2021.

From the archives: So you’ve made an RRSP contribution. Now what?

Promo of the Week:

I’ll beat this drum again – stop parking your cash in your big bank chequing or savings account. You can find decent high interest savings at online banks and credit unions.

Here’s the biggest no-brainer move to make with your emergency fund money right now. The big banks pay nothing on your savings deposits. EQ Bank’s Savings Plus Account consistently offers an everyday high interest rate at or near the top of the market (currently 1.5%) with no hassles. Open an account here and fund it with $100 within 30 days and you’ll get a $20 cash bonus for free.

Weekend Reading:

Believe it or not there were other, non-GameStop related articles published this week. Here’s what I was reading:

Erica Alini explains how the pandemic housing craze is fuelling another boom – reverse mortgages:

“Many borrowers take out a reverse mortgage loan to pay off other debts, a strategy that allows them to eliminate debt repayments and free up some cash flow. Seniors have also traditionally used these loans to provide a regular, tax-free income supplement.

But in recent months, Ziomecki says she’s noticed an increase in the number of applicants who want to borrow against their home to help their children or grandchildren get into the real estate market.”

Jason Heath says TFSAs may be a no-brainer but don’t fall into the trap of neglecting your RRSP.

Here’s Millionaire Teacher Andrew Hallam on why you might not want a higher paying job. Couldn’t agree more.

Academic research on thematic ETFs shows their average returns underperform the market by about 4% per year.

Here’s Squawkfox Kerry Taylor on opportunity costs and trade-offs:

My Own Advisor Mark Seed and Findependence Hub’s Jon Chevreau discuss whether you should speculate with your retirement portfolio.

Can a rule of thumb be a short-cut to financial well-being? Morningstar research explores how financial rules of thumb can help or hold back investors.

Rewards Canada’s Patrick Sojka explains why earning 5x points with one credit card isn’t the same as earning 5x points with another credit card. It’s all about the earn and the burn.

Michael James on Money shares a good review of Ramit Sethi’s book, I Will Teach You To Be Rich. I used to find Ramit’s approach to be off-putting but I’ve mostly come around.

Life expectancy is one of the greatest unknowns in retirement planning. Jason Heath offers strategies for both a long and short retirement.

Finally, here’s a cool story from a local Lethbridge entrepreneur who is building a luxury playhouse cottage resort in Alberta’s Crowsnest Pass.

Have a great weekend, everyone!

The deadline to contribute to your RRSP for the 2020 tax year is just over a month away (March 1, 2021). Now is a great time to take advantage of any unused RRSP contribution room and reduce your net income (and tax burden) for 2020.

Remember, your RRSP deduction limit is determined by:

- Your unused RRSP deduction room at the end of the preceding year, plus;

- The lessor of 18% of your earned income in the previous year, or the annual RRSP limit ($27,230 in 2020)

When in doubt, check your CRA My Account.

I’ve already maxed out my RRSP deduction limit for 2020, but in previous years when I was catching up on unused room I’d use the first 60 days of the year to take stock of my tax situation and then make an RRSP contribution to bring any taxes owning down to zero (or close to).

Here are some other lesser known RRSP tax tips to consider:

1.) An RRSP Loan

It’s a good rule of thumb to make regular RRSP contributions throughout the year. But an RRSP loan can be useful to boost your retirement savings, catch up on available contribution room, and reduce your tax burden (particularly if you take the ‘first 60 days’ approach to maximizing your tax planning).

The basic idea is to take out an RRSP loan from your bank at interest rates that closely resemble home equity line of credit rates (2.95% – 3.95% these days), make your RRSP contribution, and then pay back the loan over a short-period of time (3-6 months) with your tax refund and other cash flow.

2.) Reduce Tax Deductions at Source

Making an RRSP contribution is simply one of the best strategies for high income earners to build retirement savings and reduce their tax burden. Managing your cash flow can be an issue, though. That’s because you don’t realize the tax savings until you file your taxes the following year.

That’s where the form T1213 Request to Reduce Tax Deductions at Source comes into play. Fill out the form and indicate how much you plan to contribute to your RRSP this year. Submit it to the CRA along with proof – such as a print out showing confirmation of your automatic monthly deposits. The CRA will assess the form and send you back a letter to submit to your human resources / payroll department explaining how they should calculate the amount of tax they withhold for the year.

Note that you’ll need to fill out and submit the form every year.

Reducing taxes withheld from your paycheque frees up more cash flow to make your RRSP contributions. It’s like getting your tax refund ahead of time instead of waiting until after you file.

3.) Pension Income Tax Credit

The pension income amount allows you to claim a non-refundable tax credit on up to $2,000 of eligible pension income. If you are over the age of 65 you can create your own qualified pension income to take advantage of the pension income tax credit.

What you can do is transfer a small amount – say, $12,000 – from your RRSP into a RRIF at age 65. This allows you to withdraw $2,000 from your RRIF each year for six years and claim the pension income amount.

This Week’s Recap:

In my latest instalment of the Money Bag I answered reader questions about investing in cryptocurrency, selling stocks at a loss, and comparing your finances to others.

Speaking of investing in cryptocurrency, I shared my thoughts in this Global News piece by Erica Alini about whether Bitcoin belongs in your investment portfolio.

Over on the Young & Thrifty blog I explained how to invest in IPO stocks.

From the archives: So you’ve made your RRSP contribution. Now what?

Promo of the Week:

The message in that post from the archives is about the second step after contributing to your RRSP or TFSA account. Yes, I’m talking about actually investing the contribution.

More and more readers (and my fee-only planning clients) are choosing to self-direct their investments at Questrade. It’s not rocket-science by any means, especially if you use a single-ticket asset allocation ETF, but you still need to know how to execute a trade on the platform. Here’s how to do it using the Vanguard Balanced ETF (VBAL):

- Log in to your Questrade account

- Click on the green ‘Trade’ button at the top right of the screen

- Under the ‘Order Entry’ window on the right hand side, enter the ETF symbol (VBAL)

That screen will look like this:

- Look at the ‘ask’ price. You’re going to place a ‘Limit Order’ at one penny above the ‘ask’ price.

- Now confirm the amount of money you have in cash that you want to use to make this purchase (i.e. $10,000)

- Divide the amount of cash by the ‘Limit Order’ price. So, in the example above, it’s $10,000 divided by $28.90 = 346.02 shares.

- Round that number down to the nearest even number, so 346 shares.

- Enter that number where it says ‘Quantity’.

- Confirm which account type you’re making the trade in (RRSP, TFSA).

- Click the green ‘Buy’ button.

- Confirm the trade.

That’s all there is to it! Open a Questrade account and you’ll get $50 in trading commission rebates (ETF purchases are free, but selling costs $4.95 per trade).

Weekend Reading:

Our friends at Credit Card Genius look at which credit card has the best return on spending in Canada.

ETF sales outpaced mutual fund sales in Canada last year ($41.5B to $31B), but in terms of total assets under management ETFs still lag far behind mutual funds.

Jim Yih at the Retire Happy blog has all the financial planning numbers you need to know for 2021.

My Own Advisor blogger Mark Seed looks at the pros and cons of taking a salary or dividends from your corporation. This is a challenge I’m still wrestling with today.

Here’s an interesting discussion on Reddit from an insider about the problems with the financial advice industry. I don’t necessarily agree with the amount of time it takes to on-board new clients, but the rest of the comment and discussion is certainly worth a read.

Michael James on Money reports his investment returns for 2020. I like that he includes the 20% of his portfolio now held in savings accounts, GICs, and short-term bonds, which obviously brings down the overall return but reflects the reality of a retiree living off his savings.

A really smart post by Millionaire Teacher Andrew Hallam on stock market solutions to irrational exuberance:

“When it comes to investing, anything can happen. Stocks will often be priced far higher than they should. But nobody can see the future. That’s why investors shouldn’t speculate. They should maintain a diversified low-cost portfolio of U.S. stocks, developed international stocks, emerging market stocks and bonds.”

Canadian Couch Potato blogger Dan Bortolotti reports the 2020 investment returns of his couch potato model portfolios.

Justin Bender, Dan’s PWL Capital partner in crime, shares the 2020 asset allocation ETF returns from Vanguard and iShares:

Rob Carrick says the epic failure of online brokers’ mishandling of call volume in 2020 could drive away their most valued clients – well-off retirees.

A Wealth of Common Sense blogger Ben Carlson looks at markets that are definitely not in a bubble, namely value stocks, emerging markets, European stocks, and Japanese stocks.

Here’s an interview with Ben Carlson on the Humble Dollar blog about his new book, Everything You Need to Know About Saving for Retirement.

Finally, why Canada should allow joint tax filing for spouses rather than taxing individuals.

Have a great weekend, everyone!

Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

This edition of the Money Bag answers your questions about cryptocurrency FOMO, selling stocks at a loss, selling stocks at a gain, and comparing your finances to others.

First up is Terri, who wants to know if she should invest a small amount of money in cryptocurrency, given its recent ‘hype’. Take it away, Terri:

Cryptocurrency FOMO

Hi Robb,

I wanted to get your opinion on this crazy cryptocurrency move – I’m sure you’re getting a lot of questions about it. I’m not sold on it as an alternative to fiat currencies or a way to hedge against inflation. To be honest I’m not 100% sure how it works and I don’t think anyone really understands how it derives value. However, it does seem like an opportunity to invest in an asset class in its infancy. Have you done much research into this? I will admit to having some “FOMO” with the recent move, I think I’d like to look into investing a very small portion.

Hi Terri,

I’ll be honest, I heard more about Bitcoin during its last run-up at the end of 2017. That culminated when our 19-year-old restaurant server talked about wanting to buy it with her student loan money. The price proceeded to plummet from nearly $20,000 per coin to about $8,000 in two months and continued down to as low as $3,200 per coin a year later.

So why should this time be any different?

Here’s a bit of background on Bitcoin and Ethereum (the distant number two cryptocurrency):

Bitcoin really only has two uses: a digital currency and a store of value. The primary goal is to establish itself as an alternative monetary system. Like gold, there’s no intrinsic value but its price goes up or down based on public sentiment and speculation. Investors will bid the price up if they believe the demand for Bitcoin will increase, or sell and drive the price down if they believe demand will fall.

Ethereum, on the other hand, is an entire blockchain network that can be used to run decentralized applications, create and enforce smart contracts, and even create additional cryptocurrencies. Ether – the cryptocurrency of Ethereum – can be sent, received, and stored as digital money. It’s used to pay transaction fees on the Ethereum network.

You can buy Bitcoin and/or Ethereum on Wealthsimple Trade (WS Crypto), but the platform is quite a bit different than a traditional crypto trading platform like Coinbase where you actually hold crypto coins in digital wallets. WS Crypto simply allows you to trade the two cryptocurrencies – you don’t get to take hold of any coins in your own digital wallet. These traditional exchanges are prone to major hacks and security breaches. And, if you lose your “key” your coins are lost forever. Not ideal!

All of this said, I don’t recommend speculating on cryptocurrency any more than I’d recommend speculating on gold or other precious metals. Bitcoin is highly volatile, and if you do decide to buy make sure your stake doesn’t make up any more than 2-3% of your portfolio. You can’t hold it in an RRSP or TFSA, so it must be purchased in a taxable account and you track any capital gains or losses associated with buying and selling.

I don’t believe there is an ETF that holds a bunch of different cryptocurrencies. There is The Bitcoin Fund (QBTC) from 3iQ Corp – it comes with a management fee of 1.95%

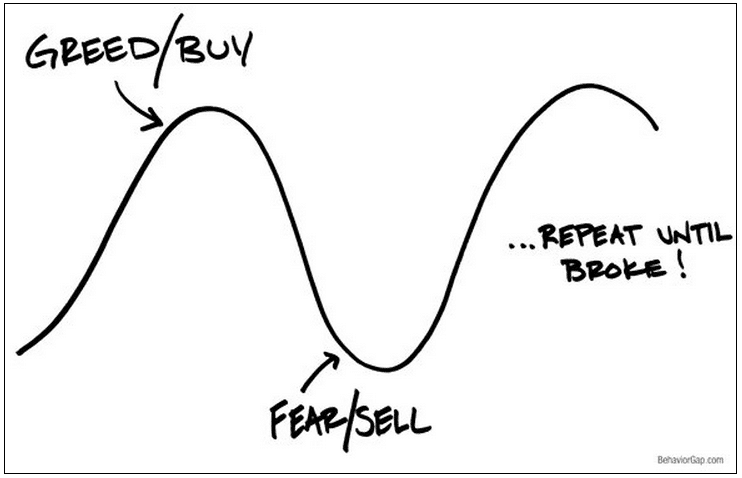

Finally, I’ll leave you with one of my favourite investing charts from Carl Richards, called the Fear and Greed cycle:

All the best!

Selling Stocks at a Loss

Here’s Norm, whose portfolio of individual stocks has taken a beating. He’s wondering when to pull the trigger on switching to a globally diversified index ETF. Sounds familiar:

Hey Robb,

I am planning to switch over my investments to a one-ticket ETF solution (VEQT) in a non-registered account, but I’m wondering about timing. Sadly, my portfolio is down significantly – the original investment of $175,000 is now down to $143,000. It’s largely made up of Canadian dividend payers that includes banks, materials, telecoms and oil stocks. It’s the oil companies that have ravaged the account – with some names down 80%.

I know it’s never a good thing to try to time the market, but I do feel like the banks, materials, and especially the energy sector finally have some tailwinds as the economy starts to reopen and could potentially recoup some of their losses. I wondered about waiting until this time next year, seeing how the portfolio does, and then making the official switch.

Hi Norm, thanks for your email. My advice would be to cut your losses and make the switch as soon as possible. You’ll benefit from the capital loss, which can be carried forward indefinitely to use against a capital gain in future years.

Related: Tax Loss Harvesting Explained

It’s a classic psychological mistake to wait for your losing stocks to come back to even. The stocks don’t care what price you paid for them. Their future prospects may continue to be bleak. Meanwhile, VEQT represents a significantly more diversified and therefore more reliable outcome over the long term.

You’ll still have exposure to all of those sectors, especially given VEQT’s 29% weighting to Canadian stocks.

It hurts to sell something at a big loss. I know, I’ve been there when I used to be a stock picker. It might be helpful to think of your non-registered portfolio as one large lump sum of cash right now. If it were in cash, would you re-purchase the exact same positions that you have now – or would you just buy VEQT? There’s your answer.

Selling Stocks at a Gain (to Rebalance)

Next up is Tracy, who took a chance on some growth stocks last year and now wonders if it’s time to take some profits and rebalance:

Hi Robb,

Last March I took advantage of the COVID dip by purchasing VEQT and some “play” stocks in electric vehicle companies. As a result of the growth in recent months, those “play” stocks now represent a double-digit percentage of my portfolio.

How does one go about rebalancing their portfolio in this scenario? Take out the original amount invested in the stocks (to buy VEQT) and leave the rest in? Leave it all in? Get out of the stocks altogether?

I don’t have much experience with stock investing, and I know you started in stocks, so thought I’d ask.

Hi Tracy, this would first depend on which account type you’re talking about. If in an RRSP or TFSA, I’d say trim your stock holdings by selling off shares to get you back to a comfortable level of “explore” compared to your core.

Yes, the idea would be to rebalance by using those proceeds to buy more VEQT. Set some rules around your stock picking, like no more than 5-10% of your total portfolio value, and then you’ll always have some guidance when to take some profits off the table.

Things are more complicated in a taxable (non-registered) account, as selling any holdings will trigger capital gains for this tax year (2021). You could get closer to your target asset mix by contributing any new money to VEQT only.

Letting your winning stocks ride can be risky as the range of outcomes is much more volatile with one single stock than it is with a globally diversified basket containing thousands of stocks.

Comparing Your Finances to Others

Finally, here’s a question from Peter who seems worried about how his finances are doing compared to his peers:

Hi Robb, I’m a relatively new passive investor, starting Jan 2019, but have been inspired by your timeline and I’m aiming for a goal you had early on: $100k by age 35.

I’m almost 34. My net worth is currently small at $76k. Therefore, my “plan”: save, save, save and at $100k seek out some fee-only advice (most likely yours) to hopefully find what I’m missing and if there are any inefficiencies in my portfolio.

What I didn’t realize until today though, upon reading your “2020 Year-End Review” post, was that at 35 you hit $100k in investments, PLUS you already had a home (purchased three years earlier). As a result, your net worth was MUCH higher than $100k at 35. Suddenly your timeline seems far less achievable…

My questions (finally):

-

- Should this dissuade me / am I on the right track?

- Does a home-purchase “before it’s too late” and then restarting my investment growth after that make any sense, especially considering I don’t really want or need a house currently?

- Does my “plan” make sense considering my late start to saving/investing?

Hi Peter, thanks for your email. I don’t think it’s useful to compare your situation to others. Everyone gets out of the starting gate at different times and with different circumstances that are largely out of their control.

Focus on your short- and long-term goals and strive to keep the needle moving forward each year. You can’t do everything all at once, so prioritize what’s important to you and make adjustments to those priorities as you move forward.

There’s nothing wrong with renting while you grow your investments. Renting offers flexibility and affordability, which can’t be understated.

If your employer offers a matching program, be sure to take full advantage of it. Make sure you’re investing the money in your TFSA rather than just keeping it in cash (if it is intended for long-term growth). Focus on increasing your savings rate each year. The milestones will come.

My finances were a mess in my 20s. I used my late 20s / early 30s to get them cleaned up and start saving. But I largely benefited from a sudden surge in real estate prices on my first home (from $129k to $239k in just a few years), which gave us some breathing room.

I changed careers to a slightly higher paying job that required less travel and was more of a 9-5. That freedom allowed me to start blogging, freelance writing, and eventually doing financial plans. The income earned from these side hustles significantly accelerated our savings goals.

My point is, don’t get bogged down looking at age-based savings goals. Focus on what you can control and keep improving each year. You’ll get there.

Best of luck!

Do you have a money-related question for me? Hit me up in the comments below or send me an email.