The Canadian media loves to talk about real estate – particularly Toronto real estate – and its seemingly unstoppable climb to new heights. The average home price in Canada reached $538,831 (June, 2020). That’s up 6.5% versus the same time last year. In a pandemic.

The national average doesn’t tell the whole story, though, as home prices in Toronto shot up an incredible 16.9% last month (year-over-year) to reach an all-time high of $943,710. Vancouver gets considerably less national attention than Toronto but its home prices rose by 4.5% to reach an average of $1,031,400.

I don’t write enough about Canadian real estate. I live in Lethbridge, AB, a small city of 100,000 people where the average home price is in the $350,000 range. For that reason I don’t view real estate with the same lens as those living in Toronto or Vancouver.

Rising real estate prices is a big deal for many Canadians. Young people can’t afford to get in the market and have been told for 12+ years to wait for the real estate bubble to burst. It hasn’t happened.

Looking at that chart, it’s certainly understandable for young Canadians to feel some real estate FOMO (fear of missing out). Getting into a house in Toronto or Vancouver at any time over the past 10+ years now looks like it would have been a great decision. If that trend continues, then why wouldn’t young people do everything they can to scrape together a 5% down payment (10% on the portion above $500,000) just to get a piece of the action?

We try to make the best decisions we can with the information we have at the time. It’s painful to look back and see that a decision to buy a house (or invest in a stock) would have led to a great outcome. But you have to remember why you didn’t pull the trigger in the first place. If that decision was based on sound reasoning then you can’t beat yourself up over an outcome that’s largely out of your control.

Real estate is such a polarizing topic and our views are often guided by our own experience. Boomers who’ve benefited from enormous price gains in the past 30 years might believe housing is a surefire investment and that prices will always go up (“Everyone needs a place to live. They’re not making any more land.”).

Young people living in major cities might believe homeownership is largely out of reach for them. The FOMO effect is real.

Meanwhile, those of us living in non-major centres might have mixed feelings towards real estate. The housing boom in Toronto and Vancouver is so disjointed from our own experiences with real estate that it may be difficult to empathize with people living in those cities.

My thinking on real estate is that homeownership is a highly personal decision. It should start with the idea that a home is not an investment, but a place to live. It should be a long-term decision, ideally staying in the same place for 10+ years. Its location should align with your lifestyle as much as possible and avoid stressors like unnecessarily long commutes and excessive maintenance. Finally, homeownership should not impact your ability to save for retirement or afford childcare.

If you can tick all of these boxes then it should not matter whether you buy a house in Toronto, Vancouver, or Lethbridge.

Unfortunately, soaring real estate prices in Toronto and Vancouver mean an increasing number of younger Canadians will have to come to grips with renting – something that people in New York and San Francisco have known for many years. The homeownership rate in San Francisco is just 37.6% and in New York it’s just 33%.

Vancouver’s home ownership rate is 64%, and Toronto’s is 67% – just 1% off the national average. Something has to give.

This Week’s Recap:

On Wednesday I wrote about past performance and your expected future investment returns.

From the archives: Here are 15 money saving tips to live by

Over on Rewards Cards Canada – understanding the difference between Air Miles Cash and Dream Miles.

Promo of the Week:

Wealthsimple Trade is Canada’s first and only zero-commission trading platform where investors can trade stocks and ETFs for free in an RRSP, TFSA, or non-registered account. Sign up for Wealthsimple Trade today.

For most robust investing needs, including for LIRAs, Margin, and Corporate accounts, Questrade is still the king of low-cost investing in Canada. You can purchase ETFs for free and trade stocks for as little as $4.95. Take your savings further with a registered account at Questrade.

Weekend Reading:

Credit Card Genius explains what is a good credit score in Canada and is it good enough to be approved?

Barry Choi at Money We Have looks at grocery stores that price match in Canada.

Visual Capitalist ranks the best and worst pension plans in the world.

Of Dollars and Data blogger Nick Maggiulli explains why a metric called the Wealth Discipline Ratio is the most important number in personal finance:

“This is a measure of your financial discipline through both savings and investing. It’s not just your savings rate, because it also incorporates how you use your savings to invest and increase your wealth.”

A report from the Canadian Institute of Actuaries looks at claiming CPP at age 70 vs age 65 and concludes that most people should wait to claim CPP benefits. While there are good reasons to take CPP early, I generally agree that deferring CPP to age 70 is a smart move.

There are fewer publicly listed companies today than there were in 1976. Michael Batnick explains where all the stocks went.

Here’s an interesting look at how Covid-19 has impacted people’s investment outlook from around the globe.

At home, 8 million Canadians are rethinking retirement because of Covid-19.

MoneySense’s Jason Heath offers six strategies to help your kids financially.

Gen Y Money takes a look at the best travel credit cards for seniors. These typically will have better travel insurance benefits for those over the age of 65.

Gold has surpassed $2,000 and the Irrelevant Investor Michael Batnick explains what’s driving the price.

Episode nine of the Canadian Portfolio Manager podcast looks at currency-hedged ETFs and whether they make sense for Canadian investors.

Finally, Millionaire Teacher Andrew Hallam explains why you should ignore how the “smart money” invests right now.

Have a great weekend, everyone!

“Past performance is not an indicator of future results.” Investors have heard this disclaimer for years, yet when it comes to picking investments we can’t help but look to a fund’s historical results to determine its quality.

Indeed, it’s one of the first questions asked whenever I mention the idea of switching to an indexed investing approach, or using a robo-advisor. How do their returns compare?

Online investing platforms are relatively new to the scene and so unlike many established mutual funds they don’t have a lengthy track record for investors to compare and measure results.

Past Performance as a Measure

But I argue that using past performance as a measure for future investment returns is misguided for two reasons.

- Cost is a better predictor of success. Morningstar grouped mutual funds together from different sector classes and sorted them by fees. The cheapest funds were three times as likely to succeed as the priciest funds (success was measured as outperforming its category group).

- Past performance needs context. Knowing that a mutual fund returned 7% annually over the past five years means little until you compare that with an appropriate benchmark over the same time period. If you find that a comparable index fund returned 9%, then the mutual fund underperformed.

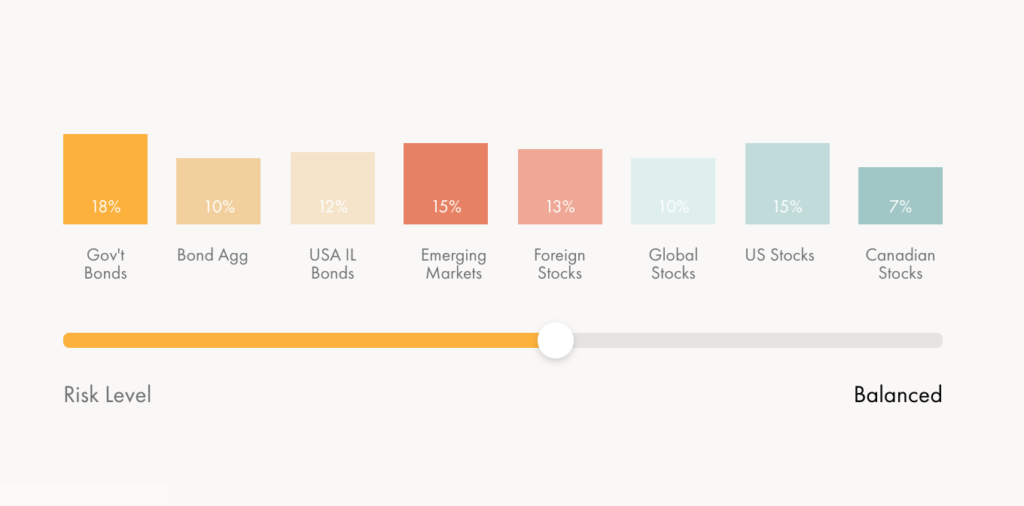

RBC Balanced Fund vs. Robo-Advisor Balanced Portfolio

Let’s examine RBC’s popular Balanced Fund (RBF272), which has been around for more than thirty years and has nearly $5 billion in assets under management.

The fund has delivered annual returns of 6.2 percent since inception. It is comprised of about 36% Canadian bonds, 33% Canadian stocks, 10% U.S. stocks, 8% International stocks, plus some underlying mutual funds and cash. The management expense ratio (MER) of the fund is 2.16%. <—–That’s high!

The RBC Balanced Fund has a decent track record for a fund in its category, but we want to know how it will perform in the future.

What we know for certain is that the returns delivered by this fund will be reduced by 2.16% every year. A similar fund (or portfolio of funds) that charged just 0.66% annually should theoretically outperform RBC’s Balanced Fund by 1.50% a year.

Related: Yes, You Can Retire Up To 30% Wealthier

Now compare that with a balanced portfolio offered through a robo-advisor platform. An investor could get a similar mix of Canadian bonds, Canadian equities, and U.S. and International stocks (60% stocks, 40% bonds), although less tilted towards Canada.

Since robo-advisor platforms are fairly new, investors won’t find any lengthy past performance numbers to compare with something that has the track record of RBC’s Balanced Fund. However, my argument is that past performance numbers mean very little when it comes to the quality of a portfolio and its future expected return.

Investments managed by a robo-advisor give you an edge on fees because they typically use low-cost index funds and ETFs to make up a diversified portfolio.

Related: The Top ETFs and Model Portfolios for Canadians

Even without much of a track record at all, past performance of a robo-advised portfolio can be safely ignored because the investments inside are set up to track particular indexes and deliver those market returns, minus a small fee.

How should you think about choosing your investments?

First, while costs aren’t the be-all and end-all of investment selection, they do matter. A lot. Aim to keep your investment fees as low as possible.

Second, diversify. Nobel-prize winning economist Harry Markowitz called diversification, “the only free lunch in finance.” The idea is that by diversifying, an investor gets a benefit (reduced risk) at no loss in returns.

Third, be risk-aware. If you can’t stomach the idea of stocks losing 30% or 40% in a short period of time, then don’t put 80% or more of your portfolio in stocks. A balanced portfolio of 50% to 60% stocks and 40% to 50% bonds will lower that volatility and smooth out your investment returns over time.

Fourth, know your competencies. If you have the skill, drive, and temperament to manage your own investment portfolio then by all means open up a discount brokerage account and go the do-it-yourself route. However, if you lack one or more of those traits, it makes sense to pay someone else to manage it for you.

Investing made easy

The advent of robo-advisor digital investing platforms has made that last point easier and a lot more palatable for investors.

Why?

By using a robo-advisor investors are likely to save at least 1% to 1.5% each year on their investment fees (compared to a bank managed portfolio). Expect to pay around 0.50% for a robo-managed portfolio, plus a bit less than 0.20% for the management expense ratios (MERs) charged by the ETFs held inside your portfolio.

Robo-advisors construct their portfolios with global diversification in mind, giving you access to Canadian stocks and bonds, plus thousands of U.S., International, and Emerging Market stocks.

Robo-advisors have pre-packaged portfolios tailored to your risk profile, so if you’re an ultra-conservative, risk averse investor you can get a portfolio heavy on fixed income with a dash of equity exposure. Alternatively, an investor looking for maximum growth can get a portfolio tilted more heavily toward equities.

Related: Using a Robo Advisor in Retirement – A Wealthsimple Case Study

Finally, for those who lack the know-how or want-to, a robo-advisor offers an easy solution for investors to achieve all three of those objectives while saving for the future.

Final thoughts

If you’re investing in mutual funds on your own or through a traditional advisor, consider the amount of fees that you pay annually and whether you’re getting value for that advice. You might find you’re overpaying for advice, or that your managed investments are lagging behind the market (or both).

If that’s the case, a robo-advisor solution would be a great alternative for your investments. You’ll get lower fees, broad diversification, and customized portfolios designed to capture market returns at an appropriate level of risk.

That last point is key: you’re capturing market returns, not chasing past performance or trying to beat the market.

“History doesn’t repeat itself, but it often rhymes.”

The U.S. stock market continues to defy all logic as the S&P 500 is now up 1.12% on the year. If you slept through the first seven months of 2020 (congratulations?) you would’ve missed stocks surging 5.14% by February 20 to reach an all-time high, then plummeting to -30.83% on the year by March 23, before steadily climbing back to positive territory by the end of July. Ho-hum.

This resurgence has been predominantly fuelled by tech stocks, as companies like Tesla (up 223%), Amazon (up 69%), and Apple (up 43%), among other big names, seem to be propping up the stock market.

Our own Canadian tech darling is Shopify, whose stock run-up of 161% this year has made it the most valuable company in Canada.

It’s fair for investors to ask if we’re in another tech bubble. I mean, the last time we’ve seen such disparity between tech stocks and non-tech stocks was in the tech bubble of the late 90s. Take a look at this chart comparing PowerShares QQQ (tracking the Nasdaq 100 index) and SPDR SPY (tracking the S&P 500):

You can see the tech bubble peaking in March 2000 and then crashing hard. The Nasdaq continued to trail the S&P 500 for the next 10 years before taking off again in 2012. The results over the next eight years have been staggering:

| ETF | YTD | 1-year | 5-year | Since 1999 |

| PowerShares QQQ | 24.1% | 41.9% | 140.5% | 397.6% |

| SPRD S&P 500 (SPY) | 1.3% | 11.6% | 55.9% | 144.1% |

Indeed, the tech-driven Nasdaq has crushed the S&P 500 – not just for the past decade but even dating back to 1999.

Tech stock proponents argue that this time is different because the companies driving the market today are actually (mostly) profitable compared to the Pets.com stocks that defined the 90s tech bubble.

To that I’d ask whether a company like Tesla, which is worth $266 billion on annual car sales of less than 300,000, is really worth $100 billion more than Toyota, the next largest car manufacturer with 11 million automobiles sold in 2019?

Fear of missing out is a real emotion when it comes to investing. I mean, who doesn’t look at the individual stock gains of Tesla or Shopify and want in on the action? I’ve even had readers ask if they should bother investing in anything but the Nasdaq since it seems to be the runaway winner for the past two decades.

It’s easy to look back and identify winning investments. It’s much more difficult to predict future winners. There’s no reason to expect that the Nasdaq will continue its massive outperformance. In fact, history suggests it’s much more likely to revert back to the mean at some point – which would make an investment in the Nasdaq now seem foolish.

That’s why diversification works. It doesn’t make for great dinner party conversation (remember dinner parties?), but a boring, low-cost, globally diversified portfolio will ensure you capture a small slice of all the winning investments while spreading your risk around so that no single stock, sector, or even country can destroy your investment returns.

I don’t know whether we’re in another tech bubble or if this is truly a new normal. All I know is that companies fall in and out of favour all the time. The vast majority of investors can’t identify the winners in advance, which is why we’re better off just owning a small slice of every company and rebalancing often.

This Week’s Recap:

Lots of buzz generated from this article on if renting is a waste of money. Bottom line: renting offers tremendous flexibility for those who might want to relocate, travel extensively, or who simply don’t want to deal with the hassles and headaches of homeownership.

Over on Young & Thrifty I explained how to transfer USD into your Questrade account.

I also took a fun look at whether you should invest in airline stocks and ETFs. Spoiler: Don’t.

Jonathan Chevreau included my thoughts on the 4% rule in his latest piece for MoneySense.

Promo of the Week:

Big banks, credit unions, and online banks continue their assault on high interest savings account rates. Most recently, Motive Financial dropped its interest rate to 1.75%.

As I’ve said many times, EQ Bank’s Savings Plus Account consistently offers an everyday high interest rate at or near the top of the market (currently 2%) with no hassles. Open an account here and fund it with $100 within 30 days and you’ll get a $20 cash bonus for free. This is a no-brainer when it comes to parking your emergency savings.

Speaking of no-brainers, this week I applied for the TD Aeroplan Visa Infinite Card. The current card promotion gets you 15,000 Aeroplan miles upon first purchase (nice!) and waives the annual fee in the first year. Time to build up my Aeroplan miles account again.

Weekend Reading:

Anyone else received an ‘amazing business opportunity’ from a friend or acquaintance recently? MLMs are back in a big way, with many people looking for ways to increase their income during the pandemic and shelter in place orders.

Now MLMs have a new target audience: The #GirlBoss

They promote the message that women are failing because they aren’t working hard enough, rather than acknowledge the simple fact that “99% of sellers end up losing money when they invest in multi-level marketing.”

A few weeks ago I mentioned my rewards credit card (Capital One Aspire Travel World Elite Mastercard) was finally getting downgraded from 2% to 1.5% and removing the 10,000 annual bonus miles. The Globe and Mail’s Rob Carrick has the same card and asked his readers for recommendations – and some surprise cards emerged.

Tawcan blogger Bob Lai also has the Capital One card and decided to replace it with the HSBC World Elite Mastercard.

A great message here from Hannah (At The End Of The Day), who says, “as COVID-19 forces us to reconsider everything about daily life, something we need to talk about more is our cycle of mindless consumption.”

This post from Nick Maggiulli ties in nicely with my opening remarks on diversification: Why you don’t need alpha.

Ben Carlson from A Wealth of Common Sense says patience is a virtue no one haas time for anymore.

PWL Capital’s Ben Felix is back with another Common Sense Investing video. This one aims to explain the Fed’s “Money Printer” (QE, the Stock Market, and Inflation):

Mortgage expert Rob McLister says variable rates are a gamble that you don’t need to take right now. This makes sense when you consider there’s no upside for rates to fall further, while at the same time large variable rate discounts have dried up.

Here’s an interesting look at how the pandemic could cost you some of your CPP retirement benefits.

Deferring CPP to age 70 is starting to gain more traction. Here’s a way for Canadians with RRSP savings to get the most out of their CPP benefits.

The head of CMHC says Covid-19 is widening the wealth gap between homeowners and renters:

“The problem is that we’re in a game of musical chairs and when the music stops playing, it’ll be young first-time homebuyers who are holding the bag.”

My Own Advisor Mark Seed explains why you should leave DSC (deferred sales charge) mutual funds for good.

Finally, Millionaire Teacher Andrew Hallam looks at why so many wealthy people drive understated cars.

Have a great weekend, everyone!