Putting Together Your Retirement Income Puzzle Pieces

One reason why retirement planning is so challenging to think about is because we often go from receiving one income stream (our T4 salary income) to juggling several different income streams throughout retirement.

Even more confusing is the fact that those retirement income streams often can (or should) arrive at different times and may have different tax treatments.

Why do you need a retirement plan?

Consider that you might draw an income from the following sources in retirement:

- Defined benefit pension

- RRSP or RRIF

- LIF

- TFSA

- Non-registered investments

- Non-registered savings

- Corporation

- CPP

- OAS

Let's explore a potentially dizzying array of decisions.

Members of a defined benefit pension plan will have to make a tricky decision about when to retire (early and reduced, earliest unreduced, or normal retirement date). Then they'll need to select from a menu of joint and survivor options (100%, 67%, 60%, 50%) with or without a 5, 10, or 15 year guarantee if you die early.

Those with a spouse are required to choose a joint life pension option that leaves their spouse a percentage of the monthly pension payments if they die first, however your spouse can sign a waiver giving up their rights to this benefit.

You can withdraw from an RRSP at any age before it must collapse at the end of the year you turn 71.

A RRIF conversion must be done at that time, but it can happen earlier and might make the most sense at 65 when RRIF income becomes eligible pension income and can be split with a spouse or common law partner.

A LIRA to LIF conversion has to wait until at least age 55 in most cases, and similarly must be done by the end of the year you turn 71. This conversion can also come with another decision around unlocking 50% to 100% of the LIF (depending on the jurisdiction) to move into a more flexible RRSP or RRIF.

TFSA withdrawals can be done at any time and for any reason, and withdrawals are completely tax free. The added bonus is that you get the contribution room back the following year after a withdrawal is made. But it might be wise to leave your TFSA funds intact to act as a margin of safety or tax-free pot of money for your beneficiaries.

Small business owners have the added complexity of winding-down their corporation by withdrawing funds personally via dividends.

Those with non-registered investments need to consider capital gains from the sale of stocks or funds that have appreciated in value over the years. Capital gains are taxed favourably, since only 50% (half) of the gain is considered taxable and added to your income (but only when sold). Investment income earned from dividends and interest are taxable in the year received.

Non-registered savings from a regular savings account is money that you have already paid tax on earlier, although as explained above the interest income earned is fully taxable in the year received.

Then there are your government benefits (CPP and OAS) to consider.

You can take your CPP as early as age 60, but it's often a mistake to do so because of the permanent 36% early take-up penalty. Taking CPP at 65 would be considered your normal retirement age with no penalty. And those who can wait to take their CPP at 70 will see their benefits rise by 42% (plus inflation adjustments).

OAS, meanwhile, cannot be claimed earlier than 65 but will automatically start at that age unless you tell Service Canada otherwise. As long as you've lived in Canada for 40 years between 18 and 65 you'll get 100% of your entitled OAS benefits (before clawback considerations). Subtract 2.5% for every year that you were not in Canada during that time. Delaying OAS to age 70 will lead to 36% more in benefits (plus inflation adjustments).

Putting the Puzzle Pieces Together

In my advice-only financial planning practice I explain to clients that I'm trying to help them fit their retirement income puzzle pieces together in the most tax efficient way to meet their retirement spending needs.

I liken it to trying to get your car out of the parking garage in one of those 3D puzzle games.

Some puzzle pieces need to be moved aside to make room for other income streams to come online.

For instance, it's now widely accepted that most Canadians are going to get more lifetime income if they delay taking CPP until 70. But I don't want you to delay living your best early retirement lifestyle until 70 when your benefits kick-in. We're just going to get the income from somewhere else, like your RRSP or RRIF with perhaps a top-up from non-registered funds.

The result from shifting these puzzle pieces around is that you maximize your lifetime spending and minimize your lifetime taxes.

Indeed, we can fool ourselves into keeping our tax rate extremely low in our 60s by drawing from our non-registered savings and TFSA, only to discover we've kicked a major tax problem down the road when the inevitable collision of taxable income from our RRIF, CPP, and OAS begins in our 70s.

Our Retirement Income Plan

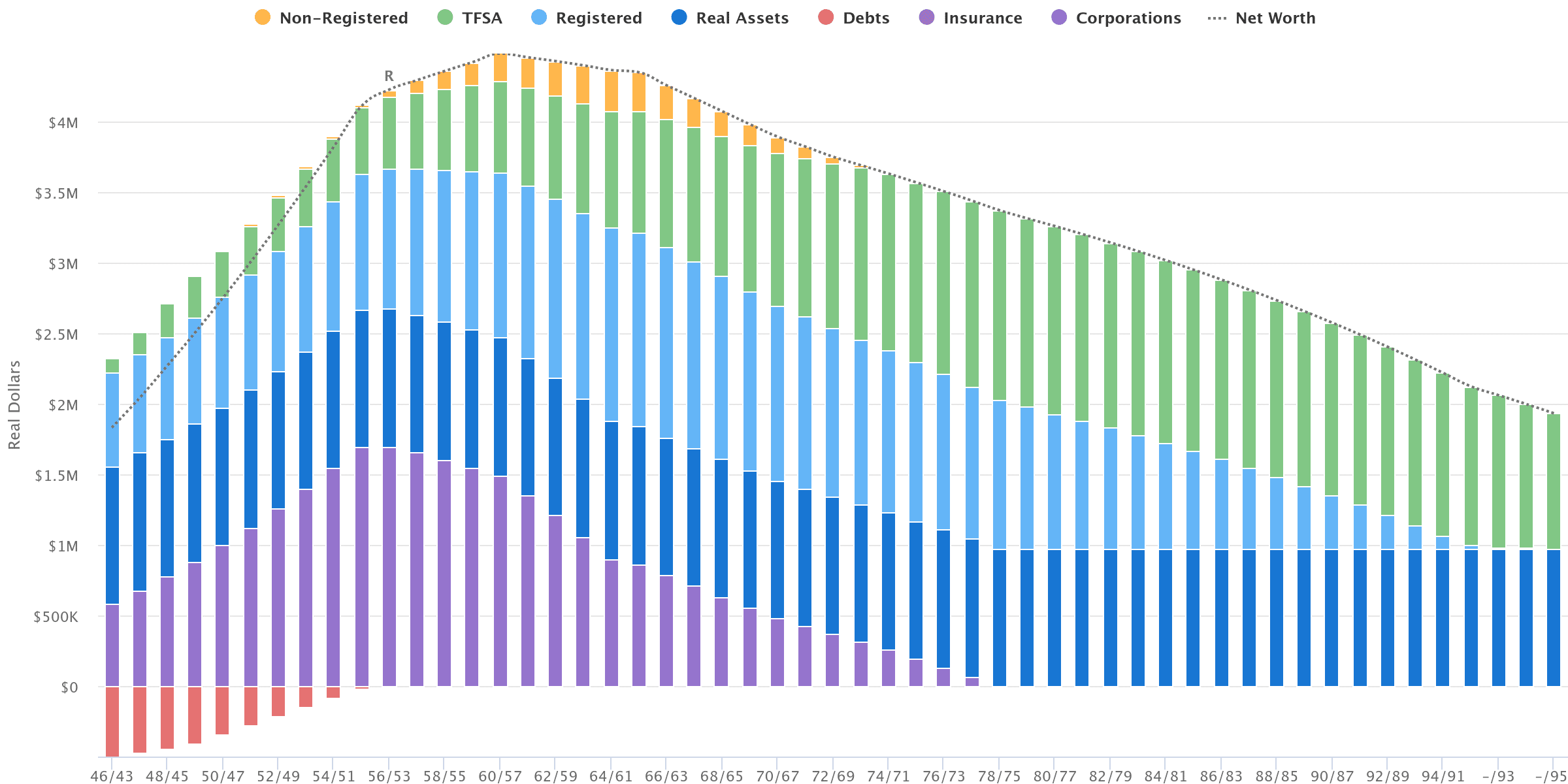

My wife and I have more complicated finances than most regular T4 salaried employees because we're incorporated and have built up significant assets inside our corporation that will need to be withdrawn in retirement.

So we need to be extra careful designing our retirement income to meet our desired lifestyle spending while also keeping tax efficiency in mind.

This takes a delicate approach that is highly influenced by our retirement date, or when we stop earning an income.

Work too long, and the window shrinks to get funds out of the corporation before CPP and OAS and ever-increasing RRIF and LIF minimum withdrawal requirements kick-in.

Retire too early (and spend too much) and you risk exhausting your resources before CPP and OAS come to the rescue.

With that in mind, my idea is to stop working full-time in 10 years (55), work at 50% capacity for five years (60) and then at 25% capacity for five more years (65).

This gradual reduction in earnings while maintaining current spending means that the balance inside the corporation will start to decline as soon as age 56. Ideally, we'd exhaust our corporation before age 70 – but according to the chart shown above we'd still have corporate funds until 78.

That's not as tax efficient as I'd like, but it's a direct product of still working in some capacity until age 65. And I think my own sense of purpose and well-being is more important than having the most optimized and tax efficient retirement plan.

In summary: retire earlier if you want to optimize your tax efficiency.

I'd also convert my RRSP and LIRA to a RRIF and LIF at 65 to take advantage of pension income splitting. This means the amount of dividends we'd withdraw from the corporation will decrease to make room for the incoming RRIF and LIF income – allowing our average tax rates to remain smooth and consistent even as new puzzle pieces enter the fray.

CPP and OAS benefits will be moved out of the way (delayed to 70) to allow for these significant withdrawals, which is fine by me because I'll take the enhanced and guaranteed income later in retirement.

Finally, there's the TFSA. Unlike some people, we do not treat our TFSAs as an untouchable source of funds. Yes, it makes sense to keep our TFSAs intact as long as possible and take advantage of that tax free growth. But we also want to maximize our life enjoyment, and that will mean using the TFSA to top-up our spending once other income sources dry up.

We also need to consider one-time expenses that are more difficult to plan for such as vehicle replacement, home renovations or repairs, early financial gifts to kids, and bucket list type travel and experiences.

In my view, a TFSA is a great place to draw from to fund those one-time expenses in retirement as the withdrawal is tax-free, does not affect your OAS benefits, and you get the contribution room back the following year.

Final Thoughts on Retirement Income

My wife and I will go from receiving one income stream each in our working years to dealing with a combined 12 different income streams or sources in retirement.

- Corp (2)

- RRIF (2)

- LIF (1)

- CPP (2)

- OAS (2)

- Non-registered savings (1)

- TFSA (2)

Each of these puzzle pieces needs to be carefully placed to maximize growth, maximize income, and minimize taxes. And because life happens and goals change, nobody (and I mean nobody) is going to do this with absolute perfection.

But you can see why even the most financial literate person or the most sophisticated do-it-yourself investor might want to work with a financial planner to build a retirement plan, model out some scenarios to see what's possible, and to stress-test their own ideas.

Clearly it's not as straightforward as simply withdrawing 4% from your portfolio and adjusting for inflation. Which portfolio? We don't have one bucket of money called retirement savings. You might have 8-12 different income sources to consider.

If you're five years or less away from retirement, it's worth reaching out to an advice-only planner to help fit all of your retirement income puzzle pieces together.

Hi Rob,

Great article, very informative. I’m trying to assist a couple whose affairs are fairly basic, husband and wife receiving OAS and CPP, only investments are GICs. Is there a ” free calculator ” that is available on the web which can produce nice infographs like in your article. I’m trying to show them the difference and the downside in only investing in GICs ( potentially run out of money, inflation, taxes etc )vs taking some equity risk like VBAL.

I appreciate any suggestions you have, thanks

Hi Lyndon, take a look at this article by another advice-only planner who spent time reviewing all of the free retirement calculators out there and ranked them best to worst. I’m sure you’ll find an option from the list that will give you the visuals you’re looking for:

https://www.evansretirement.ca/blog/best-free-retirement-calculators-canada

Thanks Robb, much appreciated

Lyndon

I believe OAS has stopped automatically paying pension benefits at 65 because of the premium for waiting. I was sent an application 11 months before my 65th birthday to complete in order to receive it when first available. I presume too many people got auto pay when they wanted to wait. There’s also a spot somewhere on the service canada site where you can click a button saying you don’t want it automatically. Again, not sure if that was a crossover fix, but for me payments will start when I ask for them.

Hi Frito, I don’t think so. Service Canada still states that:

“In most cases, Service Canada will be able to automatically enroll you for the OAS pension if sufficient information is available. Service Canada will inform you if you have been automatically enrolled.

If you did not receive any letter about the OAS pension the month after you turned 64, you may need to apply for the OAS pension.”

Ok. I was sent the full application package so won’t get it till I complete it. Just checked my account and they have nothing in progress even though my BD is very soon. I guess I’ll wait and see if my inaction results in a cheque in the mail! 🙂

Upcoming OAS payment dates are Jan 29th, Feb 26th, and March 27th.

You should receive your first payment in the month *following* your 65th birthday.

My hunch is that you will receive a payment automatically. Let us know if that isn’t the case.

Just remembered to update you on this…I received NO automatic payment after turning 65. No reason I can think they wouldn’t have enough info on me as I file regularly, get direct deposit on all government rebates and haven’t moved for 12 years.

Soooo… if I wait until 70 to take my OAS I’ll get a bigger cheque each month. How does that link up with the CRA clawback? If my income is somewhat higher than the threshold (it will be), will I have a fixed dollar amount clawed back or a percentage of my OAS clawed back? If they hold back a fixed dollar amount instead of a percentage of my OAS entitlement, that would be a better result for me… right? Although the higher OAS payment will kick me even further past the threshold. I’m getting really confused!

Hi Sandra, if you really want to blow your mind then read this advanced analysis from Aaron Hector about how the enhancement and clawback work together: https://www.linkedin.com/pulse/real-oas-deferral-enhancement-aaron-hector-cfp-r-f-p-tep-sqo5c

TL;DR – if clawback might be an issue for you then deferring to 70 can make really good sense.

Robb, a thousand thank-you’s for the link provided to Sandra ! I’ll be 64 this year, have been retired for a few years now, and blessed with a DBP. So I have a bit of a potential clawback issue with regards to the upcoming OAS.

I am delaying CPP to age 70 – a no brainer for me. But for the last few years I’ve been trying to figure out whether or not to delay OAS too. The big question for me was how the clawback ceiling worked (the actual number) for those who chose to delay. I could never find this information anywhere. That linked article, with the examples provided, sealed the deal for me. Again, thanks. I’m really grateful for today’s article and your comment section !

Hi Robb,

Is there a free calculator or some kind of software that would do the calculation for my wife and I? We need answers to all of these.

Eg. When’s the best time to start CPP/OAS?

Should we do a RRSP meltdown?

What’s the best strategy for a couple with a 10 year gap in age?

Basically a software that would tell us what’s the best thing to do to get the most $$ in our pockets.

Thanks

Hi Ben,

So after reading 1,600 words about the challenge of putting all your retirement income puzzle pieces together, your question is if there is a free calculator that will answer all of this for you?

And if there was (there isn’t), and I knew about it (I don’t), that I would willingly gate-keep it from all of you (I’m not!) just so you have to pay (me) for a retirement plan unique to your specific circumstances?

It’s quite frankly an insulting question.

Similar situation to you Robb with a corp investing account to consider. Right now I am thinking about retirement at 58-60 once kids are launched. From retirement to age 70 melt down corp account which should be $2.5-3M starting point and possibly some withdrawals from RRSP if needed (may put a small chunk of RRSPs into RRIFs to do this). Delay CPP to 70 but take OAS at 65 to get six years of it before its fully clawed back starting at 71 when RIF minimums will be large enough to eliminate OAS. Will play with income during these years to try to keep OAS with no clawback at all. Will build up savings pre-65 to have extra non-income cash available. From 71 onwards our large RRIFs, CPP and non-reg dividends will be more than enough. Leave TFSAs for LTC needs or helping kids buy homes, etc and if not, pass to the kids tax free as part of our estate.

I think this is a nuanced approach to retirement:

With that in mind, my idea is to stop working full-time in 10 years (55), work at 50% capacity for five years (60) and then at 25% capacity for five more years (65).

Allows someone to find other passions and purposes over time instead of full-time to no-time which seems to have mixed results.

Appreciate you sharing this. Would like to model this approach.

As for calculators; thereare no free ones around that do it all, believe me I have looked. However there is a young company in London that I have started to use. The software is called Adviice (two iI’s). It is only $9 a month and you can stop the subscription at any time. You can add different scenerios such as a RRSP melt down, CPP and OAS at different times, what funds to draw from next etc.. I have no affiliation with the company. I just wanted people to know how well it has worked for me. There are lots of You Tube videos on line explaining the in’s and out’s of the software.

Cheers

Hi Rob – I found your very informative website and newsletters over the last month as my husband and I ruminate over some critical asset re-allocation / de-risking decisions related to our (equity and tech heavy) portfolio, now that we’ve retired.

As we discuss rebalancing, de-risking and de-cumulation strategies a question arose which I thought I’d pose to you. It relates to the non-registered portion of our portfolio (valued at $1million and representing 15% of our combined portfolios).

Up until we retired in early 2023, all non-registered was in my name only (for potential cap gains tax purposes as my husband’s annual salary was quite a bit higher than mine). Upon retirement we made it joint for beneficiary survivorship purposes. If /when we sell any of those stocks does the ‘date it became joint’ come into the capital gains / tax equation or does CRA consider it “joint” (full-stop) and all gains can be split 50-50 for tax purposes.

Many thanks for your insights on this.

Hi Wendy, you can make the account joint for estate planning purposes, but for tax purposes the income and gains are still attributed back to you since that’s where the money originated from.

Murkier if you start adding new contributions jointly – but if all the contributions went in from your income as the sole account holder then all investment income and future gains would be attributed to you.

Some further reading here: https://financialpost.com/personal-finance/family-finance/fp-answers-what-are-the-tax-implications-of-joint-investment-accounts

Thanks Rob, for such a timely reply and providing the FP link. We assumed there would be some such rule (but I wasn’t phrasing my Google search well enough to find it!). This is very helpful information – when determining the most tax efficient strategy for drawing down funds from our various accounts. The ‘de-accumulation’ stuff is complex! 🙂

Best,

Wendy