Vanguard’s Asset Allocation ETFs – Five Years Later

It has been five years since Vanguard introduced the first asset allocation or “all-in-one” ETFs in Canada. Simply put, these one-ticket solutions have been an absolute game-changer for do-it-yourself investors.

I’m on record to say that if investing has been solved with low-cost index funds, then investing complexity has been solved by using a single asset allocation ETF. Yes, it can be that easy.

I put my money where my mouth is by holding Vanguard’s All Equity ETF (VEQT) in my RRSP, TFSA, LIRA, and corporate investing account. Many of my financial planning clients also hold asset allocation ETFs in their portfolios.

Related: How I Invest My Own Money

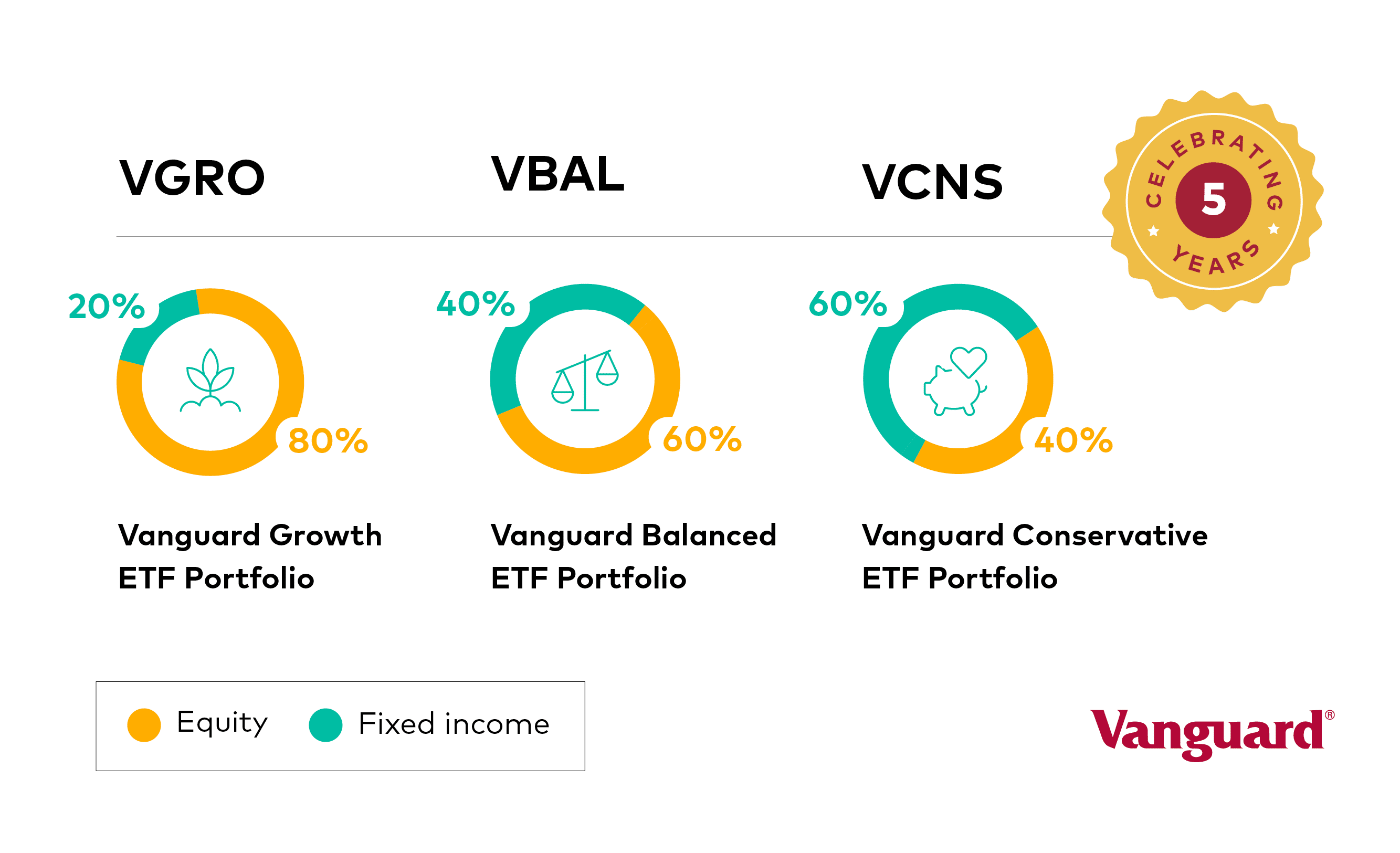

It started back in 2018 with the launch of three asset allocation ETFs; Vanguard’s Conservative ETF Portfolio (VCNS), Vanguard’s Balanced ETF Portfolio (VBAL), and Vanguard’s Growth ETF Portfolio (VGRO).

Vanguard later added an all-equity version (VEQT), a conservative income ETF (VCIP), and the retirement income ETF (VRIF) to complete what it calls the full range of risk profiles for investors and retirees.

In the last five years, Vanguard’s asset allocation ETFs have grown to almost $9 billion in assets under management – making it one of the fastest-growing investment products in Canada. VGRO is the most popular with $3.8 billion in assets, making it the 17th largest of the 1,000+ ETFs in Canada.

There’s a reason why “just buy VGRO” is the mantra for many enthusiastic DIY investors on Reddit.

I spoke with Sal D’Angelo, Head of Products for Vanguard Americas, about the impact Vanguard’s asset allocation ETFs have had on the Canadian investment landscape.

He said the company felt good about launching a brand new ETF category, given the appetite for balanced funds in Canada.

“Approximately half of the $1.89 trillion in mutual fund assets are held in balanced funds,” said D’Angelo.

The value proposition for asset allocation ETFs have certainly been enticing enough to (slightly) disrupt the balanced mutual fund market. After all, why pay nearly 2% MER for a balanced mutual fund when you could hold a balanced ETF for nearly 1/10th of the cost?

“We’ve definitely seen bigger growth than expected over the past five years,” said D’Angelo.

The Vanguard Effect on Asset Allocation ETFs

Imitation is the sincerest form of flattery, but nothing new for Vanguard. The so-called ‘Vanguard effect’ is real. Shortly after launching VCNS, VBAL, and VGRO many other asset managers launched their own suite of asset allocation ETFs.

The category is booming, with industry assets under management now at ~$14 billion dollars and growing. While that represents just over 4% of the ETF industry, the category is generating between 5-10% of industry flows (new money) over the past three years.

“We’re flattered that others have emulated the product,” said D’Angelo.

Vanguard believes, the more low-cost, simple-to-understand and broadly diversified products there are available, the better for Canadian investors.

Five years represents a significant milestone when it comes to benchmarking performance against its category peers, and Mr. D’Angelo was eager to highlight the performance of Vanguard’s asset allocation ETFs.

- VGRO beat 92% of category peers over 5yrs, 85% for VBAL, and 53% for VCNS.

- VGRO and VBAL were just awarded a FundGrade A+ Award in 2022, which is awarded for funds that demonstrated outstanding risk-adjusted performance. Only about 6% of eligible funds available in Canada win this prestigious award.

- VEQT was also a winner of the FundGrade A+ Award but was not part of the original three ETFs that launched back in 2018.

Is the 60/40 Portfolio Dead? Nope

While on the subject of performance, I asked Mr. D’Angelo about the 60/40 portfolio given its historically bad year in 2022.

He said the 60/40 portfolio is alive and strong and will continue to serve investors well over the long term.

“Past research has shown that these types of difficult years happen occasionally, but the benefit is that long-term valuations for stocks and bonds are attractive moving forward,” said D’Angelo.

- Stock-bond declines are not long-lasting: Looking back to 1976, simultaneous losses in both U.S. stocks and bonds have only occurred 0.4% of the time, on a 1-year rolling return basis.

- The 60/40 portfolio was negative only 14% of the time on a 1-year basis and 0.6% on a 5-year rolling return basis.

- The stock-bond correlation remains negative in the long-term – Our study of 60-day and 24-month stock-bonds rolling correlations from 1992 to 2022 suggests that over the long-term, the correlation between stocks and bonds remains negative. That said, long-term inflation is one of the determinants of correlation between the two asset classes.

Mr. D’Angelo says that bonds will continue to act as a ballast to the portfolio:

“High-quality bonds reduce the impact of a market downturn in a multi-asset portfolio, as seen in 2008 and more recently in 2020.”

Also, more than 90% of bonds’ total return is generated by coupons, not capital appreciation. In a rising interest rate scenario, negative returns generated by price declines can be more than offset by higher coupons if an investor’s time horizon is longer than their bond portfolio duration.

Finally, current interest rates / coupons are favourable, with high-quality bonds yielding 4-6%.

I agree with this assessment and remind VBAL investors that the balanced fund had outstanding returns from 2019 to 2021 before suffering losses in 2022:

- 2019 – 14.81%

- 2020 – 10.20%

- 2021 – 10.29%

- 2022 – (-11.45%)

“Vanguard research expects average annual returns of about 7% for a 60/40 balanced portfolio over the next 10 years,” said D’Angelo.

Final Thoughts

You won’t find a bigger fan of asset allocation ETFs than me. I invest my own money in VEQT. Many of my financial planning clients use asset allocation ETFs in their portfolios. Heck, the entire premise of my DIY Investing video series centres around how easy it is to hold a single asset allocation ETF so you can move on with your life.

I’m grateful to Vanguard for launching this category and making it easy for DIY investors to manage their own low-cost, risk-appropriate, and globally diversified portfolio.

The good news is, after five years, we’re still in the early innings of adoption for asset allocation ETFs. I fully believe that more and more investors and advisors will understand the importance of cost on investment returns over the long term and will continue to adopt low-cost asset allocation ETFs in their portfolios.

When you say “DIY” would one have to speak with their investment advisor to move money to a VEQT? I have about 5 yrs. left before I start drawing from investments, is it too late or even worth the move at this point? I mean 5 yrs. isn’t exactly considered “long term” is it?

I forgot to ask a somewhat ignorant question, could I ask my FA to invest in Vanguard for me?

Hi Gert, it really depends on where your money is and what kind of advisor you have. Some advisors do purchase ETFs for their clients. You should ask about ETFs or about lower cost “F-Series” mutual funds.

The other question is around what’s appropriate for your age and stage of life. VEQT is 100% global stocks, and may not be appropriate for someone five years away from withdrawing money (I’m 43 and possibly 20 years away from withdrawing money).

I wonder why pay an advisor to buy an ETF where you could buy yourself, saving the 1% or more you pay your FA?

Hi Denis,

Thanks for the advice. My FA has spoken to me about ETF’s in fact he’s making a move away from mutual funds altogether in my portfolio. I’ve my position known about fees. I think someone like me needs his hand held because I’m still afraid to make a mistake. At my age I’m weighing the risk over fees. I pick up the phone or send a text and my FA gets back to me right away, as many times as I want to talk about anything that concerns me.

I started with mutual funds when I started saving and investing, decades ago. I found out fast that it was a losing proposition with the obscene fees. Wish there were ETF’s then. I wouldn’t have had somuch volatility in my portfolio getting into stocks and past decade, options vs ETF.

Hi Gert, saving more than 1.5% on fees over 5 years before you start withdrawing is not insignificant. As well, the fee savings continue on your capital long into the withdrawal years. We moved from some insurance company mutual funds in to VBAL 5 years ago and wished it had been available long before. My FA never wanted to talk about ETFs. I wonder why?

My FA (or more accurately my former FA), also never wanted to talk about ETFs, and in fact didn’t want to tell me what my underlying fees were, until I accused him of ‘hiding the ball’. I’m all in ETFs now.

When you made this move were you able to speak with someone to have the move made, or do you have to set everything is yourself?

Do you speak with anyone on a quarterly basis?

In percentage how much are you saving in fees?

Thanks!

Hi Bill,

When you made this move were you able to speak with someone to have the move made, or do you have to set everything is yourself?

Do you speak with anyone on a quarterly basis?

In percentage how much are you saving in fees?

Thanks!

It would be great to have you look at performance of the various etf all allocation products against their peers…Vanguard, BMO, iShares, Horizon.

Hi Geoffrey, the Canadian Portfolio Manager blog (Justin Bender) does this for his model portfolios each year: https://www.canadianportfoliomanagerblog.com/model-portfolio-returns-for-2022/

Once all of the peers have a five-year track record I can look at doing a broader comparison.

I wouldn’t expect much long-term difference between the ones that track broad market indices (Vanguard, BMO, iShares).

Great – thanks for the link/ info. I guess small nuance’s really between… interesting that BMO is taking a slight active role in some.

This was my question too, returns and fees will be very similar I suspect, it’s almost become a homogeneous product category

Would you use VEQT and GICs or VGRO inside your Corporation (CCPC)? I plan to keep at AA 80/20 for a long time.

I am hoping I can keep using VGRO where I don’t do any work. I know that I pay more MER and more taxes for the bonds portion of VGRO.

Your thoughts? I have a good size CCPC.

Hi Liam, I hold VEQT in my corp but there’s nothing wrong with using the other asset allocation ETFs like VGRO or VBAL. The thing to watch for is the total investment income earned annually as you can run into tax issues once that gets beyond $50,000.

VGRO distributes around 2.2% of the total balance each year in income (dividends and interest) so you’d need to have $2M+ invested before that became an issue.

The Horizons’ funds are also worth considering in a taxable account as they don’t churn out annual investment income (they use a total return swap to convert the income into deferred capital gains). There are risks to this approach, as the Horizons funds are less diversified than the Vanguard funds and subject to potential regulatory risk (the gov’t potentially disallowing the total return swap approach in the future).

Also keep in mind with the VEQT + GIC approach that the interest income from GICs is fully taxable.

Curious: What do you hold in your non-registered accounts if you have VEQT in all your registered accounts.

Hi Joe, I don’t have a personal non-registered investment account but I do have a corporate investing bc account (a taxable account for my small business) and invest in VEQT.

If you want to keep things simple then just hold the same asset allocation ETF across all account types rather than trying to get cute with the “correct” asset location.

Hi Robb, I have taken a wait and see how you do approach. I am glad you did well. How does your VEQT compare so far to the market?

Have you noticed the new BMOallocation etfs that now give a 6% cash distribution? That might help me as I move to RRIF age of 72 in 5 years. Then I wouldn’t have to sell units for my RRIF withdrawals as much. Can you analyze the MER for us. I’m confused a little. They say it’s 0.2%. But is that on top of the underlying MERs, I hope not because if it is that gets expensive.

Is the MER on your VEQT in addition to the underlying ETFs it holds?

Thanks Rob. I may eventually get to where you are. I am not convinced that the INtl wtf component is a good idea as its performed poorly most years apart from a few and tends to be more volatile. What are your thoughts on that too?

Hi Steve, I’m not sure I understand your first question. VEQT, by definition, is invested in all global markets (Canadian, US, international, and emerging) so its returns track those markets closely. Total return was 19.66% in 2021 and (-10.92%) in 2022.

The MER is 0.24%. There is no double dipping of fees with the underlying ETFs (a common misperception).

The idea of investing globally is that we don’t know which markets will outperform in the future. For instance, many investors think they should just buy the S&P 500 because US equities performed so well over the previous decade. But they forget (or don’t know) that US equities had a lost decade in the 2000s (while Canadian stocks performed well).

Last year’s winners seldom go on to be this year’s winners. By investing globally, we capture the returns from all markets and can get a more reliable return (with less volatility) over the long-term.

I’m not aware of any BMO asset allocation ETFs distributing 6%. You may be thinking of a monthly income ETF or their covered call ETFs (not the same thing – these are active strategies).

Thanks Robb for another great read. I am invested in VBAL in multiple accounts and I must admit that I have had some concerns due to the recent lackluster return from bonds, but I am staying the course. Bond returns should rebound in the near term and I was happy to read about the 7 percent return prediction from Vanguard .

What are your thoughts on using asset allocation etf’s during the “decumulation” stage in retirement. Would you just sell off what you need, even after a market setback?

Hi Dave, it’s perfectly sensible to hold an asset allocation ETF throughout retirement and sell off shares as needed to meet your spending needs.

You can mitigate the pain of withdrawing in a down market by holding a year or two worth of withdrawals in cash (high interest savings or HISA ETFs).

But you’ll still need to refill that cash bucket every so often, which means selling some ETF units (along with using the quarterly distributions). In that case I’d recommend “reverse” dollar-cost-averaging – selling off a small number of ETF units every month until you’ve reached your desired amount of cash.

One thing I was a bit surprised to realize with XEQT and VGRO is that they allocate a portion of their distributions as “Capital Gains”. It took a while for me to figure out these phantom distributions as my T3 was showing I had significant capital gains and I did not sell any ETFs to trigger them. These capital gains increase you ACB. I’m not a fan of paying capital gains tax up front but it is what it is. A word of warning, ensure you are tracking your ACB yearly to ensure you don’t get double taxed on any capital gains when you do decide to sell! Robb, I’m curious what your thoughts are on these phantom distributions?

Hey Justin, thanks for your comment. Definitely something to be mindful of when you hold ETFs inside a taxable account. All the more reason to keep things simple in those accounts.

This article on phantom distributions is worth a read: https://www.bmoetfs.ca/articles/what-are-phantom-distributions-from-etf-2

“An ETF may incur capital gains if an underlying security in the ETF’s portfolio is sold for more than its purchase price. An ETF’s capital gains are paid out annually as reinvested distributions. In that case, no cash payment is made. Instead, it is automatically reinvested into the ETF, which results in an adjustment of the unit price, but it doesn’t change the number of units held.

As a result, an investor’s adjusted cost base (ACB), which is the average cost of the purchase of the security, is increased by the amount of the reinvested distribution. The reinvested distribution adds to the investor’s adjusted cost base, resulting in a lower capital gain once the ETF is sold and ensuring double taxation is avoided.

What happens when ETF distributions are paid in cash?

Investors do not adjust their ACB if there are cash distributions of realized capital gains throughout the year since the NAV is decreased by those distributions. This adjustment may be handled by the broker or dealer where the ETF was purchased.”

Hi Robb,

I’m waiting with keen anticipation for your reply to Dave McCullough’s posting on March 7, 2023 at 4:35 am regarding the use of asset allocation etf’s during the “decumulation” stage in retirement.

Thanks!

Cary

Got to it just now – thanks for the reminder!

Happy birthday!!!

So given “In the last five years, Vanguard’s asset allocation ETFs have grown to almost $9 billion in assets under management – making it one of the fastest-growing investment products in Canada.” and Sal D’Angelo’s, “We’ve definitely seen bigger growth than expected over the past five years” when is Vanguard going to follow Bogle’s practice of sharing economies of scale with investors by lowering MERs?

After all, an MER of 25bp on $9B in assets is $22.5M in revenue from these ETFs.

[Oh, the irony…]

Hi Bylo, I don’t imagine you’ll have to wait long. They’ve already dropped the MER a tick down to 0.24%.

This fee reduction has already happened with VXC (all world ex-Canada). iShares came in with XAW and undercut Vanguard’s fee. But now VXC has a MER of 0.21% and iShares’ XAW is 0.22%.

Vanguard isn’t known for being the second lowest cost provider in the industry, and they’re constantly reducing fees on various funds each year.

Hello Robb,

Thanks for all the amazing info and feedback over the years! You’ve been a great help!

In line with your drive for simplification (using an all-in-one ETF), I still wonder about the value of diversifying somewhat into a product such as iShares Bitcoin ETF to get some exposure to that segment of the market?

Hi Max, thanks for the kind words. Bitcoin isn’t for me, but there is an all-in-one ETF from Fidelity called FEQT that has small exposure to bitcoin and ethereum.