Prospective clients come to me when they’re on the cusp of retirement and looking for answers to key questions like when can I retire, how much can I spend, how long will money money last, and, ultimately, am I going to be okay?

I gather information about their current situation (income, account balances, asset allocation, expected income from a pension and/or government benefits, property value, debts, etc.), and ask them to list their financial goals and burning questions.

Then I plug those numbers into my financial planning software to model out my interpretation of their current situation and future goals to see what’s possible. Your numbers are going to tell a story, whether there are obvious opportunities to take advantage of or red flags to consider.

I use conservative assumptions for life expectancy, rates of return on savings and investments, and assume spending will increase annually with inflation.

One common observation I notice is that the early retirement years can often be financially precarious. That’s when new retirees want to spend the most money on travel and hobbies. It’s also a period of time that often overlaps with the desire to help children through post-secondary and into early adulthood.

Throw in a new vehicle and a home renovation into the mix and you can easily see the financial stress signals mounting.

Meanwhile, early retirees haven’t yet taken their government benefits, so they may be drawing significantly from their own savings (RRSPs, TFSAs, non-registered accounts) to make all of this work.

Not to mention poor stock market outcomes causing sequence of return risk.

I call this the retirement risk zone.

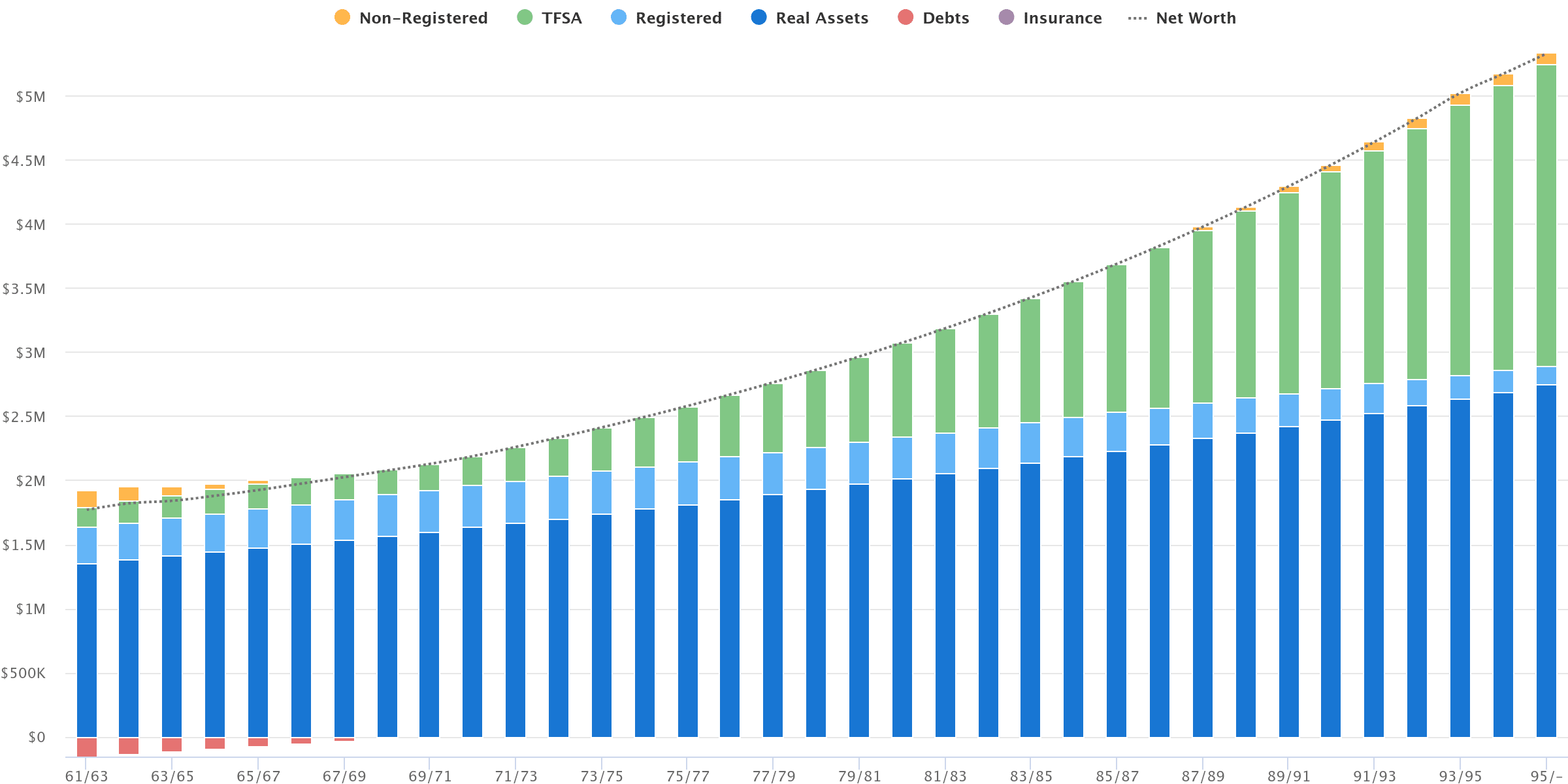

This can be a frustrating time for seemingly well-heeled retirees because they might see their retirement projections look something like this:

Your numbers tell a story, and the story here is a couple retiring with a net worth of $1.8M. Sounds great, except for the bulk of net worth is tied up in their home ($1.3M). And while they have about $600,000 in savings, they also still have a mortgage balance of $100,000 as they enter retirement.

See the dilemma? The couple sees their net worth taking off in their 70s and beyond (once CPP and OAS are fully kicked-in for the couple) and wants to pull some of that forward to spend more now.

But that’s not possible without tapping into home equity (downsize, sell and rent, or borrow on a line of credit). That solution is not appealing for this newly retired couple.

It might be tempting to take up their CPP benefits early (ages 61 and 63, respectively), but they’d be giving up a permanent reduction in their benefits and a lifetime loss of income. Instead, they’ll wait and take their CPP at age 66 along with OAS at age 65.

With the home equity release strategy off the table for now, the couple must spend carefully in these early retirement years to make sure their savings will last.

That means being “selfish” to ensure they can meet their desired spending needs over the next 5-10 years of early retirement (their go-go years).

Selfish because this does not appear to be the time to hand out large financial gifts to their children. Put on your own oxygen mask first before assisting others, as the saying goes. Take your own bucket list trip before emptying your TFSA to fund a child’s down payment.

But, as your CPP and OAS benefits kick-in and boost your guaranteed income floor, and as the go-go years of spending wane, you might find yourself in an annual surplus and even contributing to your TFSAs again.

That, and you might re-consider selling the home as you age – which will top-up your savings buckets.

If your spending needs are being met, you have a surplus of cash flow, and you have an appropriate backstop of home equity and TFSA funds, then it makes perfect sense to explore an early giving approach with your child(ren). Give with a warm hand, before the will is read.

Indeed, rather than continuing to max out your TFSAs while your own spending declines in real terms and you’re still sitting on a pile of home equity, consider your 70s as a time for generosity.

Think about it. Your kids might be in their late 30s, or early-to-mid 40s. A gift of $100k is arguably more valuable and significant at that age than an inheritance of $500,000 when they’re in their 60s and already retired.

It doesn’t have to be $100k – whatever you can reasonably afford in the context of your plan. It could be something as small (yet meaningful) as an agreement to fund your grandkids’ RESPs annually ($2,500/year). What an incredible gift and a relief for young parents trying to balance competing financial priorities in their own lives.

Your generosity could be in the form of buying more time together as a family. One retired couple I’ve worked with pays for the entire family to go to Hawaii for a week each year – covering the airfare and accommodations so that their two children and their families can come together for a relaxing vacation.

The point is, you can scale your generosity to match your financial capacity and values (of course, respecting the needs of your children and their independence).

The key is to talk about it so everyone is on the same page and expectations are properly set.

So, rather than just filling up your TFSAs each year as your own spending declines – I’m making the case for some level of generosity into your 70s and beyond to prevent an overly large final estate and to help give with a warm hand.

You can still leave yourself with a reasonable margin of safety (home equity + TFSA balance) without getting too carried away with growing the pile.

The time to do that is not in your early 60s, when finances are a bit more precarious, but in your 70s and 80s as your personal spending slows down and your net worth starts to climb once again.

Retired readers: Are you providing financial assistance to your adult children in any capacity? How do you balance this in relation to your own retirement plan and resources?

It has been more than 10 years since I started offering financial planning advice – and more than five years since I quit my day job to work as an advice-only planner full-time.

I have a soft spot for who I call regular Canadians with regular problems. That’s the majority of you who read this blog – typically you’re T4 salaried employees, some with pensions, others with employer-matching savings plans, and many more just doing their best to balance living for today with saving for the future.

This is the mass market – one that has struggled to access quality financial advice over the years. You’re working with a bank-branch or investment firm advisor selling high fee mutual funds, or got roped into a financial MLM’s insurance-based investment scheme by a friend or relative. Worse (maybe), you’re just going it alone and following tips from your favourite finfluencer(s) online.

These folks need good financial advice at certain ages and stages of life, whether they’re starting a family, buying a home, changing careers, receiving an inheritance, or gearing up for retirement.

And while there are some fabulous financial advisors in Canada, most of them aren’t tripping over themselves to work with the mass market. Instead, the best of the best are working with high or ultra-high net worth clients.

Cool.

Imagine the time and resources spent on scenario planning for the 0.13% who might have been affected by the now (likely) dead increase to the capital gains inclusion rate. Not my idea of fun.

Advice-only planning, at least my version of it, aims to help the mass market and give them a fighting chance to survive in an increasingly complex financial world.

I’ve written an astonishing number of financial plans over the past three years (451 to be exact).

But I’m only one person and the mass market is, by definition, massive. And not everyone has the means to pay for advice, or is not yet at a stage where a financial planning engagement makes sense. That’s where this blog comes into play. There’s a good 12,000 of you who subscribe and read regularly, and tens of thousands more who poke your head in from time-to-time.

Last weekend I was busy with kids’ activities and didn’t get around to writing a Weekend Reading update. That was a mistake, because many of you were busy freaking out over the threat of tariffs and wondering if you should hit the panic button and sell before the market opened Monday.

Indeed, I received at least a half dozen emails from concerned readers about exactly that.

So I quickly took to social media to put out a Keep Calm and Carry On message:

Markets have been through a lot in the past hundred years (heck, in the past five years) and continue marching on over the long term.

Unless you got way over your skis (leverage, too much risk, too concentrated) then just stick to your sensible, low cost, globally diversified strategy.

— Robb Engen (@boomerandecho.bsky.social) 3 February 2025 at 06:53

Meanwhile, I try to train my clients to be emotionless robots when it comes to investing, but it’s easier said than done when everything feels scary and uncertain:

Hi Robb, while I do tend to err on the emotionless robot side when it comes to investing, there has been so much talk about these tariffs and I wonder if this is a situation when we would want to make some changes in investment strategy, allocation etc.

I’m guessing you’ll say don’t change anything, same as always but wanted to ask regardless haha.

and:

Hey Robb,

I’ve never seen a trade war before but I can’t imagine this is good for the markets. I’m assuming your recommendation is to just keep investing with the dollar cost averaging mentality?

Notice how they both knew what I was going to say, but I think they just needed to hear me say it again this time?

Finally, my absolute favourite message was from another client (who’s friends with another client):

I was freaking out last weekend with all the crazy stuff about tariffs. I did not do a thing. And you were right!

I almost emailed you, but I talked to (other client / friend) and she said, “do not bother Robb – he has taught us.”

I love it.

So what exactly is a regular Canadian with regular problems?

My ideal client is an individual or couple who is 3-5 years away from retirement and looking for a roadmap. They want to know if they can retire at their desired date, how much they can safely spend, and ultimately if they’re going to be okay.

They want to know if they’re paying too much in fees in a managed portfolio, or if their self-directed portfolio is appropriately allocated.

They want to know if they can travel more, or help their children get through post-secondary and/or buy a house one day.

That’s my wheelhouse. But I also have many clients in their 30s and 40s who want guidance on how to maximize their life enjoyment now while also saving for the future. I have many clients who are already retired and want a tax efficient withdrawal of their resources. And I have an increasing number of clients who are dealing with an influx of money from an inheritance, settlement, or insurance pay out.

Okay, so who is NOT a regular Canadian with regular problems? Well, let’s say you own a business (not a sole proprietorship or a “freelance” business like mine, but something more complicated with employees and widgets, or other business partners), or you’re a US citizen, or you plan on leaving Canada or retiring outside of Canada, you receive regular stock options or other equity based compensation, or you own multiple rental properties (or foreign properties), to name a few.

Complexities like that deserve more time and expertise than I can offer. When I receive requests from folks with those issues, I typically refer them to other rockstar advice-only planning firms such as Spring Planning, Objective Financial Partners, or Modern Cents.

There are others, but in general I’ve found that more and more financial planners have co-opted the advice-only planning label but also offer investment management for a percentage fee.

I believe true advice-only planning separates advice from product sales. That’s just me. The trade-off, and a frustrating aspect of advice-only planning, is that I’m just giving advice. It’s up to my clients to accept and implement that advice.

Which leads me back to my point about keeping the blog up-to-date. If you’re a client, you should be following the blog and subscribing to email updates. When I publish something, I’m speaking to you (and many more like you) about good financial decision making and (hopefully) reinforcing the more specific advice I have given you.

Next weekend we’re heading to Cancun to escape this never ending winter freeze. Meanwhile the RRSP deadline is fast approaching. To head-off dozens of emails about RRSP contributions, I should probably publish a quick blog post explaining how to think about optimizing your RRSP contribution for the 2024 tax year.

This Week’s Recap:

In my last post I opened up the money bag to answer reader questions about investment loans, optimizing your RRSP, underspending in retirement, and more.

Prior to that I wrote about putting your retirement income puzzle pieces together.

And my last Weekend Reading looked at the power of simplifying your finances.

Promo of the Week:

Wealthsimple is back with an even more generous transfer bonus promotion that they’re calling their Big Winter Bundle Promotion.

What’s included in this new transfer bonus promotion?

- 2% cash back match on RRSP, spousal RRSP, and LIRA transfers

- 1% cash back match on TFSA, FHSA, and other eligible transfers

- 5 lift tickets for referring friends, setting up your first direct deposit, and more

New and existing Wealthsimple clients can qualify for the match offer.

In order to receive the match bonus, the client must have a Wealthsimple Cash account.

The match bonus will be applied as 24 equal monthly payments to your Wealthsimple Cash within 60 days after the full net funding amount has settled.

Open your Wealthsimple account here, and then register for the Big Winter Bundle promotion to get yourself some cash back.

I’ve helped hundreds of clients and readers set-up their own self-directed investing accounts and start investing with a single, risk appropriate asset allocation ETF. You can do this!

Weekend Reading:

YCharts is debunking investing myths such as “investing is like gambling”.

Financial planner Markus Muhs looks at true long-term investing and why recent returns can be misleading.

On a similar note, Dan Hallett says if you’re piling into US stocks don’t expect the past decade to repeat.

Mark Walhout takes a thorough look at the health conditions that may necessitate a stay in long term care, the different types and levels of long-term care support in Canada and their associated costs, and how retirees should be planning for the potential costs and lifestyle impact that a move to long-term care will bring:

Fred Vettese looks at whether minimum RRIF withdrawal rates are too high (G&M subs):

There’s indeed an argument if returns are too low (or the portfolio is invested too conservatively) and the retiree has a long life expectancy.

Finally, a double-shot from A Wealth of Common Sense blogger Ben Carlson. First he describes the perfect level of wealth.

Next, does buying the dip actually work? In theory, yes. But not so much in practice.

Have a great weekend, everyone!

Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

Today, I’m answering reader questions about borrowing to invest, optimizing your RRSP, market timing, the reluctance to spend in retirement, and switching from dividend stocks to index funds.

First up is Andrea, whose financial advisor is trying to talk her into setting up an investment loan. Take it away, Andrea!

Should I borrow to invest?

My advisor suggested using a HELOC, paying only the interest, and using the rest to invest (obviously in hopes of gaining a higher return than the cost of the HELOC interest). Do you think this is a wise idea?

Hi Andrea, I’ve recently helped several clients extract themselves from unnecessary investment loans. It’s one of those ideas that looks good on paper but is not so great in real life.

Interest is tax deductible, yes. But that’s a one-time savings when you file your taxes. You still need to service the loan interest each month.

What are you investing in? It should be high enough exposure to equities to give you a higher expected investment return than the loan interest, but not too risky (betting on individual stocks) and not too expensive (what kind of fees are you paying to your advisor?).

Stocks can fall sharply (34% in March 2020, or down 12-18% in 2022 depending on the index).

How would you feel about a $140,000 market value when your loan is $200,000?

Investment loans are great for investment advisors because they get a loan on the books and an investment to manage (from which to extract fees).

Finally, are your other goals being fulfilled (optimize RRSP, maximize TFSA, prioritizing other goals like living your best life)?

All more important than creating a tax deductible investment loan.

What does it mean to optimize your RRSP?

Next up is Tim, who wanted clarification on my suggested way to optimize your RRSP contributions when you have an employer matching RRSP.

In a recent Weekend Reading edition, you suggest to ”contribute enough to max out the match, but no more” when it comes to employer matching savings plans. Why not contribute more?

Let’s say someone earns $100,000 per year and can contribute 18% of his income to RRSPs. At work, five percent would come from the employee and five percent would come from the employer’s match, for a total of 10%. But what about the remaining eight percent? Why not maxing out the RRSP with the employer only? What are the cons with this approach?

Hi Tim, the answer is a bit nuanced. First of all, it might make sense to contribute the extra 8% but I would only do that in the context of my next point, which is to “optimize” your RRSP within your marginal tax bracket. Take the free money with the match, yes, but the extra contribution is either warranted or not. If not, maybe TFSA makes more sense.

If it does make sense to contribute more to the RRSP, my point is that most people should do that in a personal RRSP that is not tied to the group plan. Remember the group plan often limits its members to a narrow menu of investment options, which most of the time will be higher fees than an ETF that you can buy on your own.

So, the idea is that you’ll take the free money and max out your employer matching plans, then possibly contribute more to your RRSP, but do that in a personal RRSP and invest in lower cost ETFs.

Is a market crash coming?

Next, we have Adam who is feeling nervous about a post-election market crash and wants to know what to do about it.

Hi Robb: I keep reading about the impending market downturn after the election glee is over.

That said, since my wonderful foray into VEQT (with your encouragement,) should I be taking steps to secure my portfolio by moving say half of VEQT to a more balanced fund? Will you be writing about this in the near future?

Hi Adam, you’ll find no shortage of opinions on when the market is going to crash (and how bad). Whether it’s the election, or aftermath, or the next big thing that people are nervous about there will always be a reason for panicky investors to sell.

Your investing strategy should not change based on market conditions.

Meaning, if you are investing for the long haul and are in an asset mix that you’re comfortable with, then stay the course and ignore punditry and short-term price fluctuations.

Moving half of your VEQT into VBAL just creates VGRO (an 80/20 portfolio). If an 80/20 portfolio allows you to more comfortably stay in your seat then that might be a prudent move.

Just know that if VGRO existed during the great financial crisis it would have fallen 33.89% from June 2007 to March 2009 (45 months). So it’s not like 80% stocks is substantially less risky than 100% stocks (which fell 42.06% during that same time period).

Finally, know that the US market is not THE entire global market. It’s why you’re invested in VEQT (14,000+ global stocks) and not VFV (500 US large cap stocks). You’re taking risk, but you’re diversifying that risk around the world.

Stocks will absolutely fall at some point. But they’ll also recover eventually and make new all-time highs. That’s the nature of investing.

Market timing is a great way to end up poorer and drive yourself mad.

Why don’t retirees spend their money?

Next we have Darlene, who wants to know why retirees are so reluctant to spend their money.

Hi Robb, you mention retirees don’t spend up to their capacity. What’s driving this reluctance to spend down to zero, and what are they holding on to the money for? And do they really need to spend to zero?

Hi Darlene, the reluctance to spend comes from a fear of running out of money, either from a bad market crash, higher than normal inflation, high expenses on healthcare as they age, or from a higher-than-normal life expectancy.

A good retirement plan can help alleviate those fears, showing a range of outcomes using conservative assumptions on spending, inflation, longevity, and rates of return.

I don’t think anyone should be planning to truly die with zero – you need a margin of safety – but in my experience most retirees are not spending nearly up to their capacity due to the above fears and concerns.

I like to give my retired clients a spending range. A comfortable spending floor (typically what they’re spending now) that they could easily stick to in good times or bad, and then a safe spending ceiling that they could spend up to if desired without worrying about running out of money.

Related: Putting together your retirement income puzzle pieces

That range might look like an annual spending floor of $60,000 after-taxes, and an annual safe spending ceiling of $72,000. In reality, the sweet spot might be somewhere in the middle at $66,000, giving them a bit more spending capacity to enjoy retirement without causing too much anxiety that they’re overspending.

From dividend stocks to index funds: When to pull the trigger?

Finally, here’s a question from Jean about switching from dividend stocks to index funds.

I’ve been a successful dividend investor for about 20 years now and have been thinking of switching to indexing for a while. One of the main reasons for me to switch is that I’m getting older and losing the patience to manage my portfolio. Also, my family is not into it at all, so teaching them indexing would be much easier.

I have a pretty good idea what my final indexing strategy will look like. Something like VEQT with sprinkles of VCE/VV. Quite basic and simple!

My dilemma now is how to accomplish the transition? When and how do I pull the trigger?

Setting a date and doing it all at once seems to be the play like you did. But then, how do my manage my holdings till then? I’ve always had a long term approach and managing till the switch would be a pretty short term thing, hence a great part of my dilemma.

Any thoughts on all of that?

Hi Jean, you’ve listed some pretty compelling reasons to make the switch to indexing. As fun and interesting as it can be to manage your own stock portfolio, in my experience the juice is just not worth the squeeze anymore now that you can buy a single global index fund for the low price of 0.20% and get market returns without any effort.

No need for sprinkles, either. VEQT (or XEQT) has everything you need. Don’t overthink it!

Jean, this is a bit like getting into a cold pool or lake. Best to just jump in at once rather than stress about it and inch your way in.

Think of your portfolio as if it’s in cash right now. Would you buy all of your individual stocks again, or would you just buy your index fund?

Because that’s the exact same thing as selling all of your stocks at once and then immediately buying your ETF. You’re out of the market for a hot minute, and right back in with a globally diversified fund (minus some transaction fees, depending on your brokerage platform).

Pick a day – why not Monday at noon? The market is open, you can sell all of your stocks, and immediately buy your ETF. Done. No need to manage anything in the short term.

This is not like timing the market or anything. If you’re going to do it, best to get it over with and do it right away.

My only caveat to all of that is if you have large unrealized capital gains in a taxable account. More careful consideration needs to be taken there, likely with a financial planner or tax professional. I’ve worked with clients to sell their taxable holdings over a period of 2-3 years to spread out the capital gains hit.

There are no tax implications at all for selling stocks inside your registered accounts (RRSP, TFSA, and LIRA).

Do you have a money-related question for me? Hit me up in the comments below or send me an email.