5 Ways To Avoid Monthly Bank Fees

I’ve banked with TD my whole life but while I consider myself to be a fairly loyal customer that doesn’t mean I’ll blindly accept blatant fee grabs without fighting back.

That’s exactly what happened two years ago when the big green bank announced changes to its chequing account fees and minimum balances. Their basic chequing account, which I used, charged $3.95 per month but waived the fee as long as you maintained a $1,500 balance. That was about to increase to $2,000 and I had enough.

I sent an email to an advisor at my local branch and said I’d like to close my account ahead of these changes and asked him about moving some of my automatic withdrawals to another bank.

He replied back right away with an offer too good to pass up:

“Hi Robb, I can help you with this. I would need a void cheque and some signatures, so we would need to book an appointment. If you are interested, though, I will change your chequing account to a student account. It’s a free basic account, includes 25 transactions and no minimum balance, and this way you won’t have the hassle of making a bunch of changes to any direct debits you have going out.”

Well, needless to say, I jumped at the offer and today continue to bank fee-free with TD. It’s a win for me, of course, but also for the bank as they get to keep all of my business that includes banking, a mortgage, line of credit, plus RRSP, TFSA, and RESP accounts.

A chequing account might be the linchpin that holds all of your banking needs in one place. Let that go, and it becomes easier to move other aspects of your banking as well.

So, how can you comfortably bank for free? Here are some options I recommend to avoid monthly bank fees:

Unlimited chequing account, high minimum balance

If you’re the type of person that uses a debit card for the majority of your purchases, has a lot of automatic bill payments, and requires a full-service bank for in-branch transactions then you’ll have to bite the bullet and opt for a full service chequing account.

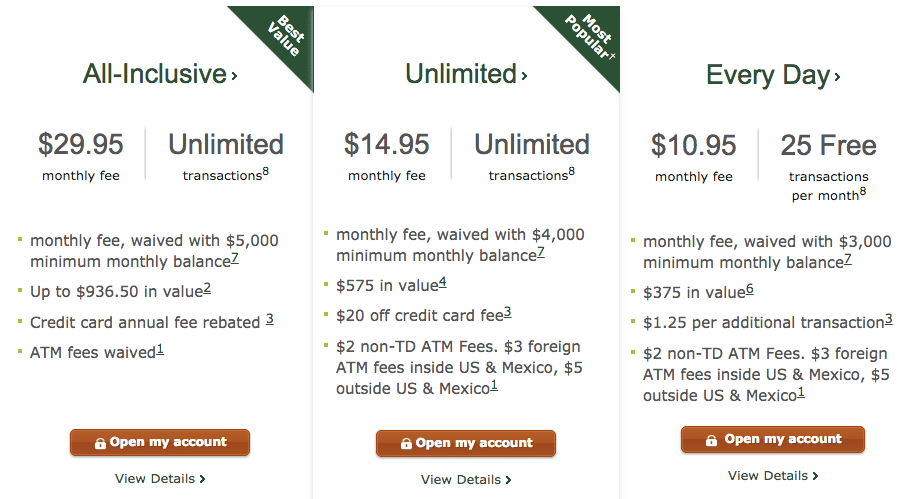

Unlimited transactions at most banks will cost about $14.95 per month and you’ll need a high minimum balance to waive the fees. You’ll have to decide if having $5,000 sitting around in a chequing account is worth it to get unlimited banking.

Basic chequing account, still a minimum balance

The big banks were volun-told by the federal government to offer low cost accounts to consumers for $4 per month. These accounts offer bare minimum services, 10-12 transactions per month, and some will waive the monthly fee provided you maintain a minimum balance.

Look for terms like ‘basic’ or ‘minimum’ accounts, as they’re not well advertised by the banks and in some cases buried well below other more profitable banking options online. Here’s what’s highlighted at the top of TD’s chequing account page:

And then waaaay down at the bottom of the page you’ll find some other options:

A minimum or basic account is not a bad choice for those who use cash or a credit card for the majority of their transactions but still require the use of a full-service branch from time-to-time.

Combo: No-fee online bank + Basic chequing account at big bank

This is the sweet spot for those that have broader banking needs but don’t want to pay monthly bank fees or maintain a high(er) minimum monthly balance.

Open a no-fee chequing account at an online bank such as Tangerine or PC Financial, or at a local credit union, and pair it with a basic chequing account at a big bank, while maintaining the minimum balance to waive any monthly fees.

With the free-banking combo you can use the free account for any transactions such as bill payments, debit purchases, email money transfers (free with Tangerine) and cheque payments (free with PC Financial). Then you still have access to a full-service branch to get a bank draft, cash a cheque without a long hold, and have a wider network of ATM’s from which to choose.

I did this for several years with a Tangerine chequing account alongside my basic TD account. I got fed up when the minimum balance kept increasing (from $1,000 to $1,500 to $2,000).

No-fee online bank or credit union

Let’s face it, technology has changed the way we bank and unless you have complicated banking needs most customers can pretty much get the same level of service from an online bank or credit union as they can at a full-service bank.

The biggest difference: no fees. I’ve received countless emails from readers who have banked at PC Financial for over a decade and rarely paid a fee or ran into an issue where the no-fee bank couldn’t meet their needs. Plus, PC Points!

Credit Unions are also becoming more competitive and offering low or no-fee accounts to attract your business.

Just ask

It’s an annual ritual for some Canadians to call up their telecom provider and negotiate a better deal on their cable, internet, or phone charges. We should be doing the same for our banking. You always see awesome deals and promotions to attract new customers. What about an incentive for their existing customers? Since the bank is not going to just freely offer everyone a better deal, it’s up to you to ask (or demand!) one.

Related: Want a better deal? Just ask.

Final thoughts

Banks continue to make it difficult for customers to avoid monthly bank fees by increasing the minimum balance required or eliminating that option altogether.

You might not luck into a free full service bank account like I did but you’ll increase your odds if you have a back-up plan. There’s no harm in opening a no-fee bank account online and trying it out for a few months. Then, if you like what you see, go to your main bank with offer in-hand and threaten to close your account.

Keep in mind that the only way this negotiating tactic will work is if you’re actually willing to walk away. For some, it’s too much hassle to change their banking, but if you’re serious about saving money on bank fees you need to have an exit plan.

Readers: How do you avoid monthly bank fees?

I tried what you did with RBC but no luck! I got the usual story about how I got so much more from RBC than I would if I went to a no-fee bank, but so far I have no regrets about moving!!!

I have that middle bank account,the $14.95 one. It used to be $4.95 for the exact same account before the TD/Canada Trust merge.

I look at that $4000 as an investment earning me $180 a year. Not that bad a return for zero risk.

It’s a bit convoluted but given my account needs are vast and varied, it’s helped me accept the fact that otherwise, I’m paying $15 a month.

I have an excellent full-service chequing account at RBC for 10.95 per month. Each month my fee is instantly rebated because I have multiple products with the bank. No minimum bank account balance is required.

As a senior I was encouraged to switch to a Plan 60 account at TD, so no monthly charges. Mind you, they neglected to tell me this (don’t banks record birth dates?) until I was 63 so I missed three years of free banking!

They definitely have your birth date as when my son turned 18 he was immediately notified that his ‘youth’ account would expire on the next billing cycle. However, when questioned at the same time why my father-in-law was not notified of the Seniors account as he was turning 65 on the same day. It was hard for them to say they didn’t have birth date information on that same call. They danced a lot about things but eventually admitted that banks are not in business to notify you of cost savings.

We have banked with PC Financial since it opened. We love the fact there are no charges for anything, including cheques, debit, etc

We keep our investments at Scotia since many ETFs are traded for no cost.

It is not difficult to switch from one bank or account to another. It is just an online thing now, very quick and very convenient.

I cannot see a reason for paying any bank charges now.

Hi Robb,

We all know that banks are in the business to make money for their shareholders.

They nickle and dime us ordinary ‘savers’ for anything to do with our accounts.

We do all our banking transactions online and the ATM ways but we still get charged with the service and maintenance fees on the transaction and our accounts right into our ‘senior’ years.

We got irritated at the ‘unexplained’ fees that kept appearing in our statement we decided to go in and talk to our branch manager for an explanation. She couldn’t find any good reason to give to us but through checking in into our banking records, she noticed that we had become ‘seniors’ and changed our accounts to the Senior Plan where there won’t be any maintenance fees charged on the accounts.

So, I agree with you that we should always ask them for these ‘special’ hidden deals.

We also have adopted the idea of ‘ Don’t get mad, get even ‘ at all these businesses that charge us fees for doing business with them by owning shares of the companies. That way we get back our money from the dividends they pay monthly or quarterly from becoming ‘part owners’ of the companies. Very satisfying indeed.

I bank at BMO with an unlimited account, and the world elite mastercard. The fee is waived for the mastercard as well as the account when you meet the 5k minimum.

That is not the case anymore. BMO charges you the annual fee on the World Elite Mastercard even if you have an unlimited account and maintain the minimum 5K balance.

CORRECTION:

1. Monthly minimum for the BMO Premium Plan is $6K as of December 1, 2016

2. BMO World Elite MasterCard is still free with the Premium Plan, but supplementary cards are now charged a $50 annual fee

3. Annual fee rebate no longer applies to BMO Cashback World or BMO AIR MILES World MasterCards

There are NO “no-fee” options at any of the Credit Unions, at least not where I live. All of them offer comparable checking accounts to the Banks, only waiving some of the fees if you maintain some outrageous minimum balance in your chequing account.

You’d think the financial institutions would be willing to offer better deals to people willing to move all of their investments, savings accounts, etc. along with the checking account. That isn’t happening, either.