You might not have a hot clue how much you plan to spend in retirement, especially if those days are still a decade or further away. Even those nearing retirement may not have a good sense of their desired retirement spending amount.

A good rule of thumb is that you’ll likely want to enjoy the same standard of living you enjoyed in your final working years, if not enhance it with extra money for travel, hobbies, helping your kids, and spoiling your grandkids (if possible).

When preparing retirement plans for clients I’ll look closely at their current spending, and then stress-test the heck out of their plan to determine their maximum annual spending (the most they can sustainably spend without running out of money by age 95).

This offers clients a spending range between a comfortable floor (what they’re spending today), and a safe ceiling (their maximum sustainable spending limit). For example, let’s assume you spend $84,000 after-taxes in your final working years. A thorough stress-test of your plan suggests you can spend up to $96,000 per year without running out of money by age 95.

Knowing this, clients have the option to dial up spending in good times or to dial it back in bad times. Reality probably means settling into the sweet spot of spending $90,000 per year.

Retirement spending of $84,000 likely gives you the ability to continue making TFSA contributions into retirement – socking away money for large known one-time expenses, unplanned future spending shocks, or to build up tax free savings for your estate. The trade-off is sacrificing some standard of living and not spending up to capacity.

Spending up to the $96,000 ceiling offers the ability to maximize life enjoyment, particularly in the “go-go” years of early retirement. The trade-off is no room for extra savings contributions to the TFSA for a rainy day, and potentially less margin of safety for unplanned spending, poor market returns, or longer than normal life expectancy.

One area of spending not talked about enough is your one-time cost categories like buying new vehicles, renovating or repairing your home, gifting money to your children, or taking a bucket list trip. These expenses are often large, are not factored into your annual spending needs, and tend to occur in the early years of retirement, squarely in what I call the retirement risk zone (the period of time between retirement and when pensions and government benefits kick-in).

Throw a bad stock market outcome into the mix, and this could be a recipe for disaster if not planned for appropriately.

All the more reason why retirement planning should be done 5-10 years before your retirement date. This gives you a chance to understand your retirement spending needs, list and prioritize your one-time expense categories, and hopefully knock some of those items off while you’re still working and earning income.

This also gives you a chance to consider working part-time as a way to combat the retirement risk zone and ease yourself into full-stop retirement living.

This Week’s Recap:

No posts from me in a while as much of our free time has been sucked up by kids’ activities (dance season) and birthdays.

From the archives: Forget about asset location – why you should hold the same asset mix across all accounts

One final note on our mortgage renewal with Pine Mortgage. Everything is in place now and we’ve received the $3,000 cash back promotion along with a reimbursement for the home appraisal that they ordered. The dashboard is nice and user friendly, and they allow payments from our regular TD chequing account.

Speaking of TD, they reimbursed us for the mortgage payment that automatically came out of our chequing account on May 1st.

Finally, it looks like Pine Mortgage will get more attention now that they’re been chosen as Wealthsimple’s mortgage partner. That’s right, Wealthsimple is now offering mortgages (through Pine) and has some great deals for Wealthsimple customers (existing and new).

Promo of the Week:

Want to earn some serious credit card rewards? Start with the Amex Cobalt card – the best card for everyday spending in Canada with 5x points for food & drink. Sign up and spend $750 per month on this card to get an extra 15,000 Membership Rewards points (plus the 45,000 points you’d earn if you spend $750 per month on a 5x spending category).

Then use your own referral link to refer your spouse or partner (called: activating Player 2), and have them do the same thing. This could be worth a total of 120,000 Membership Rewards points in a year, plus another 10,000 for the referral bonus.

Next, use this link to sign up for your own American Express Business Gold card and earn 75,000 Membership rewards points when you spend $5,000 within three months. Then activate your player two for a chance to earn another 90,000 points (15k referral plus 75k welcome bonus).

If you’re looking for hotel rewards, this one is an absolute no-brainer card to have in your wallet. The Marriott Bonvoy Card gives you 55,000 bonus (Bonvoy) points when you spend $3,000 within the first three months. Not only that, you get an annual free night certificate to stay at a Marriott hotel (easily worth $300+), making this a card a keeper from year-to-year. The annual fee is just $120.

Weekend Reading:

A question I’m hearing more and more from clients and readers alike: Is it wise to begin investing when stocks are at an all-time high?

A Wealth of Common Sense blogger Ben Carlson on the gambler’s fallacy in the stock market.

David Aston explains why, when it comes to Canadian government pensions (CPP and OAS), timing is everything.

Jason Heath shares why your retirement may be different than you expected:

“Retirement math, whether based on rules of thumb or professional planning, can overlook some of the real-life implications of being a retiree. Running out of money is a risk, but so is running out of time.”

You want to retire early. Should you start your RRIF withdrawals sooner or later?

Trading meme stocks is gambling, not investing. But, have you ever gambled with meme stocks? Preet Banerjee walks us through the latest drama with GameStop stock:

Work can maintain engagement, keep us all sharp, as well as continue social connections and even a sense of purpose. Here’s why we should douse the FIRE movement and adopt CHILL instead.

A good piece by Dana Ferris on how to determine the appropriate retirement date. I recently wrote something similar about the best time of year to retire.

Long-time renter and blogger at Of Dollars and Data Nick Maggiulli writes about the rise of the forever renter class:

“This is where many in the unwilling Forever Renter class find themselves. They have good jobs. They make good money. But interest rates are also the highest they have been in two decades. As a result, if they want to borrow money to buy a house, they will pay for it dearly.”

PWL Capital’s Ben Felix explains why there’s room for good financial planning – and for error – before the June 25 capital-gains tax change (G&M subscribers).

Ben and his Money Scope podcast co-host Mark Soth teamed up to explain what the proposed capital gains changes mean for business owners.

Jamie Golombek says be careful moving your TFSA — or the CRA might come knocking. That’s because you need to let the financial institutions handle the transfer rather than withdrawing money from one TFSA and depositing it into another.

A really important article by Anita Bruinsma on what kind of money messages you’re sending your kids.

Used cars versus new cars: which market is offering better deals, and how has the landscape changed after the pandemic-era disruptions to supply?

Travel and credit card expert Barry Choi says there’s a loyalty arms race on, but not being loyal might be a consumer’s best move.

Finally, speaking of credit cards and loyalty programs, here’s a deep dive into the anatomy of a credit card rewards program. Interesting stuff!

Have a great weekend, everyone!

Some readers were appalled to learn that my wife and I completely drained our TFSAs in 2022 to fund a larger down payment on our new house. Okay, maybe not appalled – but it did raise a few eyebrows.

Remember, inflation was running hot and interest rates started to rise in March of that year. While we didn’t know the extent of the eventual rate hikes, it was clear that our new mortgage interest rate would be substantially higher than our existing one.

Besides that, we didn’t want to sell our existing house until we took possession of our new home. That meant taking on new debt from both a home equity line of credit and a builder mortgage (used to fund the new house construction at specific stages of completion). Both of these loans were floating at Prime rate – which eventually ended up at 7.2%.

Not relishing the prospect of carrying a larger mortgage balance at an ever increasing interest rate, we made the decision to tap into our TFSAs to the tune of about $175,000. That helped fund the first two construction draws before we had to turn to our lines of credit.

We moved into the house in April 2023, sold our previous house in May, and held back about $50,000 from the sale to pay for landscaping, window coverings, and some furniture.

Fast forward to 2024 and my wife and I are still sitting here with empty TFSAs. Well, until now.

On Friday we each made a $9,000 contribution to our TFSAs, with a goal of each contributing a total of $28,000 in 2024.

Here’s my TFSA catch-up plan:

- 2024 – $28,000

- 2025 – $28,000

- 2026 – $28,000

- 2027 – $40,000

- 2028 – $35,000

That will get me fully caught up on unused room, plus the new annual room accrued each of those years. From 2029 onward I’ll only need to make the annual maximum contribution to my TFSA.

My wife has less overall contribution room, so she’ll need to contribute $28,000 per year from 2024 to 2027, and then contribute $13,000 in 2028 to fully catch up on her TFSA contribution limit.

How are we contributing at such a high rate for the next five years? Part of it comes from one-time expenses we incurred in 2022 and 2023 that can now be redirected towards savings.

But we also made a conscious decision to pay ourselves more from our business so we can fund the extra TFSA contributions. The trade-off is that we’re investing fewer dollars inside the corporation.

It’s a delicate balance to pay yourself enough to fund your personal spending and savings goals, while retaining earnings inside the corporation to invest and grow at a lower tax rate (hopefully to fund future consumption).

The upcoming changes to the capital gains inclusion rate inside of corporations was also a key consideration.

We’ve already triggered a capital gain inside of our corporate investing account of about $70,000, which, after some nifty accounting, we’ll be able to withdraw $35,000 tax-free as a capital dividend.

Finally, it just made good sense to pay a bit more tax upfront over the next five years to fill up our TFSAs quickly and get those funds invested and growing tax-free for the long haul.

So, fear not, dear readers. Our TFSAs will be maxed out again soon. Hopefully we can stay away from any new show homes for while and they’ll stay that way 🙂

This Week’s Recap:

In last week’s edition I celebrated our investments surpassing the $1M mark for the first time. I’m really excited to add our TFSAs back to the mix of accounts and really give us a diversified set of options to draw from in retirement.

From the archives: A look at closet indexing – the dirty little secret of the mutual fund industry.

A final update on our mortgage switch from TD to Pine Mortgage. Pine came through and got the mortgage switched before the end of the month, and I can’t say enough good things about working with them so far. Your mileage may vary, of course, but they got the job done.

TD, on the other hand, discharged the mortgage on April 30th and then still took our monthly payment out on May 1st. Not cool!

Promo of the Week:

Want to earn some serious credit card rewards? Start with the Amex Cobalt card – the best card for everyday spending in Canada with 5x points for food & drink. Sign up and spend $750 per month on this card to get an extra 15,000 Membership Rewards points (plus the 45,000 points you’d earn if you spend $750 per month on a 5x spending category).

Then use your own referral link to refer your spouse or partner (called: activating Player 2), and have them do the same thing. This could be worth a total of 120,000 Membership Rewards points in a year, plus another 10,000 for the referral bonus.

Next, use this link to sign up for your own American Express Business Gold card and earn 75,000 Membership rewards points when you spend $5,000 within three months. Then activate your player two for a chance to earn another 90,000 points (15k referral plus 75k welcome bonus).

If you’re looking for hotel rewards, this one is an absolute no-brainer card to have in your wallet. The Marriott Bonvoy Card gives you 55,000 bonus (Bonvoy) points when you spend $3,000 within the first three months. Not only that, you get an annual free night certificate to stay at a category five hotel (easily worth $300+), making this a card a keeper from year-to-year. The annual fee is just $120.

Weekend Reading:

Of Dollars and Data blogger Nick Maggiulli explores why people make “bad” financial decisions.

A nice piece on the rise of zero-based budgeting, a system in which you assign a job to every dollar of gross income.

Author Morgan Housel smartly explains how to think about debt:

“Once you view debt as narrowing what you can endure in a volatile world, you start to see it as a constraint on the asset that matters most: having options and flexibility.”

Should you max out your RRSP before converting it to a RRIF? Jason Heath explains what to consider before making this pivotal conversion.

Mark Walhout highlights the risks of adding your children to your accounts:

On a similar note, estate & trust professional Debbie Stanley answers an often asked question – can transferring ownership of a house help avoid probate tax?

Rounding out the estate planning trifecta, here’s Aaron Hector on whether you are tax planning for you, or your estate:

“In a nutshell, every dollar of income that you accelerate is a dollar of income that you don’t have to report in the future, and you get to choose what tax rates get applied to that dollar; the current marginal rate, or the future marginal rate (which could be higher). It’s easy to see how this process can result in your paying a lower average lifetime tax rate.”

Ontario’s Sunshine List discloses the salaries of government employees making more than $100,000, but hasn’t been adjusted for inflation since debuting in 1996. Preet Banerjee says the directory, which now has more than 300,000 names on it, is mostly a list of people who can’t afford to buy a home in Ontario.

Finally, Jason Heath answers the following question – Do all the advice articles about waiting to take CPP at age 70 take into account the calculation of your eligible amount if you stop working and contributing at, say 60 years old, and therefore have 10 years of no contributions?

Enjoy the rest of your weekend, everyone!

When should you take your Canada Pension Plan (CPP) benefits? Like many personal finance decisions, the answer depends on your unique circumstances. In general, it makes sense to defer taking CPP until age 70. The caveat is that you need to have other resources to draw from while you wait for your CPP benefits to kick-in. After all, who wants to delay spending in their “go-go” retirement years just to shore up their income in their 70s and beyond?

I’ve written before about when it makes sense to take CPP at age 60, why taking CPP at age 65 is never the optimal decision, and why taking CPP at age 70 can lead to $100,000 or more lifetime income.

But one question I often receive from readers and clients is when should early retirees take CPP? Here’s a reader named Keith, who decided to retire at the end of last year at age 60:

“My understanding is that since I won’t earn any income from now to 65, those five years will add to the CPP average calculation and potentially lower my eligible monthly amounts. If that’s the case, should I apply for CPP right away, or choose to defer it to 65 or 70? If I apply today, will those five years of zero income still be included in the average CPP calculation?”

It’s a great question. CPP is a contributory program based on how much you contributed (relative to the yearly maximum pensionable earnings) and how many years you contributed between ages 18 to 65.

To receive the maximum CPP benefit at age 65 you would need 39 years of maximum contributions. You can drop-out your eight lowest years (more if you are eligible for the child rearing drop-out provision) from the calculation.

Related: How Much Will You Get From Canada Pension Plan?

You can see the problem for early retirees. They’re going to have more “zero” contribution years which will reduce the amount of their CPP benefits.

Not so fast.

You will always get more CPP by waiting, even if you’re not working.

CPP expert Doug Runchey says that your “calculated (age-65) retirement pension” may decrease if you’re not working between age 60 and 65, but the age-adjustment factor will always make up for that decrease, and then some.

“In that situation I use the expression that you will receive a larger piece of a smaller pie if you wait, but you will always get more pie,” he said.

CPP checklist for early retirees

Here’s what to do if you’re in the early retirement camp and want to know when to take your CPP benefits. Log into your My Service Canada Account online and click on “Canada Pension Plan / Old Age Security.”

Scroll down to the “contributions” section and click on “Estimated Monthly CPP Benefits.”

You’ll see your expected CPP benefits at age 60, age 65, and age 70.

Now take that calculation and throw it in the garbage because it’s completely useless. That’s right. The CPP estimates you see here assume that you continue contributing at the same rate until age 65. That’s problematic if you plan to retire at age 58 or 60 and will no longer be contributing to CPP.

Go back to the previous screen and click on your CPP contributions. There you will find a web version* of your Statement of Contributions – a history of your contributions dating back to age 18. Right click on this page and “save as” (format: webpage, HTML only).

*Note you can request a copy of your Statement of Contributions in the mail, but you won’t need that for the next step.

Now visit www.cppcalculator.com and sign up for the website with your first name and email address. You’ll receive a confirmation email from the site founder David Field (co-created by Doug Runchey) to activate your account, followed by another email to login to the site and run your own unique CPP calculation.

Upload the statement of contributions that you saved earlier (or manually enter your pensionable earnings year-by-year). The beauty of the CPP Calculator website is that it allows you to manually enter future years, including future “zero” years if you plan to retire early.

I ran this calculation for myself because, as of right now, I am paying myself dividends from our corporation and not making CPP contributions (it’s a decision I continue to wrestle with, as I’d have to switch from dividends to salary and then pay both the employer and employee portion of CPP each year).

The estimate I shared above from My Service Canada is my own estimate based on 15 years of max contributions, plus another eight years of lower than max contributions. I did not contribute to CPP in 2020 or 2021, but it looks like Service Canada assumes I will continue making contributions until age 65.

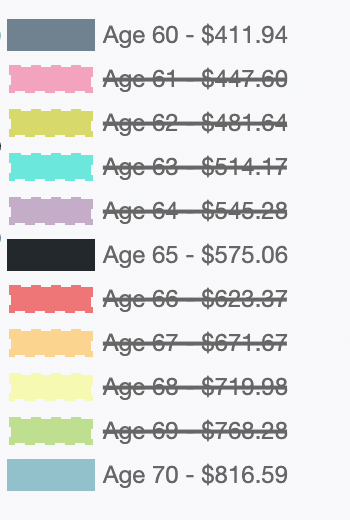

When I ran the numbers in CPP Calculator I assumed no more contributions to CPP from age 43 to 65. Look at the difference that makes for my CPP at ages 60, 65, and 70:

Instead of receiving $1,086.95 per month at age 65, I should only expect to receive $575.06 per month. That’s almost a 50% reduction in expected benefits. In other words, it’s a huge difference.

Final Thoughts

When should early retirees take CPP? There’s no definitive answer, but having the right data will help inform your decision.

The My Service Canada estimator assumes you work until 65. Use the CPP Calculator website and manually enter “zero” years if you plan to retire earlier than 65. That will give you a more accurate estimate of your CPP benefits.

Remember that you will always get more CPP by waiting, even if you retire early. Your calculated age-65 CPP benefit may decrease, but that will be more than offset by the age-adjustment factor or deferral credit (7.2% per year from 60 to 65, and 8.4% per year from 65 to 70).

Disclaimer: If at any time you stopped work to raise kids or recover from a disability, or you have been widowed, divorced or separated then the CPP Calculator will not provide you with an accurate calculation. It is recommended that you have your benefit amount manually calculated by Canada Pension Plan expert Doug Runchey, who charges a nominal fee but guarantees the accuracy of your estimate.