“When the facts change, I change my mind. What do you do, sir?” – John Maynard Keynes (maybe)

As a long-time mortgage holder, I’ve been adamant about a mortgage renewal strategy that goes something like this:

Go variable when the 5-year variable rate is offered at a steep discount off of prime rate (prime minus 1% or better), or else take a short-term fixed rate (1-2 year term) when the variable option is not attractive.

This approach meant holding a variable rate from 2011-2016, then taking a 2-year fixed rate from 2016-2018, and then back to variable from 2018-2023. This worked splendidly until about March 2022 when rates started to increase, and only really started getting hairy when the Bank of Canada hiked a full 1% in July 2022.

Nevertheless, we’ve done well with this approach – “winning” in 11 out of the last 12 years as far as I can tell.

We moved into our new house at this time last year and, amidst rising interest rates, elected to take a 1-year fixed rate mortgage term at 5.74%. This gave us a chance to hopefully see inflation come down in a meaningful way and open the door for the Bank of Canada to cut rates.

Turns out that was a bit premature, as rates aren’t expected to start falling until at least June or July. And, if inflation remains sticky in the high 2% / low 3% range, the Bank of Canada could certainly hold steady.

At the very least, BoC governor Tiff Macklem has already said that interest rates won’t decrease nearly at the same speed that they increased during the height of inflation.

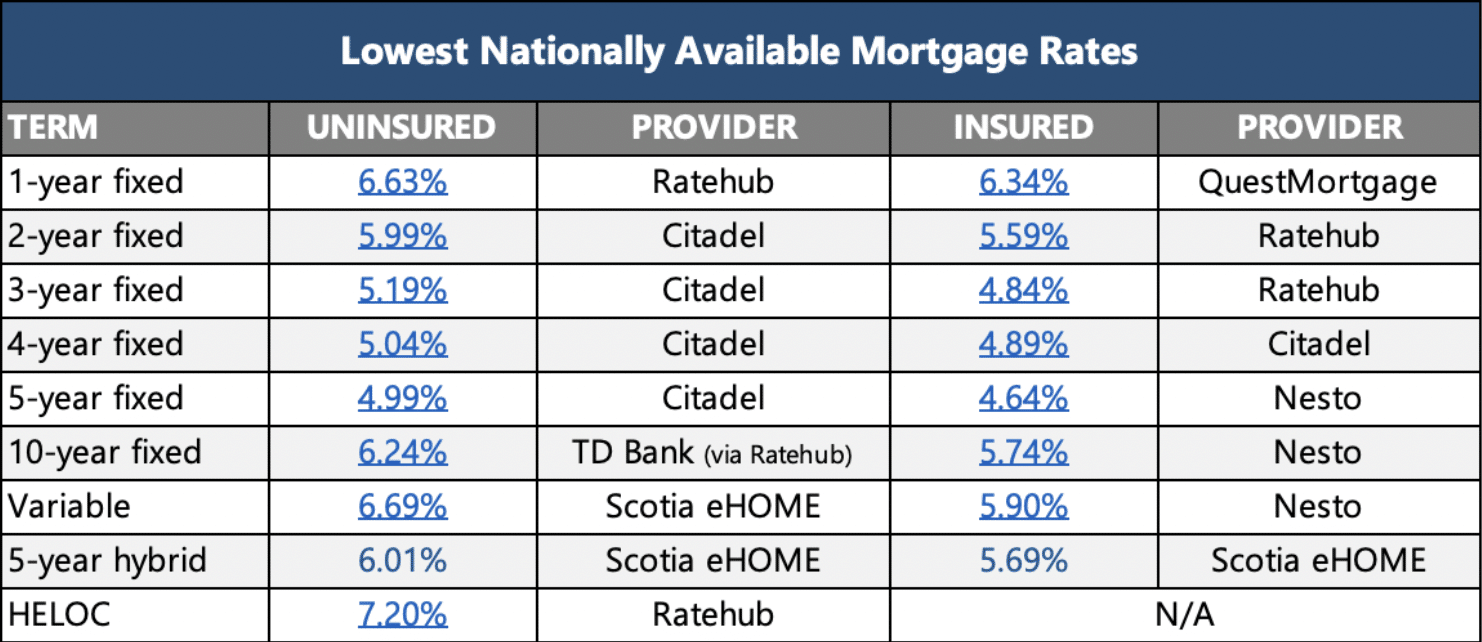

That’s enough to give this personal finance blogger pause when it comes to betting on variable rates to win this term. Besides, the best variable rates on uninsured mortgages are pretty, pretty bad right now.

Rates would have to fall fast and hard for a variable term to outperform.

The trouble is, short-term (1-2 year) fixed rates aren’t much better.

That’s why I’m holding my nose this time and going with a 3-year fixed rate term. It’s the Goldilocks term – not too long in case rates do fall in a meaningful way, and not too short that we don’t get any meaningful rate relief now.

I found out through the grapevine that one of the big 5 banks is offering 3-year fixed rates at 4.99% so I’ve made that known to our mortgage lender and they’ve reached out to the powers that be to see if they can make it happen.

An interest rate of 4.99% is 0.75% better than our current rate. We’ll keep our payments the same, so we can make a bigger dent into the principal balance over the next three years.

This Week’s Recap:

In last week’s edition of Weekend Reading I shared some tips for investing in an asset allocation ETF.

From the archives: Why it would be ludicrous to invest in these model portfolios.

And for those of you filing taxes this month, here’s the difference between tax deductions and tax credits.

Promo of the Week:

We activated player two for our rewards cards strategy, meaning earlier this year I signed up for the American Express Business Gold card, hit the minimum spend target to reach the welcome bonus, and then referred my wife (player two) to get the same card in her name.

The result is 15,000 additional Membership Rewards points for me for the referral, and now my wife has a chance to earn 75,000 Membership Rewards points after spending $5,000 in the first three months.

Use this link to sign up for your own American Express Business Gold card and earn 75,000 Membership rewards points when you do the same. Then activate your player two for a chance to earn another 90,000 points (15k referral plus 75k welcome bonus).

If you’re looking for hotel rewards, this one is an absolute no-brainer card to have in your wallet. The Marriott Bonvoy Card gives you 55,000 bonus (Bonvoy) points when you spend $3,000 within the first three months. Not only that, you get an annual free night certificate to stay at a category five hotel (easily worth $300+), making this a card a keeper from year-to-year. The annual fee is just $120.

We used our free night to stay in the Calgary Marriott Airport in-terminal hotel the night prior to an early flight departure. Nothing beats walking out of the hotel lobby and right to your gate without stepping foot outside! We’ll do it again in London later this year before flying home from Heathrow in October.

Again, refer your spouse or partner and do it all over again to earn another 55,000 Bonvoy points, plus 20,000 referral points, and another free night certificate.

Weekend Reading:

Why Andrew Hallam doesn’t regret selling his Berkshire Hathaway shares, even though they’d be worth almost $2M today.

Of Dollars and Data blogger Nick Maggiulli explains why someone’s current financial standing or background should hold much weight when determining whether their advice is useful:

“Just because someone is rich doesn’t imply that they know how they got rich. The same goes for someone who was “poor” and then became rich. After all, you could’ve gotten rich in a different way than what you claim publicly.”

You should subscribe to the FP Collective, a new website aimed at helping Canadians cut through the noise and find trustworthy financial information. The first post by Cameron Smith debunks investment myths to explain what you really need to know about expected returns.

Here’s PWL Capital’s Ben Felix on why bank financial advice is worse than people realize:

Morningstar’s Christine Benz shares why index funds and ETFs are good for retirees due to low costs, tax efficiency, ease of oversight, and cash flow extraction.

Another FP Collective banger, this time it’s advice-only planner Julia Chung explaining what to think about when it comes to passing down the family cottage:

“You may find that there are just a few people who really want to keep the property. Or perhaps there are none and it’s time for you to sell. Or perhaps everyone wants in. If more than one person definitely wants to maintain the property, then you know it’s time for a family meeting.”

Recent retiree Jeffrey Actor and his wife were shy to admit that their international travel bucket was relatively empty, and they had embarrassingly few stories to share. The question they asked themselves was – if not now, when?

People like to complain about CPP, but it is one of the most valuable retirement assets available to Canadians:

Morningstar’s latest study on balanced funds shows that Canadian investors have been steadily selling commission-based funds for balanced ETF versions. Well done!

Finally, The Loonie Doctor Mark Soth says that investors are prone to fear, overconfidence, and other forms of expensive self-talk.

Have a great weekend, everyone!

Asset allocation ETFs revolutionized investing for do-it-yourself investors when they were first introduced by Vanguard in 2018.

Prior to the existence of these multi-asset ETFs, passive investors might have opted to follow one of the Canadian Couch Potato’s model portfolios to build their own multi-ETF portfolio (remember the 10-ETF Über-Tuber portfolio?).

That’s why I say asset allocation ETFs have been such a game changer for self-directed indexers. I take it a step further and say investing complexity has largely been solved with these all-in-one funds.

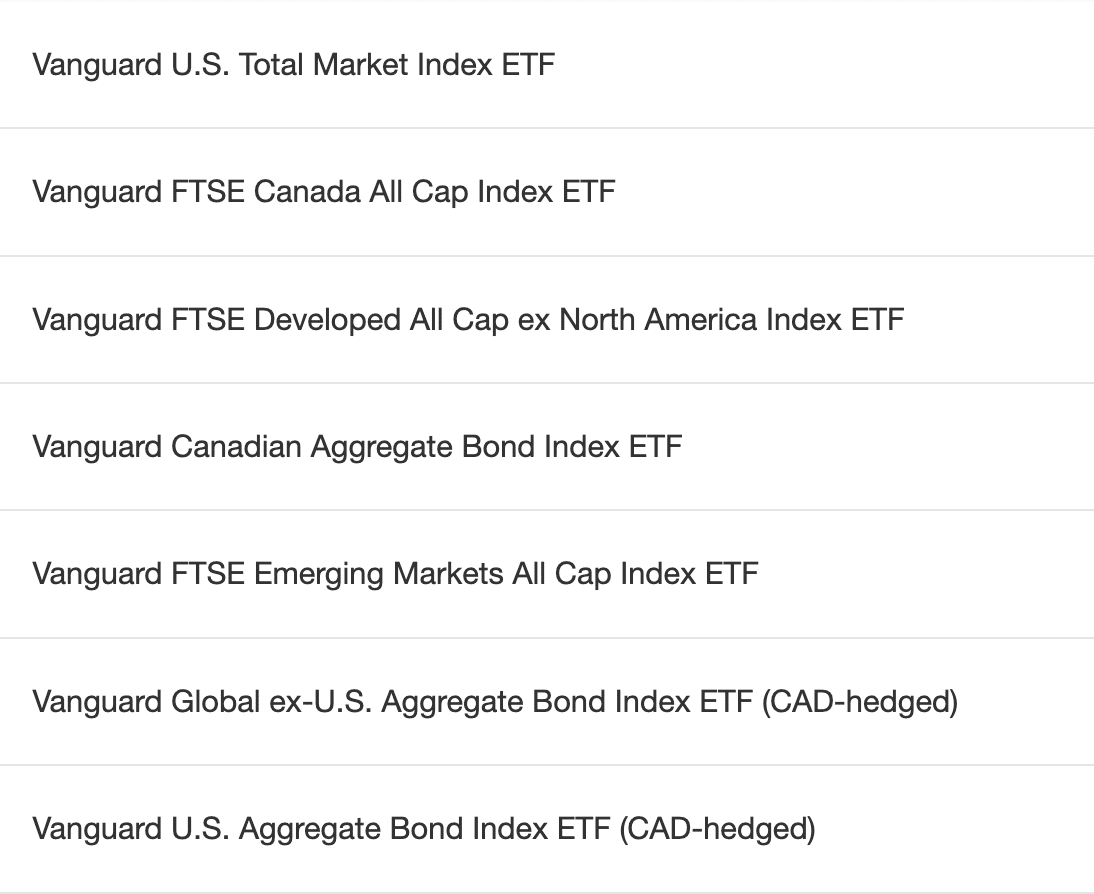

Many investors agree, as Vanguard’s Growth ETF (VGRO) has taken in $4.84B in assets in six years, while Vanguard’s All Equity ETF (VEQT) has gathered $3.69B in assets in five years of existence. I invest my own money in a single asset allocation ETF in each of my account types.

Despite their growing popularity, myths and misconceptions about asset allocation ETFs frustratingly still persist today.

Just one fund?

The most common push back against moving to an asset allocation ETF is that investors think they’re putting all of their eggs in one basket. But this is just an illusion. Asset allocation ETFs are simply a fund-of-funds that contain 4-8 underlying ETFs.

Like the old Couch Potato model portfolios, these individual ETFs have just been neatly packaged up into a single, automatically rebalancing product.

It’s also a pretty darn big basket. For instance, VGRO contains more than 13,500 global stocks and 19,000 global bonds.

Finally, holding a single globally diversified ETF is no different than how many Canadians currently invest at their bank branch. Consider most cookie-cutter bank portfolios (like the RBC Select Growth portfolio (RBF459) are also invested in just a single globally diversified mutual fund.

The big differentiator is that VGRO comes with a total MER of just 0.24% while the RBC Select Growth portfolio charges an almost criminal 2.04% MER (but at least you get a phone call once a year at RRSP season – maybe).

Really, just one?

Okay, so you’ve been convinced that holding an asset allocation ETF is a good idea, but which one?

Vanguard, iShares, BMO, Horizons, TD, Mackenzie, and Fidelity all offer a suite of asset allocation ETFs. And, the suites contain everything from 100% global equities to a conservative 20% equity / 80% bond mix. Shouldn’t you hold a few to spread your risk around?

Umm, no. These products are truly designed to be a one-ticket solution for your portfolio. Pick one that best represents your risk tolerance and time horizon and move on with your life.

Need help deciding? Watch this:

Here are two scenarios in which I’ll concede that holding multiple asset allocation ETFs makes good sense:

- Hedging your bets: Can’t decide between VGRO and XGRO? Hold one in your RRSP and the other in your TFSA (assuming you have the same risk profile in both account types). Or, as a couple, one spouse picks the Vanguard fund and the other spouse picks the iShares fund.

- Odds or evens?: Asset allocation ETFs are typically offered in increments of 20%. Meaning, if you are an oddball with a target mix of 90/10, 70/30, or 50/50 you’ll be hard pressed to find a one-fund solution. In this case, split your portfolio evenly between a 100/0 and 80/20 fund to create your desired 90/10 mix. Or hold the 80/20 fund and 60/40 fund to create your 70/30 allocation.

Double-dipping on fees?

Asset allocation ETFs bundle 4-8 individual ETFs into one easy to manage solution and typically charge a fee of between 0.20% to 0.25%. But one common concern for individual investors is whether they’d also be charged the MER on each of the underlying ETFs – essentially double-dipping on the fees.

Let’s put that myth to rest right now. What you see is all there is when it comes to the MER associated with an asset allocation ETF. There are no hidden fees or double-dip charges for the underlying funds.

While you could technically hold the underlying funds yourself at a slightly cheaper cost, you could also pay a slightly higher convenience fee to have those ETFs bundled into one self-rebalancing product.

Ask yourself whether the juice is worth the squeeze when it comes to adding complexity to your portfolio just to save a few basis points of cost.

This Week’s Recap:

Revisit my last weekend reading where I asked where are my customers’ yachts?

From the archives: Here’s how early retirees can more accurately estimate their CPP benefits.

RIP to behavioural psychologist legend Daniel Kahneman, who passed away earlier this week at the age of 90:

I emailed Daniel Kahneman several years ago asking about peculiar behaviour I noticed amongst credit card users. To my surprise he kindly replied right away with his classic line of “What You See is All There Is.”

RIP to an absolute legend https://t.co/gPifESvuMY

— Boomer and Echo (@BoomerandEcho) March 27, 2024

Promo of the Week:

Have you noticed that credit card companies have started to communicate with you about when your annual fee is due? I’ve received notifications from American Express and from CIBC in recent weeks, which makes me wonder if this is something that has been regulated or mandated (anybody know?).

I’m all for it, since I often forget to call and cancel a card ahead of the annual fee being charged.

Speaking of credit cards, I’ll continue to beat the drum about the American Express Cobalt – the best card for everyday spending in Canada with 5x points for food & drink. Sign up and spend $750 per month on this card to get an extra 15,000 Membership Rewards points (plus the 45,000 points you’d earn if you spend $750 per month on a 5x spending category).

Then use your own referral link to refer your spouse or partner (called: activating Player 2), and have them do the same thing. This could be worth a total of 120,000 Membership Rewards points in a year, plus another 10,000 for the referral bonus.

Also, for business owners and side hustlers, the best sign-up bonus in Canada right now is for the American Express Business Gold Card, where you’ll get 75,000 Membership Rewards points when you spend $5,000 within the first 3 months. The annual fee is just $199, which is reasonable for a business card.

Weekend Reading:

How to cope with the RRSP-to-RRIF deadline in your early 70s.

Picking a financial advisor? There are red flags you should know about.

Preet Banerjee on why those most likely to benefit from a budget are least likely to have one.

Sometimes we do stupid shit, and everything works out. On most occasions, it doesn’t.

Ben Felix explains why it’s dangerous to assume that stocks will return 10-12% per year.

More on that assumption here:

Morningstar’s Christine Benz on how to declutter your investor portfolio.

Tales of charlatans and chagrin from the Loonie Doctor blog:

“Before you scoff and claim that it would never be you, know that these stories take in people from all walks of life. Less financially sophisticated people may not recognize the danger. Financially sophisticated people are juicy targets because they have money and are often looking for new ways to invest.”

A well-traveled crew of retirees share their savviest tips and tricks – from travel days to avoid, to must-pack items.

Investment advisor Markus Muhs shares how he invests his money and his own money story.

A cash wedge can make good sense for retired investors, at least from a psychological perspective. A Wealth of Common Sense blogger Ben Carlson looks at the 60/30/10 portfolio.

The wacky negative interest rate experiment never gained traction economically but went on for more than a decade anyway. What was gained? (sub may be required)

Mortgage expert Rob McLister explains why putting discretionary income towards a mortgage is often not the winning play.

Finally, a must-listen podcast on overcoming frugality in retirement and why it takes a bit of a leap of faith to learn to let go and spend your money.

Have a great weekend, everyone!

Author Fred Schwed gave us his cynical take-down of Wall Street back in 1940 with the hilariously written, Where Are the Customers’ Yachts?. The book amazingly still holds up today in a world where investment advisors get rich while their customers, well, not so much.

“The title refers to a story about a visitor to New York who admired the yachts of the bankers and brokers. Naively, he asked where all the customers’ yachts were? Of course, none of the customers could afford yachts, even though they dutifully followed the advice of their bankers and brokers.”

I’m an advice-only financial planner who doesn’t manage money or get paid to tell you what to invest in. My goal is to help you navigate the financial minefield and use your resources over time to maximize your life enjoyment.

While my customers may not own any yachts (hey, neither do I!), I do get immense satisfaction helping clients achieve their rich life goals. One client suggested I start collecting postcards from my retired clients’ bucket list trips. Great idea!

It’s true that many retirees have a difficult time spending. I’d argue that the vast majority of my retired clients are capable of spending much more than they are right now.

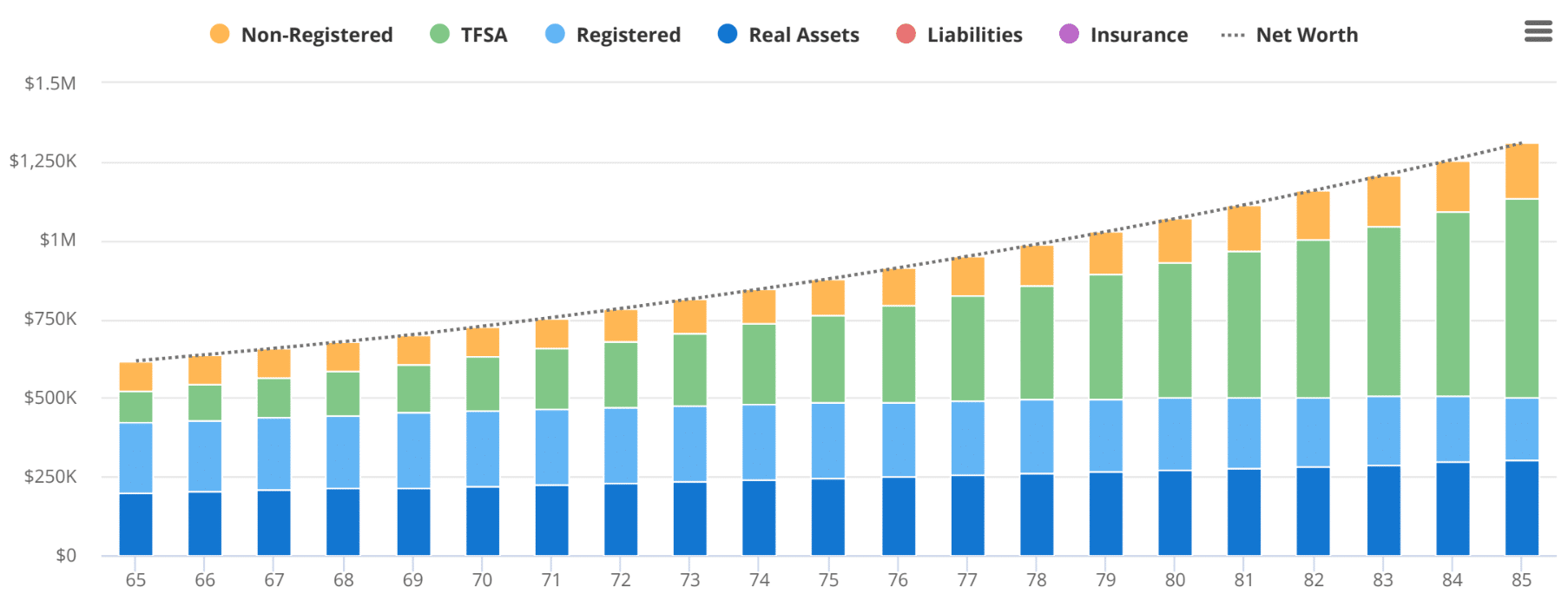

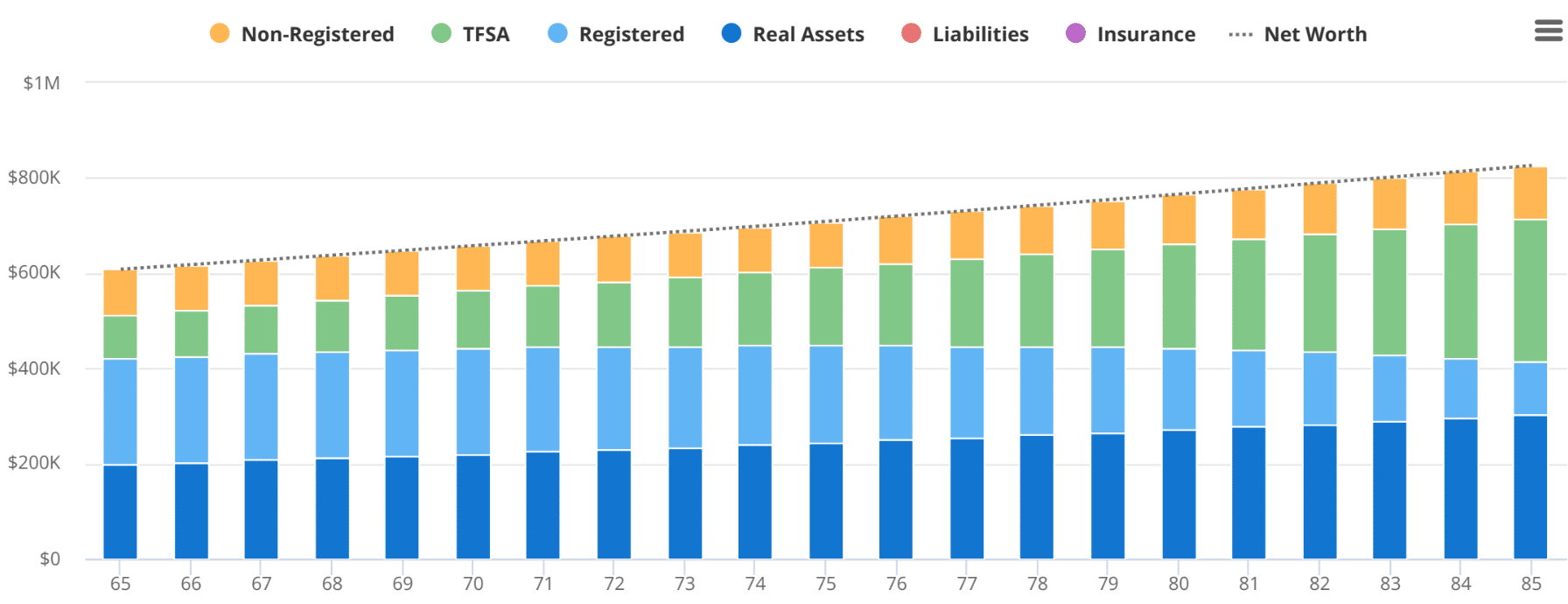

For instance, if your net worth is projected to increase every single year throughout retirement, that’s a pretty good clue that you can spend more money.

Occasionally I have a breakthrough and can convince a retiree to open up the spending taps a bit. This might be a bucket list trip, a home renovation, a new car, or an early financial gift to their kids or grandkids. I love it!

In the above example, let’s assume the client planned to spend about $38,000 per year after-taxes. Financial projections suggest they can spend up to $58,000 per year without running out of money (and without touching their home equity).

The client has an epiphany. Why live a smaller life than I need to in retirement, only to leave more than $1.3M in my estate for two children who are already established in their careers and have encouraged me to spend my money?

Don’t get me wrong – they don’t suddenly become a spendthrift after decades of frugal living. But they decide it’s not necessary to contribute to their TFSAs annually throughout retirement “just because” and so they re-direct that $7,000 contribution back into their annual spending amount – increasing from $38,000 to $45,000.

This amount is still well below their maximum sustainable spending number, but gives them more breathing room for travel (an annual cruise, perhaps?) and to hire a personal trainer.

They’re also still not touching the $100,000 they currently have invested in their TFSA. That amount will grow to nearly $300,000 by age 85, leaving a healthy and tax-free margin of safety for unplanned spending shocks.

This new spending plan also reduces their total savings and investments to about $500,000 at age 85 (versus $1M in the previous scenario). Still a very comfortable nest egg to fall back on if needed.

It’s a modest example, but these are my customers’ yachts. A realization that you have the ability to live the retirement of your dreams without worrying about running out of money.

This may allow you to snowbird in the US or Mexico for four months of the year, or buy a property in Florida to golf year-round and escape winter. You could take a bucket list trip to see the World Juniors in Sweden, or take that African safari adventure, or climb Machu Picchu in Peru.

Your “yacht” might literally be to buy a boat and sail around the world for a year, or buy a motorhome and visit all of the national parks in North America.

Perhaps your dreams are more philanthropic and you want to give money away to your kids, or to set up an endowment with your favourite charity. Maybe you just want to fund your grandkids’ RESPs, or take the entire family on a hot holiday once a year.

Whatever your version of a yacht is, don’t forget to send me a postcard!

Weekend Reading:

I recently moved my LIRA from TD Direct to Wealthsimple Trade and updated my post on how I invest my own money.

My “controversial” takes on bitcoin, CPP, and dividends from the last Weekend Reading update.

Finally, my latest post for MoneySense shows you how to start saving for retirement at age 45.

Promo of the Week:

Speaking of Wealthsimple Trade, the commission-free self-directed trading platform has slowly started adding more account types such as RRIFs, LIRAs, and LIFs. Supposedly RESPs and RDSPs are on the way soon.

As Wealthsimple Trade continues to add new account types, and several big bank brokerages (BMO, Scotia) offer commission-free ETF trades, I’m struggling to see how Questrade makes any sense for DIY investors

— Boomer and Echo (@BoomerandEcho) March 9, 2024

For simple index investors following my one-fund solution using a risk appropriate asset allocation ETF, Wealthsimple Trade is looking better and better.

Get $25 when you fund any Wealthsimple account with my referral code: FWWPDW

Plus you’ll get your reward boosted to $250 if you become a Premium client ($100k) within 30 days and $1,000 if you reach Generation status ($500k).

https://www.wealthsimple.com/invite

Weekend Reading:

New on CBC Marketplace this week, hidden cameras capture bank employees misleading customers and pushing products that help sales targets.

Something I’m keenly watching as my mortgage term expires next month. Variable or short-term fixed mortgage? Where experts see the ‘sweet spot’.

Mortgage broker David Larock says the longer the Bank of Canada takes to cut rates, the lower our variable rate mortgages will go.

Pay off your mortgage early or invest? Morningstar’s Christine Benz takes on this age-old question.

Of Dollars and Data blogger Nick Maggiulli has a clever take on bitcoin as a momentum trade – more people buy, number go up.

Michael Batnick with some smart thoughts on the fear of missing out:

“I have no problem with speculative behavior, but like walking into a casino, you have to know your limits, set them, and then don’t go back to the ATM once you hit that number. Have fun, but be careful out there.”

A Life Income Fund (LIF) is the annoying cousin of the Retirement Income Fund (RRIF), with both minimum AND maximum required withdrawal limits. Adam Chapman shares a neat trick to completely unlock your LIF in just a short period of time.

Speaking of RRIFs and LIFs, Jason Heath explains everything you need to know about these plans and their withdrawal rates.

Here’s a really good piece by Jason Evans about the pros and cons of buying back pensionable service.

A Wealth of Common Sense blogger Ben Carlson shares 20 lessons from 20 years of managing money.

Finally, retirement expert Fred Vettese explains how delaying retirement can boost income for singles (subs).

Have a great weekend, everyone!