The Super Bowl is the most-watched program on television each year and this year’s match-up between the New England Patriots and Seattle Seahawks will be no exception – as 113 million viewers are expected to tune-in to the big event.

I don’t have a horse in this race. My team, the dysfunctional Cleveland Browns, faded away in December and missed the playoffs for the 12th consecutive year (sad face). But that won’t stop me from spouting off predictions about the game and who I think will win Sunday.

The Patriots are favoured to win by 1 point, but so were the Denver Broncos and their record-setting offence last year before running into Seattle’s Legion of Boom defence en route to a 43-8 loss.

Prediction: New England will overcome the absurd ‘Deflategate‘ allegations that hogged headlines for the past two weeks and keep the game close for three quarters before Marshawn Lynch and the Seattle offence takes over in the fourth quarter to grind out a 28-20 win.

This week’s recap:

I was proud to be part of this event last night as the University of Lethbridge Pronghorns men’s hockey players shaved their heads in support of goalie Dylan Tait and trainer Brennan Mahon, who were diagnosed with testicular cancer earlier this season. Sportsnet turned up in Lethbridge to cover the post-game head shave, an event that raised close to $15,000.

Monday on the blog we had a guest post by Richard Garand of Master Your Portfolio. He explained the importance of international diversification.

On Wednesday, Marie looked at the problem with comparing your net worth to others.

On Friday, I explained why a core-and-explore investing approach is a bad idea.

Over on Rewards Cards Canada I looked at the best credit cards for travelling outside of Canada. Hint: It’s the ones that don’t charge a 2.5% fee for foreign currency conversion.

Weekend Reading:

My switch from dividend stocks to a two-fund ETF solution has generated some buzz in the media. Jonathan Chevreau of MoneySense and the Findependence Hub wrote about two other Canadians who’ve made similar changes to their portfolios.

A fascinating read about two Capital One fraud researchers who used massive amounts of credit card transaction data to make $278,000 trading options on shares of Chipotle, Coach, and Cabela’s after determining whether revenues were increasing or declining.

I’m not sure that the Bank of Canada’s 0.25 percent rate cut was intended to shore up bank profits, but Canada’s big 5 banks finally caved to pressure and (partially) lowered prime rate by 0.15 percent.

A pair of surveys shows a wide gap between what the public thinks and what scientists know about everything from genetically modified food, climate change, vaccinations, and evolution.

Sandi Martin addresses the problem with financial facelifts and soundbite financial advice.

Ben Carlson lists several questions that most investors don’t ask.

Jonathan Chevreau explains how low interest rates have changed retirement planning.

Michael James was a stock-picker for 12 years before making the switch to index investing. He’s come up with a tongue-in-cheek check-list for investors who still want to feel good about picking stocks.

Dan Wesley does a nice job explaining one of the more complicated financial decisions – a pension buy-back.

Mark Seed put a lot of thought into listing his income sources, needs, and wants in retirement.

Million Dollar Journey continues its net worth series – this one profiling a 30-year-old Calgary engineer just getting started with a negative net worth.

Alan Whitton wrote about a new website designed to help lower-income families open RESPs and access the Canadian Learning Bond.

Retirees shared their biggest financial surprises in this piece from the Financial Post.

Finally, for the hotel and travel enthusiasts, Marriott International acquired Delta Hotels and Resorts from my former employer, bcIMC, for $168 million.

Have a great weekend and enjoy the Super Bowl, everyone!

Do you ever wonder what others are doing with their finances and where they stand? My usual, rather pessimistic, thought is that I’m not doing nearly as well as my peers.

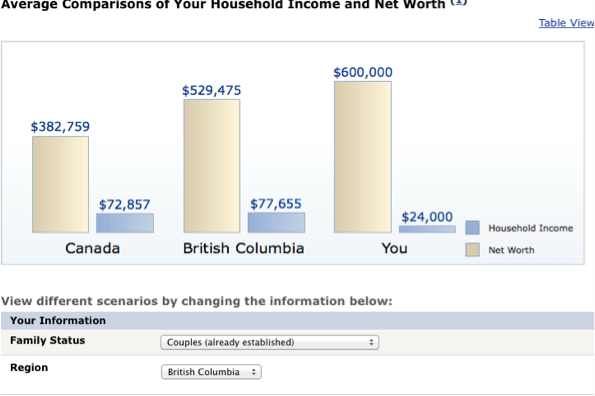

I came across this calculator on CNN Money that gave a median net worth comparison for income and age. My income is pretty low at $24,000 and I entered this amount and my age – 60 and this was the result.

My net worth is in the $700,000 range, but before I start congratulating myself I realize that this compares the net worth of US residents. Canadians must be better savers. After all, I always read about Boomers with $5-million residences and portfolios in the seven figures, so now I feel I’m falling extremely short.

Related: Fun with calculators (and other online financial resources)

I found another net worth comparison calculator from the Royal Bank that give me this result:

So What?

We all like to compare ourselves to what others are doing, especially in financial matters, where our conversations are vague and we always want to sound smart and on top of our money.

We’re curious about what the benchmark – or median – is. But, really, these types of calculators and comparisons are useless because there is no other context. Everyone is different and has different circumstances.

Related: Why age-based savings benchmarks are dumb, but we look anyway

Assets only have the value that you give to them. Some people might be thrilled to have the above-mentioned $180,000. Then there are others that worry themselves sick because they don’t think several million dollars is enough.

Final thoughts

Having a comfortable life has less to do with how much wealth you have stored up and more to do with your state of mind. How much do you need to maintain a comfortable lifestyle? The “magic number” is going to be different for everyone depending on chosen lifestyle, spending, and priorities.

You only get meaningful data by calculating your own net worth at least annually, and comparing the results with your previous information. Your annual review can help you measure the progress of your financial plan. It helps to keep you on track and stay focused on achieving your own vision. You then have a choice of whether you’re willing to make any necessary changes.

What do you think of these net worth comparison calculators?

Many people are saying that since all stock markets went down in 2007 – 2009, international diversification doesn’t work anymore. How is it supposed to help you when everything is falling apart? Does it even work? Is it worth the trouble? I’ll show you a few examples from recent years so you can see for yourself.

Related: How I turned $100 into a six-figure portfolio

Do All Markets Crash Together?

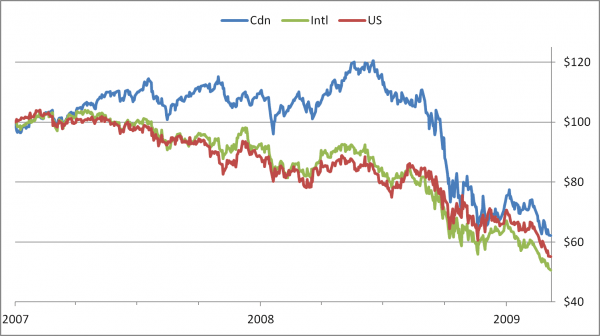

Take a look at what Canadian investors saw if they invested $100 in three major stock indexes at the start of 2007:

You can see that diversification was not dead. The markets behaved differently. It’s true that US and international markets followed each other down step for step. But the Canadian market actually rose for over a year and a half after the others passed their peak. That doesn’t mean the Canadian market is always the safest — it just happened to do a little better this time.

Related: Market efficiency: A glaring oversight in passive strategies

A disciplined investor with a rebalancing plan could have taken advantage of this to sell some Canadian stocks and buy others cheaply. Even without rebalancing the portfolio losses would be more limited at first because the Canadian market would hold it up and limit the worst effects of the crash.

Diversification protected portfolios during the crash and created opportunities even in the worst of times.

What Happened After the Crash?

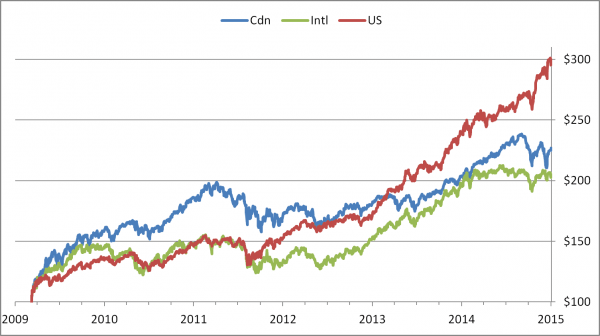

Here’s what each market did if you invested $100 on March 9 2009, when they all reached the bottom at the same time:

This time the differences are even bigger. Each market takes turns accelerating and decelerating.

Diversifying worked here too. At almost any time over the last 6 years, at least one market was doing well. Once again this created opportunities for rebalancing and protected investors from losses.

When Does Diversification Fail?

If you paid close attention you’ll notice one way that diversification didn’t work. For 6 months around the end of 2008 all three indexes were falling to similar levels relative to the start of 2007.

Related: How behavioural biases kept me from becoming an indexer

Even more surprisingly they all reached the bottom on the exact same day. If things like this happened all the time then diversifying your portfolio would be a waste of time.

But the important lesson here is how exceptional these events were. It wasn’t rational connections between markets that made them stop falling on the same day. The real reason is because that was the day when investor panic reached its peak around the world and everything was being sold whether it was good or bad.

An unusual situation like this tells us a lot. It was only when people thought the world was ending that markets started to behave the same and diversification started to break down. As soon as that fear passed it started working again.

Any time we don’t have a worldwide panic where investors expect the financial system to collapse any day, you know that each market will perform differently and betting your whole portfolio on one market is too risky.

Why I Diversify

Diversified investors will be protected from the worst surprises. That makes it easier to take advantage of opportunities. And they do all of this without having to predict economic growth or quantitative easing. They will be prepared for anything, at any time.

Related: Why investors should embrace simple solutions

There may be rare occasions where diversification does not work perfectly. But I’m not going to throw away the idea because it “only” works 99% of the time!

In these examples I only looked at three major stock market indexes. If you diversify to other types of assets like bonds and REITs then you get even more protection. Bonds kept making money through the crash and recovery in the stock market. Canadian REITs crashed in 2008 but then had a great run for the next four years.

For another example that includes more asset classes take a look at the chart here. Notice how each market bounces around from best to worst with no pattern. Some of them literally go from best to worst in one year. I’m not going to bet my portfolio on the idea that I can guess where they will end up next year.

But that’s ok because no matter what happens I can take advantage of it thanks to a diversified portfolio. That’s why the Canadian stock market is only a small part of my portfolio. And it’s why you shouldn’t cut important asset classes out of your portfolio just because they haven’t done well for the last few years or the media is saying they’re in trouble (usually when it’s too late).

Related: How to get started with an index portfolio

Diversifying your investments will always be important. In the past Canadian investors were restricted in what they could put in their RRSPs but now there is nothing holding us back except our own decisions.

Richard is an investor who teaches other Canadians how to build a safe diversified portfolio at Master Your Portfolio.