Canada Pension Plan (CPP) benefits can make up a key portion of your income in retirement. Individuals receiving the maximum CPP payments at age 65 can expect to collect $17,196 per year ($1,433 per month) in benefits.

The amount of your CPP payments depends on two factors: how much you contributed, and how long you made contributions between ages 18 and 65. Most don’t receive the maximum benefit. In fact, the average amount for new CPP beneficiaries is just $9,697.68 per year (as of January 2025).

CPP Payments 2025

The table below shows the monthly maximum CPP payment amounts for 2025, along with the average amount for new beneficiaries:

| Type of pension or benefit | Average amount for new CPP beneficiaries (Jan 2025) | Maximum payment amount (2025) | ||

|---|---|---|---|---|

| Retirement pension (at age 65) | $808.14 | $1,433.00 | ||

| Disability benefit | $1,538.67 | $1,673.24 | ||

| Survivor's pension - younger than 65 | $527.91 | $770.88 | ||

| Survivor's pension - 65 and older | $325.64 | $859.80 | ||

| Death benefit (one-time payment) | $2,500 | $2,500 | ||

| Combined benefits | ||||

| Combined survivor's and retirement pension (at age 65) | $1,017.67 | $1,449.53 | ||

| Combined survivor's pension and disability benefit | $1,293.81 | $1,683.57 |

Now, you may not have a hot clue how much CPP you will receive in retirement, and that’s okay.

The good news is that the government does this calculation for you on an ongoing basis. This means that you can find out how much money the government would give you today, if you were already eligible to receive CPP.

This information is available on your Canada Pension Plan Statement of Contribution. You can get your Statement of Contribution by logging into your My Service Canada Account, which – if you bank online with any of the major banks – is immediate.

Related: CRA My Account – How to check your tax information online

If you’d prefer to send your personal information by mail you can request a paper copy of your Statement of Contribution sent to you by calling 1.877.454.4051, or by printing out an Application for a Statement of Contributions from the Service Canada Website.

Note that the information available to you on your CPP Statement of Contribution may not reflect your actual CPP payments. That’s because it doesn’t factor in several variables that might affect the amount you’re entitled to receive (such as the child-rearing drop-out provision).

The statement also assumes that you’re 65 today, which means that later years of higher or lower income that will affect the average lifetime earnings upon which your pension is based aren’t taken into consideration.

CPP is Indexed to Inflation

Canada Pension Plan (CPP) rate increases are calculated once a year using the Consumer Price Index (CPI) All-Items Index. The increases come into effect each January, and are legislated so that benefits keep up with the cost of living. The rate increase is the percentage change from one 12-month period to the previous 12-month period.

CPP payments were increased by 2.7% in January 2025, based on the average CPI from November 2023 to October 2024, divided by the average CPI from November 2022 to October 2023.

Note that if cost of living decreased over the 12-month period, the CPP payment amounts would not decrease, they’d stay at the same level as the previous year.

CPP Payment Dates

CPP payment dates are scheduled on a recurring basis a few days before the end of the month. This includes the CPP retirement pension and disability, children’s and survivor benefits. If you have signed up for direct deposit, payments will be automatically deposited in your bank account on these dates:

All CPP payment dates 2025

- January 29, 2025

- February 26, 2025

- March 27, 2025

- April 28, 2025

- May 28, 2025

- June 26, 2025

- July 29, 2025

- August 27, 2025

- September 25, 2025

- October 29, 2025

- November 26, 2025

- December 22, 2025

Why Don’t I Receive The CPP Maximum?

Only about 6% of CPP recipients receive the maximum payment amount, according to Employment and Social Development Canada. The average recipient receives about 56% of the CPP maximum. With that in mind, it’s best to lower your CPP expectations when calculating your potential retirement income.

Why don’t more people receive the maximum? Well, because it requires 39 years of CPP contributions at the maximum level to get the biggest possible benefit in retirement. That means you need a salary that meets or exceeds the yearly maximum annual pensionable earnings threshold, which in 2025 is $71,300.

Note that there is a new Year’s Additional Maximum Pensionable Earnings (YAMPE) as part of the enhanced CPP that is being phased in over two years. This means Canadians will pay an additional 4% on the earnings between $71,300 to $81,200.

- Year YMPE

- 2025 $71,300

- 2024 $68,500

- 2023 $66,600

- 2022 $64,900

- 2021 $61,600

- 2020 $58,700

- 2019 $57,400

- 2018 $55,900

- 2017 $55,300

- 2016 $54,900

Plenty of variables affect your ability to earn the maximum CPP benefits. Maybe you joined the work force late, dropped out for a period of time, or retired early.

Related: When Should Early Retirees Take CPP?

Low income earners may not hit the YMPE level often enough to get the highest possible CPP retirement benefit. Business owners who choose to pay themselves dividends don’t need to contribute to CPP, but that means they won’t be eligible to receive benefits either.

When To Take CPP?

Perhaps the most common question about CPP is when to take it. The standard age to take CPP is at age 65. But, Service Canada may proactively send out a notice a few months before your 60th birthday advising you that you’re eligible to apply for CPP and giving you an estimate of your expected CPP payments.

You can take a reduced CPP payment starting as early as age 60. If you do elect to take CPP early, you’ll receive 0.6% less for every month you receive it before age 65. That means, for those taking CPP at age 60, a reduction in their CPP payments by 36%. Reductions aside, there could be good reasons to take CPP early – namely if you need the income sooner than 65, or if you expect to have a reduced life expectancy.

Conversely, you can enhance your CPP payments by deferring your pension up until age 70. The advantage of waiting is you’ll receive a 0.7% increase for every month you defer CPP past age 65. Taking CPP at age 70 results in a 42% enhancement to your pension. The biggest reason to defer CPP is to protect against longevity risk – the risk of outliving your money. The trade-off is using your own personal savings to tide you over until the enhanced CPP payments kick-in later in life.

Note there is no benefit to defer CPP beyond age 70, so get your CPP application in on time to avoid delays.

Final Summary

CPP is a complicated system but one that is crucial to retirement planning for many Canadians. It’s important to understand how much CPP you will receive in retirement, and to know how difficult it is to receive the maximum CPP payments. Most CPP beneficiaries receive much less than the maximum, with the average between 55% and 60% – so that’s good to know going into your retirement income planning.

You can find out an estimate of your CPP benefits by looking at your Statement of Contribution online at your My Service Canada Account, or request a paper copy by calling Service Canada.

CPP payments are indexed to inflation, with the latest increase going up by 4.8% in 2024. CPP payment dates are scheduled toward the end of every month and automatically deposited into your bank.

Finally, a big consideration is when to take CPP and how the payments fit into your retirement plan. Do you expect to live a long life? Will you work until age 65? Do you have sufficient personal savings to last until your CPP payments kick-in? Will you take CPP at age 65, or elect to take your pension earlier or later?

Readers: How does CPP fit into your retirement income plan?

It might seem counterintuitive to spend down your own retirement savings while deferring government benefits such as CPP and OAS past age 65. But that’s exactly the type of strategy that can increase your income, save on taxes, and protect against outliving your money. Indeed, the key to more lifetime income for many retirees is to defer CPP until age 70.

Why Take CPP at age 70?

Here are three reasons to take CPP at age 70:

1. Enhanced Benefit – Take CPP at 70 and get 42% more!

The typical age to take your CPP benefits is at 65, but you can take your retirement pension as early as 60 or as late as age 70. It might sound like a good idea to take CPP as soon as you’re eligible but you should know that by doing so you’ll forfeit 7.2% each year you receive it before age 65.

That’s right, you’ll get up to 36% less CPP if you take it immediately at age 60 rather than waiting until age 65. That alone should give you pause before deciding to take CPP early. What about taking it later?

There’s a strong incentive for deferring your CPP benefits past age 65. You’ll receive 8.4% more each year that you delay taking CPP (up to a maximum of 42% more if you take CPP at age 70). Note there is no incentive to delay taking CPP after age 70.

Let’s show a quick example. The maximum monthly CPP payment one could receive at age 65 (in 2025) is $17,196. Most people don’t receive the CPP maximum, however, so we’ll use the average amount for new beneficiaries, which is $808.14 per month. Now let’s convert that to an annual amount for this example = ~$9,700.

Suppose our retiree decides to take her CPP benefits at the earliest possible time (age 60). That annual amount will get reduced by 36%, from $9,700 to $6,208 – a loss of $3,492 per year.

Now suppose she waits until age 70 to take her CPP benefits. Her annual benefits will increase by 42%, giving her a total of $13,774. That’s an increase of $4,074 per year for her lifetime (indexed to inflation).

2. Save on taxes from mandatory RRSP withdrawals and OAS clawbacks

Mandatory minimum withdrawal schedules are a big bone of contention for retirees when they convert their RRSP to an RRIF. For larger RRIFs, the mandatory withdrawals can trigger OAS clawbacks and give the retiree more income than he or she needs in a given year.

The gradual increase in the percentage withdrawn also does not jive with our belief in the 4 percent rule that will help our money last a lifetime.

You can withdraw from an RRSP at anytime, however, and doing so may come in handy for those who retire early (say between age 55-64). That’s because you can begin modest drawdowns of your retirement savings to augment a workplace pension or other savings to tide you over until age 65 or older.

Related: When Should Early Retirees Take CPP?

Tax problems and OAS clawbacks occur when all of your retirement income streams collide simultaneously. But with a delayed CPP approach your RRSP will be much smaller by the time you’re forced to convert it to a RRIF and make minimum mandatory withdrawals.

With careful planning (and appropriate savings) your retirement income streams by age 70 could consist of CPP and OAS benefits, small RRIF withdrawals, plus – the holy grail – TFSA withdrawals, which do not count as income and won’t affect means-tested benefits like OAS.

3. Take CPP at age 70 to protect against longevity risk

Here’s where the counter-intuitiveness comes into play. Most default retirement projections will have you taking CPP at age 65 (or earlier) while delaying withdrawals from your RRSP and/or LIRA until age 71.

As I suggested above, the idea is to spend down some of your RRSP before age 70 to fill the gap left by deferring your CPP benefits. Good luck getting your commission-paid advisor to buy into this approach. I doubt many advisors would like the idea of spending down your savings early in order to maximize retirement benefits from CPP.

“Spend your risky dollars first because they may not be there for you in your 80s, depending on how your investments do. A bigger CPP cheque, however, will definitely be there for you.” – Fred Vettese

Spending down your RRSP in your 60s while deferring CPP until age 70 is like converting your risky assets (personal savings in the stock market) into a guaranteed income stream for life.

Related: 5 ways to save your retirement

Think about it. Will you still have the required mental faculties at age 80 or 90 to continue managing your own retirement assets? Or would you prefer to enjoy spending those assets in your 60s and 70s, knowing you still have an enhanced (and guaranteed) income stream to last a lifetime?

If your biggest fear in retirement is outliving your money then why not design your retirement income streams to protect against that very fear? Instead, most retirees take their CPP benefits the first chance they get – leaving additional money on the table and giving up a portion of that longevity risk protection.

Let’s hear it: Retirees, when did you take CPP? Soon-to-be retirees, have I given you a compelling argument to take CPP at age 70?

In previous articles I’ve looked at reasons to delay taking CPP until age 70, along with explanations why you might want to take CPP earlier at age 60. But in this article I’m going to explain why you shouldn’t take CPP at age 65.

The most compelling reason to defer CPP is the increase or enhancement of your benefit – 0.7% for every month you delay past 65. Wait until age 70 and you’ll receive 42% more CPP than if you took it at age 65. Taking CPP early can also be an attractive option for those with a reduced life expectancy or for those who simply need the money right away.

Once you’re close to age 60, Service Canada will mail you an application form, along with an estimate of your CPP benefits. Curious, since this behavioural “nudge” may influence you to take CPP early at a reduced rate, rather than waiting until the standard retirement age of 65.

Finding out the optimal age to take CPP requires a break-even analysis and depends on a number of factors, including how much you’ve contributed and for how many years, plus a guess on how long you’ll live. Also playing a role is your current and future tax bracket, your income needs now versus in the future, plus the impact that taking CPP early has on means-tested benefits such as GIS and OAS.

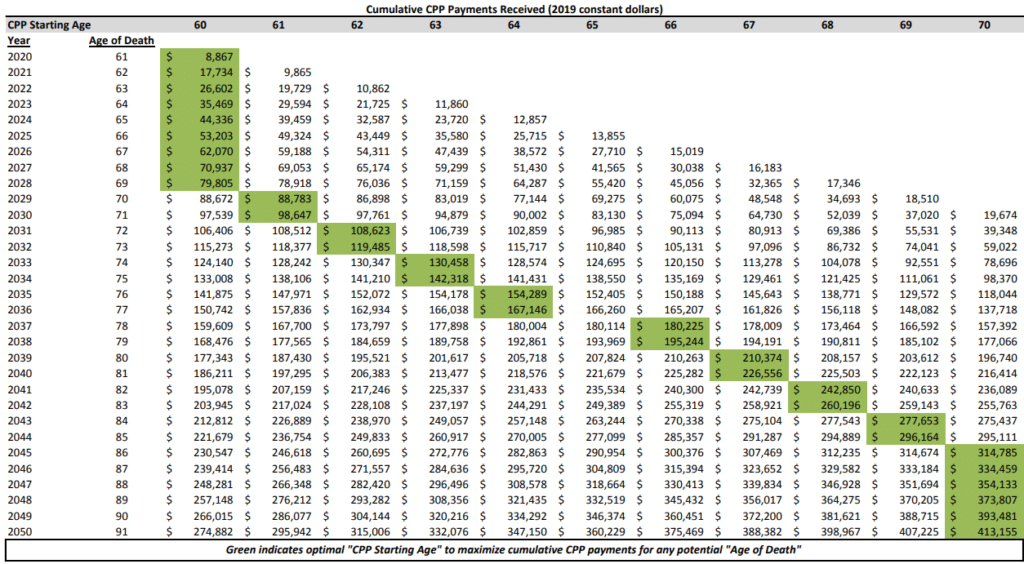

What’s interesting about the break-even analysis for CPP is that the standard retirement age of 65 is never the optimal age. Let me explain:

Why Not Take CPP At Age 65?

In I post I wrote years ago about taking CPP early or late, Canada Pension Plan expert Doug Runchey shared with me the interesting fact that taking CPP at 65 is never the optimal choice from a payout perspective.

Indeed, Aaron Hector, a financial planner at Doherty & Bryant Financial Strategists, expanded on that fact with an interesting analysis on optimal CPP starting ages.

Hector looked at two scenarios; one in which the retiree spends all of his or her CPP benefits, and one in which the retiree invests their CPP and earns a 3% real return after taxes.

What he found was that taking CPP at age 60 was best for those who live only until age 69 (when CPP was spent), or until age 71 (when CPP was invested). Taking CPP at age 70 was optimal for those who live until age 86 and beyond.

As you can see, age 65 is never the optimal starting age to take CPP. That said, you could argue that 65 is the sweet spot between the two extremes of taking CPP early or late.

It’s helpful to know that the normal life expectancy at 60 for a Canadian is 25 years. So, if you don’t have any reason to believe you’ll have a shorter or longer life expectancy then 85 is a good age to use as a benchmark for your own break-even analysis. In this case, the optimal age to take your CPP payments and receive the most money is age 69.

Taking CPP early and investing

There’s a mindset among some retirees that they should take CPP as soon as possible and invest. The idea being that the longer their investments can compound, the better off they’d be versus delaying CPP beyond age 65.

But Hector’s analysis should put a damper on any expectation that taking CPP early and investing will lead to a better outcome. This could be due to overconfidence in one’s investing ability, over over-optimism about the expected rate of return. In any case, as you’ll see below, taking CPP at 60 and investing the entire amount only improves the optimal outcome by two years.

It’s hard to beat a guaranteed 7.2% a year increase in CPP benefits just by delaying your application. There’s also a practical argument against this approach. Is the object of the game to amass the largest bank account before you die? Or is it to spend and enjoy what you worked so hard to earn in retirement?

In my mind, it’s not a rational argument that a retiree will invest every single dollar of CPP benefits. At some point we’re going to spend our money.

Final thoughts on taking CPP at 65

The standard retirement age of 65 is embedded in our society and triggers most Canadians to take their CPP benefits at that age – like a rite of passage for retirement. But what I’ve explained here clearly shows that it’s never optimal to take CPP at age 65, from a purely financial perspective.

If anything, this analysis and research should at least give us pause before automatically applying for CPP at age 65. Look at your family history – are they leading long and healthy lives, or is there a trend of illness or disease? Beyond that, what kind of shape are your finances in today? Where will your retirement income streams come from? Do you fear you’ll outlive your money?

All of these questions should play a role in your decision as to whether to take CPP early, late, or somewhere in-between.