The Consumer Price Index (CPI) measures changes in prices paid for a basket of goods and services (i.e., inflation). For the past three decades the Bank of Canada has successfully targeted an inflation rate of between 1% and 3%. The latest figures show year-over-year inflation at 1.9%.

But as you know, our personal inflation rate can vary widely from the basket of goods and services used to measure CPI. There are eight major categories, which include:

- Food

- Shelter

- Household operations, furnishings and equipment

- Clothing and footwear

- Transportation

- Health and personal care

- Recreation, education and reading

- Alcoholic beverages, tobacco products and recreational cannabis

We’re going to focus on the food category. Covid-19 has had a major impact on food spending and consumption in Canada. Before the pandemic, 62% of personal food consumption was purchased at retail grocery stores, and 38% was consumed outside the home.

At the beginning of the pandemic, food spending and consumption shifted to 91% retail grocery and just 9% of food spending outside the home. This makes perfect sense, as many businesses closed, and people stayed at home as much as possible. This immediate shift in spending also resulted in disruptions to the supply chain and shortages of items like toilet paper and bread flour.

As lockdown restrictions eased in the summer and into the fall, we’ve seen food spending shift again to 75% retail grocery and 25% dining out.

Food Inflation and Changes in Consumption

Food inflation has trended higher than the CPI for many years. What can we expect as we head into 2021? According to a report issued by Dalhousie University, University of Guelph, University of Saskatchewan and University of British Columbia, Canadian families can expect their household food bill to increase by more than 5% next year.

“Canada’s food inflation index has outpaced the general inflation index over the last 20 years, and that trend is likely to continue for a while,” the report said.

source: tradingeconomics.com

The report indicated the premium for consuming food outside the home is between 40-45%, so even though prices at the grocery store have increased, overall household food spending may be lower if more people are buying groceries instead of dining out.

In a recent episode of the Stress Test podcast, co-hosts Roma Luciw and Rob Carrick looked at how Covid-19 has shifted out food spending. Two areas they focused on was the rise of meal kit delivery services like HelloFresh and Chefs Plate, and the growth of online grocery shopping and delivery.

Roma tried one of the options and wasn’t overly impressed, saying the portions were small, the price per person was high, and that the kit came with an uncomfortable amount of plastic packaging. The main benefit is saving time figuring out what to make for dinner, although you still need to prepare the meal yourself.

Rob wasn’t a fan of online grocery shopping, saying he’d prefer to pick out items himself rather than relying on a grocery picker to find the best produce and cuts of meat. He was also concerned about the grocery picker substituting other brands or similar items that may not be desirable.

My Personal Food Inflation and Consumption

The pandemic has certainly impacted our food spending as well. We weren’t big spenders on dining in the first place, but our spending on food prepared outside the home has decreased by 26% this year. Meanwhile, our retail grocery spending is up 7%.

As a percentage of our household food bill, groceries make up more than 86% of that total, which is up from 81% last year.

| Grocery increase | Dining increase | Groceries % of Food | Dining % of Food | |

|---|---|---|---|---|

| 2020 | 7.01% | -26.03% | 86.35% | 13.65% |

| 2019 | 19.09% | 22.01% | 81.39% | 18.61% |

| 2018 | 0.01% | -17.62% | 81.76% | 18.24% |

| 2017 | 16.36% | 11.24% | 78.48% | 21.52% |

| 2016 | 12.50% | 2.97% | 76.15% | 23.85% |

The biggest change in our food spending during the pandemic has been in the way we purchase groceries. Almost all of our grocery shopping is now done online (and delivered) through Save On Foods and Spud.ca.

We definitely pay a premium for this service, not just in extra delivery charges but we’re less apt to find a bargain in store. On the other hand, when shopping in person I tend to wander the aisles and pick-up items that aren’t necessarily on the grocery list.

The advantage of grocery shopping online, outside of limiting my trips outside of the house, is saving time. It takes 10 minutes or so to complete an order online, versus the hour or more spent driving to and from the store, shopping, and waiting in line at the checkout. That’s more time I can spend working on my business or hanging out with my family. A good trade-off.

I’ll concede to Rob’s point that we don’t always get the best selection of produce, and sometimes items are substituted or end up being out of stock.

We have yet to try a meal delivery service (despite the constant barrage of flyers in our mailbox). I agree with Roma’s concerns about getting value for the meal kit – small portions and a high cost per person. Plus, we’re not busy professionals working outside the home and pressed for time. We both work at home.

Finally, our family switched to a vegan diet (no meat, eggs, or dairy) last fall. While I expected a decrease in our household food bill over time, so far that hasn’t been the case. I suspect this is because we spend more on good quality produce, plus meat and dairy substitutes tend to be more expensive alternatives. No, we don’t just live on rice and beans.

That said, our diet doesn’t lend itself to meal delivery services or to dining out that often. That’s fine. We’ve found great recipes and we love to experiment with new dishes by cooking at home. I expect our food spending and consumption will continue to stay in the 85-15 ratio of retail grocery to dining out.

How has your food spending changed this year?

Fewer than 1% of eligible recipients choose to take their CPP benefits at 70. Most Canadians take CPP at age 60, as soon as they’re eligible, perhaps unknowingly giving up substantial lifetime income.

Dr. Bonnie-Jeanne MacDonald, Director of Financial Security Research at the National Institute on Ageing, wants to change the conversation around when to take CPP. Her latest research looks at the substantial (and unrecognized) value of waiting to claim CPP/QPP benefits.

I had the pleasure of speaking with Dr. MacDonald about this research and her key findings. She says the financial services industry needs to reframe its messaging to clients about the decision to take CPP. Rules of thumb aimed to make decisions easier can ultimately lead to confusion and even incorrect solutions.

The study describes three reasons why retirement planning practices currently encourage Canadians to take their benefits early.

- Lack of advice – More than two-thirds of Canadians nearing or in retirement do not understand that waiting to claim CPP benefits will increase their monthly pension payments.

- Bad “good” advice – Canadians who do seek retirement financial planning advice are being encouraged to take CPP/QPP benefits early using concepts like “breakeven age” to explain the decision. More on this later.

- Bad “bad” advice – This includes poor anecdotal advice from friends and family, and advice influenced by potential conflicts of interest from a financial advisor.

Dr. MacDonald says the breakeven approach is misleading and has been proven to powerfully influence the decision to take CPP early.

“It pushes people to mentally gamble their subjective life expectancy against the “breakeven” age.”

Indeed, a 60-year-old male has a 50% chance of living to age 89, while a 60-year-old female has a 50% chance of living to age 91.

CPP Lifetime Loss

Changing the conversation around CPP starts with using behavioural psychology to reframe the problem. Enter the “Lifetime Loss” concept that demonstrates the expected financial loss of taking CPP earlier rather than later. It encourages Canadians to look beyond the short-term and consider their entire financial future.

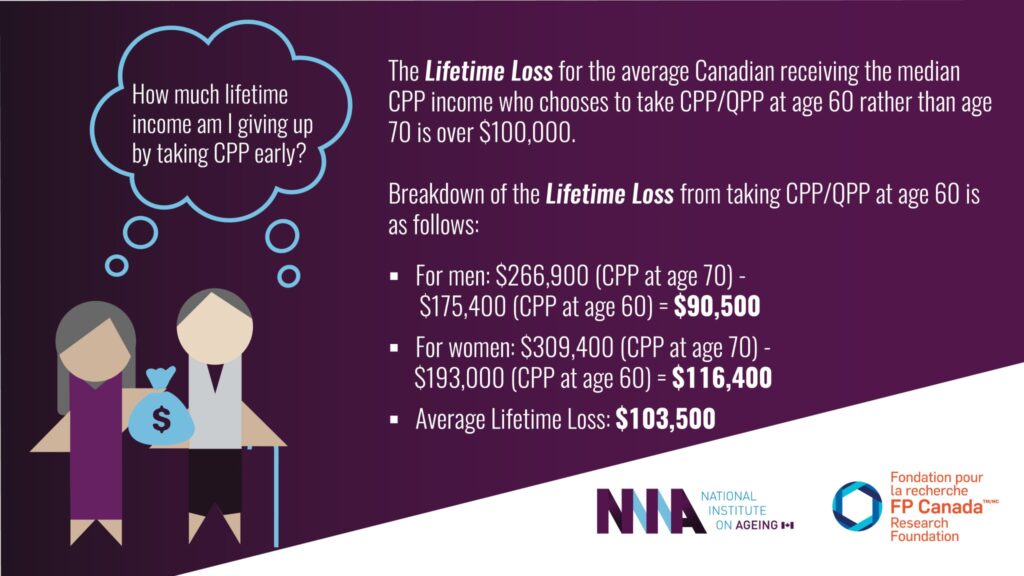

“An average Canadian receiving the median CPP income who chooses to take benefits at age 60 rather than age 70 is forfeiting over $100,000 (in current dollars) worth of secure lifetime income.”

Dr. MacDonald says we should be using behavioural psychology techniques to influence the CPP uptake decision, such as changing how the information is framed by advisors (using lifetime loss framework instead of breakeven age), to the application forms sent out by Service Canada, which may be unknowingly encouraging Canadians to apply for CPP early.

Finally, Dr. MacDonald and I discussed the issue of retirement spending for older Canadians. Most people believe expenses will decline as we age since we’re no longer spending as much on travel and hobbies. But Dr. MacDonald says that long-term care is a greater concern, and that 75% of home care for older Canadians is currently provided by family members (unpaid).

That dynamic will change in future years. Retiring Canadians now have fewer adult children, and those children are more likely to be geographically separated from their families than past generations.

“Without adequate family support, work that has traditionally been done for free (e.g., transportation, daily care, preparing meals, etc.) will come at a cost, and those services are expensive to replace.”

This makes deferring CPP an attractive option, as you’re essentially purchasing a very secure pension at an excellent price. The financial incentives are even higher than we think. By deferring CPP from age 65 to 70, you will increase your retirement benefit by 42% (0.7% for every month you defer). But this fails to account for the inflation-adjustment applied to CPP benefits. The real increase is closer to 50% (49.2%).

I encourage you to read the research paper – it’s lengthy but written in plain language with clear visuals that explain the key findings and solutions.

This Week’s Recap:

There was a lot of interest in my post highlighting Emerge ARK ETFs and their eye-popping returns. Several of you asked if I would invest in these myself. The answer is no. I’m 100% dedicated to my total market approach to investing, and I avoid anything that will tempt the irrational part of my brain to try to chase returns.

But just because I’m an emotional robot when it comes to investing doesn’t mean that you are. Many readers (and clients) have dabbled in tech stocks this year (through ARK ETFs, or Invesco’s QQQ, or by simply picking individual stocks). It’s hard not to get caught up in the frenzy when tech stocks have been driving the stock market returns for many years.

I don’t advocate for picking individual stocks at all, but I recognize that some investors want to express themselves through their portfolio by owning what they know, or what’s new and exciting, or what hedges their fears.

That’s why I’d prefer to see investors build some guardrails around their behaviour by limiting their “explore” to no more than 5-10% of their portfolio, avoiding individual stocks, and instead choosing a thematic (and more diversified) ETF to scratch that itch.

My guardrails include avoiding stock market news (“What investors need to know about the stock market today”), avoiding looking at my investments as much as possible, and staying 100% invested at all times. This way I’m rarely tempted to do anything with my portfolio.

Promo of the Week:

Just a reminder to join our new (private) Facebook group – Personal Finance Canada – where we’ve been having some great discussions about investing, retirement, credit cards, and more.

The group is administered by me and travel expert Barry Choi, but we also have other experts in the group on CPP, retirement planning, and investing there to answer your burning questions about money.

Please join us and leave a question or comment for the group.

Weekend Reading:

There’s still time to enter the $1,000 cash Christmas giveaway over at Credit Card Genius.

The Measure of a Plan website has updated its investment portfolio tracker – a spreadsheet for DIY investors.

My Own Advisor’s Mark Seed and Money Coaches Canada’s Steve Bridge explain what is a financial plan and what it should cover.

Michael James on Money explains how to transition your investment portfolio as you head into retirement.

Millionaire Teacher Andrew Hallam uses The Misguided Beliefs of Financial Advisors paper to show how advisors punch themselves by purchasing actively managed mutual funds and chasing past performance:

“I was surprised to learn the advisors ate their own cooking…and burned their own food. They bought themselves actively managed funds instead of index funds. In other words, they bought the same things for themselves that they recommended to their clients. That doesn’t reveal a lack of ethics–just a lack of knowledge.”

File this under something I usually ignore, but is interesting nonetheless. Maclean’s “charts to watch in 2021.”

Rob Carrick shares a new option for safely parking U.S. dollars, plus a 2.3% TFSA savings account.

Jason Heath continues to descend into the particular, this time with ways to unlock retirement savings in a LIRA.

Morgan Housel shares another gem with “A few things I’m pretty sure about.” I completely agree with this one:

“Most professions would benefit from at least one a day month where you did nothing but think. No meetings, no calls, no deliverables. Just a seat on the couch thinking about what’s working, what’s not, and what to do about it.”

Finally, a must-read by Zandile Chiwanza on why she had to use her “white-passing” middle name to get an apartment in Toronto.

Have a great weekend, everyone!

HSBC Canada made history this week when it announced a 0.99% mortgage rate – the lowest advertised rate ever offered in Canada. The 0.99% mortgage rate is available for high-ratio insured purchases (i.e. for those putting less than 20% down). It’s not a fixed rate, but a steeply discounted variable rate of prime minus 1.46%.

RateSpy.com also reported that HSBC launched three more record-low mortgage rates, including 1.39% on a 5-year fixed rate mortgage (high-ratio insured purchases), 1.59% on a 5-year fixed rate for uninsured purchases and switches, and 1.64% on a 5-year fixed rate for refinances. Incredible.

It seems like a no-brainer to take advantage of a 0.99% variable rate mortgage, given that the Bank of Canada has pledged to maintain its key lending rate at a historic low until at least 2023. That’s at least two years of sub-1% borrowing.

“At this point, we can’t blame any well-qualified insured borrower for wanting a piece of this rate. And HSBC’s floating-rate features are fantastic. It’s a standard-charge mortgage that’s fully open after three years and you get to convert to a fixed rate anytime without penalty (not that we’re advocating that). That’s not to mention the much more favourable 3-months’ interest penalty of a variable versus a fixed.” – RateSpy.com

I remember when BMO made headlines in 2012 when it offered the first sub-3% fixed rate mortgage (a 4-year with conditions, if memory serves). Eight years later, HSBC has broken the 1% barrier.

Meanwhile, I have clients and readers who still have mortgage rates above 3%. If you find yourself in that position, it’s time to seriously consider refinancing your mortgage. A mortgage broker can help you run the math and determine if it makes sense to pay a penalty to break your existing mortgage and refinance into one of these record low mortgage rates.

This Week’s Recap:

I was happy to contribute to Young & Thrifty’s Financial Literacy Month piece with my top financial lesson for Canadian millennials.

Last week I explained why I switched back to the Scotia Momentum Visa Infinite card for my everyday spending.

Stay tuned for a couple of interesting profiles coming up on the blog – one that looks at a small family of ETFs with eye-popping returns, and another that looks at a new online service for arranging funerals.

I was happy to see that Wealthsimple Trade (the zero-commission trading platform) has launched a desktop version of its platform (currently in beta and not available to all users). I moved my RRSP and TFSA to WS Trade in January and so far have really enjoyed the experience.

I’m also amazed at the resiliency of the stock market. When my portfolio was down 34% in March, I would have never predicted it would rally and actually be up 7.41% on the year. Unbelievable. I might have an outside shot at reaching my $1M net worth milestone at the end of the year.

Wealthsimple Trade is Canada’s first and only zero-commission trading platform where investors can trade stocks and ETFs for free in an RRSP, TFSA, or non-registered account. Sign up for Wealthsimple Trade today and get a $10 cash bonus.

Weekend Reading:

Our friends at Credit Card Genius have the best credit card offers, sign-up bonuses, and deals for the month of December.

According to the National Institute on Aging, 95 per cent of Canadians take CPP at the age of 65 or earlier, with only 1% deferring until the maximum age of 70.

Michael James on Money offers a case study on his family’s CPP timing choice.

My Own Advisor Mark Seed interviews CPP expert Doug Runchey on the survivorship benefits for CPP and OAS.

A detailed and excellent look at CPP’s commitment to Canada 2050 (Canada’s path to net-zero emissions).

Working longer appears to boost longevity. Here’s Andrew Hallam on the retirement solution that could extend your life.

MoneySense’s Jason Heath shares some unique ideas for your last will and testament.

Rob Carrick answers a reader question about whether it makes sense to use preferred shares as a bond substitute.

Why wouldn’t you want to invest in the companies leading a new world-changing technological paradigm? Ben Felix explains in his latest Common Sense Investing video:

Our vision of the good life is stuck in the twentieth century. Max Fawcett says it’s time to reinvent it—starting with home ownership:

“If you showed someone from the late 1950s the typical Middleton life today, they would probably think society had made extraordinary economic advances. How else could someone middle class afford a beautiful car, an enormous new house (relative to what was normal, say, seventy years ago), and access to the kind of food and wine once the exclusive preserve of royalty and the very rich?”

Rich as I say, not as I do. Nick Maggiulli (Of Dollars and Data) takes issue with many so-called personal finance experts who have gotten wealthy by selling advice to others rather than by using their own advice.

Wealthsimple CEO Michael Katchen says the best path to financial literacy is to build products that people actually understand.

Finally, I want to share this excerpt from Global’s Money123 newsletter (subscribe to it here). It’s an answer to a reader question about retiring on a low income. Here’s the must-read advice from low-income retirement specialist John Stapleton:

“Max out your tax-free savings account (TFSA) when you can and any equivalent employee contribution while working. Avoid RRSPs if you are under age 65 and cash them out slowly before age 65 if you have them. Pay the tax penalty. Put the leftover money in a TFSA.

Take the Canada Pension Plan (CPP) early at 60 unless you receive social assistance.

Apply for Old Age Security (OAS) one month after you turn 64. The OAS application is the same form as that for the Guaranteed Income Supplement (GIS). Apply for the GIS. Don’t tick the box that keeps you from applying for GIS.

If you are GIS-eligible at 65, register for an RRSP with any money you have between ages 65-71. If you don’t have money, consider borrowing from the same institution where you open your RRSP. OAS and the GIS begin at age 65. But people can keep contributing to RRSPs until they turn 71. Contributing to an RRSP effectively lowers your income for purposes of GIS eligibility.

Pay attention to fees. Avoid actively managed funds. Make sure your financial advisors commit to fiduciary standards. Buy inexpensive, well-diversified mutual funds such as D-series funds and always buy from a discount brokerage that you can find online. Never buy or sell individual securities.

Get a no-fee credit card with a low limit. Use it to pay for things but pay your credit card balance in full every month.

Maximize tax-advantaged savings vehicles like registered education savings plans (RESPs) if you have children and TFSAs for each family member who is eligible.

Maximize all entitlements but do everything you can to avoid social assistance whenever possible.

Print this page and keep it with you.”

Have a great Sunday, everyone!