When To Take CPP: Early, Late or Somewhere In-Between

One of the biggest decisions as you edge closer to retirement is when to take CPP. The standard age to take your Canada Pension Plan benefits is when you turn 65; but you can take a reduced CPP retirement pension as early as 60, or you can get an increased benefit by delaying CPP up to age 70.

I asked Doug Runchey, pension expert at DR Pensions Consulting, to weigh-in on the benefits of taking CPP early versus late.

Taking CPP early

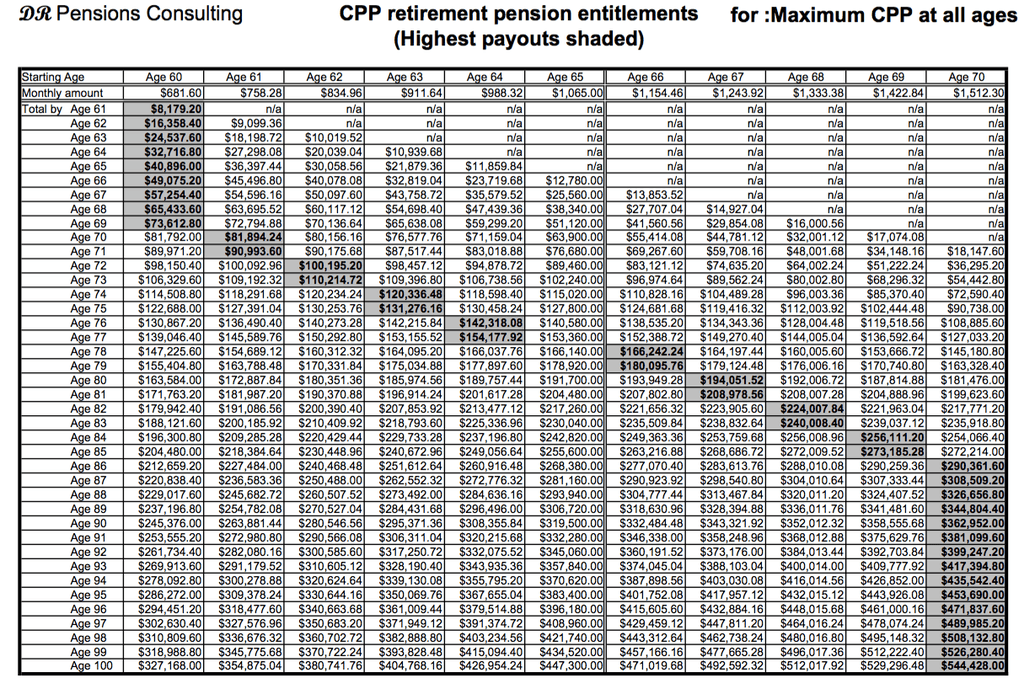

The earliest you can take your CPP benefits is the month after your 60th birthday, but you’ll get 36 percent less than if you had waited until 65.

This chart shows the monthly CPP pension you’d receive if you retired in 2016 and elected to take your benefits early:

| Age | Reduction | Monthly benefit* |

| 60 | 36.0% | $681.60 |

| 61 | 28.8% | $758.28 |

| 62 | 21.6% | $834.96 |

| 63 | 14.4% | $911.64 |

| 64 | 7.2% | $988.32 |

*Assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP early:

When you take CPP at 60, your benefits are based on your best 35 years of earnings, rather than your best 39 years of earnings if you were to take it at 65.

If you’re confident that you will be eligible for the Guaranteed Income Supplement (GIS) once you reach 65, you should generally take your CPP at 60.

Finally, if you’re thinking about taking CPP early because of ill health, always apply for a CPP disability pension instead.

“If approved, the CPP disability amount will always be higher than a retirement pension and it will convert to a full retirement pension at 65,” says Runchey.

Taking CPP late

The advantage to taking CPP after 65 is that you’ll receive a healthy 8.4 per cent increase for each year you delay receiving benefits, up to age 70. That works out to a 42 percent incentive for taking CPP at 70 instead of 65.

This chart shows the monthly CPP pension you’d receive if you delayed taking your benefits until after age 65:

| Age | Increase | Monthly benefit* |

| 66 | 8.4% | $1,154.46 |

| 67 | 16.8% | $1,243.92 |

| 68 | 25.2% | $1,333.38 |

| 69 | 33.6% | $1,422.84 |

| 70 | 42.0% | $1,512.30 |

*assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP late:

You will always get more CPP by waiting, even if you’re not working.

Runchey says that your “calculated (age-65) retirement pension” may decrease if you’re not working between age 60 and 65, but the age-adjustment factor will always make up for that decrease, and then some.

“In that situation I use the expression that you will receive a larger piece of a smaller pie if you wait, but you will always get more pie,” he said.

If you’re withdrawing RRSPs from age 60-70, it makes sense to defer your CPP until age 70 when you might be in a lower tax bracket.

The Verdict: When to take CPP

The choice of when to take CPP should be based on your individual numbers and take into account your life expectancy, current and future tax bracket, your immediate versus future income needs, plus the impact that taking CPP early has on any other benefits that you’re receiving, such as GIS and OAS.

One thing that’s clear, according to Runchey, is that taking CPP at 65 is never your optimal choice from a CPP payout perspective.

The bottom line: You will always eventually be ahead if you take CPP later.

As you can see from this chart (click to open in a new window), you will be ahead financially – considering the CPP only – if you take your CPP:

- At age 60 and if you don’t live past age 69

- At age 61 and if you live past age 69 but not past age 71

- At age 62 and if you live past age 71 but not past age 73

- At age 63 and if you live past age 73 but not past age 75

- At age 64 and if you live past age 75 but not past age 77

- At age 66 and if you live past age 77 but not past age 79

- At age 67 and if you live past age 79 but not past age 81

- At age 68 and if you live past age 81 but not past age 83

- At age 69 and if you live past age 83 but not past age 85

- At age 70 and if you live until at least age 86

Final thoughts

If you're unsure about your Canada Pension Plan benefits, have questions about the optimal time to take your CPP benefits, or simply want to go over some different scenarios, I highly recommend consulting Doug Runchey at DR Pensions. He charges a fee-for-service, and in many cases it is well worth the money.

Also read:

Understanding your retirement benefits: Part 1 – CPP

Understanding your retirement benefits: Part 2 – OAS

Understanding your retirement benefits: Part 3 – Private Pension Plans

CPP's child-rearing dropout provision

I am wondering about survivor’s benefits and CPP. How does that effect whether you take it early or later?

Leah

How a CPP survivor’s pension is calculated when it’s combined with a CPP retirement pension is certainly something to consider when deciding when to take your CPP. Here’s a link to an article that I wrote on this subject: http://retirehappy.ca/cpp-survivor-benefits/

I am wondering the same thing as Leah, as to how it affects the survivor’s benefit. When I researched this a while back, it seemed that it didn’t affect it either way. Also that the survivor amount cannot make that person’s pension over the max Canada pension amount either. Please confirm. Thank you.

Linda

As per my reply to Leah as above, I recommend that you read this article: http://retirehappy.ca/cpp-survivor-benefits/

Excellent article, I’m getting close to the age for early access and it covers the questions and concerns I have. Keep up with the articles.

If you have a spouse with no pensions, savings and few CPP contributions they it may be worth going later so they have more security for life, they would inherit more of your CPP, subject to the max per month. I have seen stay home Mums or farm wives with zero CPP .

I also think people underestimate the guaranteed and increasing nature of this, we are jealous of people with company defined benefit pensions yet cash this out early!

Doug Runcheys website is brilliant!

Kathy Waite Saskatchewan

Kathy

Thanks for the positive feedback on my website.

I just want to correct you on how the survivor’s pension works though. The amount of the CPP survivor’s pension is based on the “calculated” or “unadjusted” CPP retirement pension, and not on the actual retirement pension amount.

It therefore won’t be more if someone delays in applying for their retirement pension, and it may even be less if they’re not working and contributing after age 60.

Something you did not mention is the opportunity to invest the early CPP into something with a decent rate of return. That $40,000 received over the first 5 years from 60-65 must be taken into account when we are doing calculations of how much we “get” shouldn’t it? If I put my taken early CPP of $600/month into my RSP at 5% do I not get a double return in investment by deferring those taxes and earning interest?

I keep asking the same question. If you don’t calculate the earnings on the money you would not of have, or the Tax deduction from putting it into your RRSP. These calculations don’t seem correct.

I wonder if these calculations take the $40,000 and use it monthly to supplement the cpp (even with not interest)at the later date. I would put it into my TFSA and then pull it out and leave the RRSP alone and then get the OAS andGIS ! Just don’t quite understand how it was calculated.

I began my own business at age 54. I elected to take dividends rather than salary therefore no CPP contributions are made. My CPP benefit according to the website was very close to the max. How will zero contribution years from 54 to 60; or 54 to 65 affect my benefit?

Ardee

Depending on your earnings from age 18 to 54, your CPP might still be close to the maximum if you take it at age 60, but it will definitely be reduced if you wait until age 65.

I could do some calculations for you (for a fee) if you email me a copy of your CPP statement of contributions to DRpensions@shaw.ca

Exactly – cookie cutter advice or one size fits all can get you into trouble – I’m (was) in the same boat as Ardee – delaying CPP would have cost me money (i.e. decreased benefit) not the always touted “delay for as long as possible” – would be really nice if the advice included the caveat rather than blindly spouting the same mantra

Here is what Moshe Milevsky has said,

“Those who delay claiming CCP income to the latest age possible are effectively buying a real (inflation adjusted) advanced-life delayed annuity, with a survivor benefit for the spouse. The implied longevity yield from such a stategy far exceeds the rate of return available from real or nominal bonds in today’s environment of ultra-low interest rates, especially for people in better than average health. For them, delaying annuitization is optimal.”

I also like what Jonathan Clements has said, (tongue in cheek)

“If you and your spouse fully intend to die early in retirement, then claiming early is the optimal strategy”

Having used Doug Runchey’s services, I can highly recommend him.

I have a question,

One of the other blogs mentioned a drawback if one retires and does not collect the cpp for several years, if one has more than 8 years without maximum contribution then the cpp calculation is based on a smaller average and the increase of the cpp on waiting is offset partially by additional no income years. Is that true?

Tom

It is true that your average earnings could be decreasing if you wait to apply for your CPP, and you might not benefit fully from higher percentage of the benefit that you will get by waiting. I refer to this situation as waiting to receive a larger slice of a smaller pie, but you’ll always get more pie if you wait.

In your summary after the chart, “you will be ahead financially – considering the CPP only”. The problem with that qualifier is that almost everyone has other considerations, even with CPP. Things are just so much more complicated for almost everyone. I cannot cover all my thoughts thoroughly here, but I will throw a few things out there.

With CPP alone, the decision to stop paying into it and the decision to start collecting from it are entirely separate. I developed a much more complex spreadsheet that takes into account assumed growth of the money withdrawn and the money saved by contributing less to CPP up to 65. Paying into it is almost a 10% tax if your income is around 50,000. There is a good argument to try to avoid employment income before 65 in lieu of RSP and other income, to avoid the CPP “taxation”. If you want to defer something for higher return OAS after 65 is a better bet, as it does not cost you.

As to making more money by the time you are in your 80’s, why? Your world travels, yacht and sports car will not be important by then. The truth is the money is worth much more to you in your early 60’s than later. (would you rather buy a ticket to Europe each month at 65 or a trip to Madagascar each month at 85?) My own guess is that the earlier the better for tapping CPP for almost everyone. If you are self-employed this is almost a certainty. It is true that the net amount you receive is greater if you wait and also live long, but between inflation and lifestyle it won’t really matter.

I should mention, this exercise is not theoretical for me. I retired at 60 and am now 62. I started taking CPP a few months ago, and I have started dipping into my RRSP to avoid some of the CPP contributions.

Robert

As per my reply below, I’m not sure how dipping into your RRSP saves you any CPP contributions unless it simply allows you not to work which means you don’t have to contribute.

If you did make further contributions after you’ve started receiving your CPP though, you would earn some PRBs (post-retirement benefits) from CPP.

To answer your question. It is really not complex at all. I can withdraw money from my corporate account or my RSP. Before 65 I am forced to pay CPP premiums on money I withdraw from the corporate savings as it is “normal” income, but not from RSP withdrawals which are not subject to CPP premiums. The CPP premiums are around 10% on the first 50k, to round things for simplicity.

Anyway, bottom line is that before 65 there is no CPP premium applicable to RSP withdrawals. After 65 there is no mandatory CPP premium anywhere.

Robert

I agree with you that it’s rarely so simple as to just consider the total CPP payout, but I still think that knowing the accurate numbers is an important starting point.

I’d just like to clarify one of your points.

There is no choice to stop contributing to CPP until after age 65, and only then if you are receiving your CPP retirement pension (unless you have no employment earnings, in which case you won’t have to make any contributions regardless whether you’re receiving CPP or not).

Actually, if you stop taking employment income you do not have to pay CPP premiums at any age. CPP premiums only apply to employment income.

After 65 it is a choice even with employment income.

If you live off your RSP or other savings until 65 you do not need to contribute to CPP premiums. After 65 there are no mandatory premiums to CPP, so that is a better point to draw money from a corporate account if you are inclined to not pay CPP premiums at 9.9% on the first 50k or so.

Whether one does all this is a decision based on individual circumstances of course.

My wife and I both have a defined benefit pension plan. We are 56 years old and I am retired and my wife will be retiring next summer. If we decided to take cpp at 60, or one of us at 60 and the other at 65, will our pension monthly amount from our former employer, drop once we start receiving cpp?? Or, would the answer to the question depend on the contractual agreement and rules of your personal pension plan? My understanding is that cpp earnings have no bearing on your private pension monthly earnings, but once you start receiving OAS, your private pension would drop some at that point. Can you clarify this for me. Thanks.

Brian:

That is a question best answered by your DBP administrator. Some DBP plansallow you to take an advance on your CPP which allows you to level out the money received when combining DBP and CPP. It is usually a loan that has to be repaid with interest. That reduces amount of CPP received at 65.

I am on cpp disability and recently turned 65 where my cpp disability automatically turns in just cpp. Can I still have the option to delay my cpp till I am 70 ?

I currently am an employee of my corporation, so I pay both sides of the CPP. I soon turn 65. At that point, I will continue working at reduced hours. If I switch from salary to dividends, does that mean that I am no longer ’employed’ from CPP’s point of view? Does that mean I can now defer my CPP until later?