Zero Down Mortgages: The Last Gasp From A Housing Bubble Ready To Pop?

Since the 2008 financial crisis Canada’s federal government has taken several steps to cool the nation’s housing market; namely reducing the short-lived 40-year mortgages to today’s 25-year amortization period, and eliminating zero down mortgages to require homebuyers put down a minimum five percent.

These measures didn’t do much to slow down a rapidly rising real estate market, particularly in major centres such as Vancouver and Toronto. The national average price for a home in January 2012 was $347,732. Four years later that number would reach $470,297 – a 35 percent increase.

I feel for would-be homebuyers saving for a down payment in a market like Vancouver. You save prudently and wait for a housing correction, only to watch average home prices rise by an ungodly 30 percent in one year. How can you possibly keep up, and at what point do you throw in the towel and concede to a life of renting?

The rest of the country isn’t doing as well. In fact, you could argue Toronto and Vancouver have been propping up Canada’s housing market for years.

Alberta, whose economy is reeling from the collapse in oil prices, has seen a 2.7 percent dip in average house prices from January 2015 to January 2016. Edmonton is down 6.7 percent in that time. Newfoundland’s housing market is down 10 percent over the last 12 months.

But the housing industry, led by banks, real estate agents, mortgage brokers, and home builders, isn’t going to sit idly by while this gravy train runs out of steam. Oh no, housing is too important to the economy to let a silly thing like affordability get in the way of every Canadian’s homeownership rite of passage.

That’s why every week I look forward to receiving a copy of RealtyBook to discover local real estate, and once a month I get to revel in all the new show homes being built in the area with New Homes magazine.

The housing industry doesn’t just own my mailbox – it follows me online, floods my email inbox, and even embeds ads into my Facebook news feed:

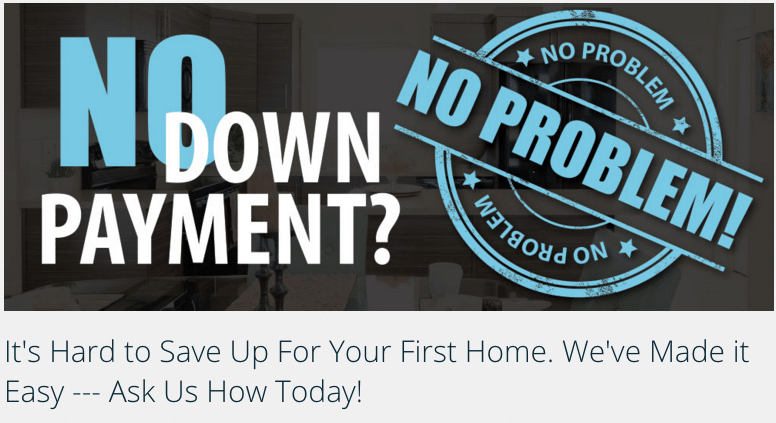

Zero down mortgages?

Talk about the sign of a desperate industry that’s determined to get anyone into home ownership at any cost: advertising the mysterious “flex-down” mortgage, which encourages borrowers to use existing credit (line of credit, credit cards(!), personal loans) to fund their down payment.

Canada’s two mortgage default insurance providers, CMHC and Genworth, actually do provide information about borrowed down payments, or what they call “non-traditional” sources of down payment, including the fact that you’ll pay a higher insurance premium on the borrowed amount.

So what exactly is going on here? The federal government did away with zero-down, 100 percent CMHC backed mortgages in 2008. Then came cash-back mortgages, where banks would lend homebuyers the 5 percent down payment in exchange for a higher interest rate. That practice was quickly banned by regulators in 2012, although it was still offered by a small number of credit unions until last year.

Well, it turns out none of these rules actually prevent lenders from offering an unsecured line of credit for the borrower’s down payment – say at a rate of prime plus 4 percent. That’s where these mysterious “no down payment, ask me how” advertisements come into play. You won’t find out the exact details unless you fill out a form and sign up with the mortgage broker or home builder.

Final thoughts

Canada’s housing industry has tried to convince us that our real estate market is different, not in a bubble, and somehow immune to a correction. It wouldn’t turn out like the U.S. housing crash because there lacked a catalyst here – that one thing that could send our housing market tumbling into recession.

But now the oil crisis is starting to cripple the economy in our prairie and maritime provinces, with massive layoffs and corporate investment abandoned or on hold.

Couple that with ultra-inflated housing prices over the last decade, not to mention the outrageous stories of mortgage brokers committing fraud, real estate agents engaging in their own dubious practices, plus this last-ditch effort to sell zero-down mortgages, and it’s hard to see this ending well for many Canadians.

I can see this ending well for patient Millennials who rent, save 20%+ of their take-home pay, and buy a home once housing becomes affordable. That’s the advice I have for my sons.

If I were in a market like Vancouver and saving for a down payment I would probably rent, or leave the area entirely. There’s no way anyone, especially a first time home buyer, should have to save that much just for a down payment relative to the average income. Vancouver is a beautiful city but it’s just not worth having that much debt.

Again, you miss the underlying fundamentals driving the real estate market in Canada, and why Toronto and Vancouver continue to accelerate while the rest of the country languishes.

There are many bargains to be had across the country – Edmonton, Calgary, Moncton, St. Johns come to mind – and with a moderate size down payment, you could purchase high quality starter homes for a mere $300,000. So why aren’t people buying these starter homes? Hint: It has nothing to do with affordability or government regulations or even the real estate market.

The bigger issue you miss while focusing on the real estate market is the lack of quality employment outside Toronto and Vancouver now that the resource sector has tanked, dragging Alberta and the Maritimes down.

Real Estate prices are driven by demand and, while some of the demand is impacted by the low interest rates, much of that demand is driven by employment patterns and trends. As long as employment remains high in Toronto and Vancouver, real estate prices will continue to accelerate until supply catches up with the demand. Trying to fix the symptom (unaffordable real estate) without addressing the cause (employment patterns and trends) is a recipe for disaster. Until unemployment reaches 40% in those urban centres, expect real estate prices to escalate until supply catches up to demand – and it will eventually. Even then, prices will level off and maybe we’ll see a moderate dip of 2 – 5% – nowhere near a US style crash.

I won’t pretend to understand all of the so-called fundamentals that are keeping the Toronto and Vancouver markets afloat. You mentioned employment being high, yet median annual household income in both centres is $76,000 – below the national median of $80,000.

The price-to-income ratio in Vancouver was 11.2 – and that was using the $850k average house prices from 2015, not the $1M+ average the city sees today.

Yes, Vancouver is a beautiful city and it attracts all sorts of demand for its real estate. But at some point it comes down to affordability.

To me, convincing people who should be renting to buy with a borrowed down payment seems like the final desperate act of an industry that’s about to decline.

That we can agree on – borrowing for a down payment is not a wise money, especially for a principal residence, in most cases.

Even in a booming market, I would not suggest borrowing money for a down payment for a principal residence as you would be over leveraged, and exposed fully to market fluctuations. As an investment, sure, borrow to the max the lenders will allow … but don’t hedge your bet by exposing that risk to the taxpayers. We don’t expect that risk; we accept the risk of helping first time buyers get into the market through CMHC but not the risk of an investor profiting from our largess.

These types of promotions have always been there … good times and bad. It is not a symptom of an industry about to decline; it is a marketing ploy like many others that comes with a price and risk.

Zero down, 5% cash back, low interest loans as down payments, vendor take back mortgages, real estate agents using their commission to offer down payment assistance – they have all been used in the past, are in use today and will be used in the future. Hey, the governments have even gotten in on the act … Assisted Hone Ownership Programs have existed in the past and will again.

“Until unemployment reaches 40% in those urban centres, expect real estate prices to escalate until supply catches up to demand”

Thanks for my laugh of the day. You do realize unemployment peaked at only 25% in the Great Depression, right? 40% would be an epic disaster.

Since 2006 Vancouver has been over saturated with Construction workers, Realtors, Home Repair stores to name a few. Any slowdown in employment in the home sector will bring not the market down. And quickly.

That renter suite bringing in $1500/ month? What if those funds dry up?

As for the Asian influx, the smart money came in long ago. Highly leveraged Chinese mainland is what you have now. Some crowdsourcing.

This is the top. Spring 2016.

I don’t really think we can foretell the future. However, one earmark of past asset bubbles is that almost nobody thought it was coming. In this case everybody is worried about it, so it does not seem bubble-like psychologically.

In Toronto, for practical purposes, there will be almost no more houses built because there is no place to put them. Some will be bought up for high-rise developments.

As a result, I see the chance of a big pullback in condo prices to be much greater than for houses, barring some economic catastrophe. Even that is moderated by the fact that many condos are viewed as starter homes now.

I suppose policies make it harder for many people to get in big trouble if things change. If someone wants to use a credit card or unsecured loan to shore up a down-payment I hope they are aware of the risk level.

Can anybody tell me which lenders are the ones doing these deals? I have contacts in each of the big five banks plus a few of the smaller lenders, and they all tell me the same thing. Each of these companies shut down an application as soon as borrowed funds are disclosed.

Is it the subprime lenders who are offering these? Or is it the non-bank prime lenders? If anyone reading knows, please enlighten me.

This is the one I kept seeing come up in my research for this post – http://www.cffbank.ca/cff-centres

“CFF Bank is a wholly owned subsidiary of Home Trust Company.”

And if you look at the contacts in each of their “centres” many are mortgage brokers working for Dominion Lending.