The federal government released its ‘Indexation adjustment for personal income tax and benefits amounts’ (IAFPITABA), which shows the increases to 2019 tax bracket thresholds, plus increases to income-tested benefits like the GST credit and Canada Child Benefit. These increases are tied to inflation using Consumer Price Index data from Statistics Canada, which pegged inflation at 2.2 percent.

Of note for many investors is the TFSA limit increase from $5,500 to $6,000. As you may know, the annual TFSA contribution limit is indexed to inflation each year and rounded to the nearest $500. If you were eligible to open a TFSA in 2009 and haven’t contributed then you’ll have $63,500 in available TFSA room.

I’m in the midst of re-filling my TFSA after several years of neglect. I was able to contribute $12,000 to it this year and plan to do the same next year. At that rate my wife and I will completely catch-up on our unused TFSA contribution room by 2024

Families receiving the Canada Child Benefit should also see a boost in their benefits next year. If you recall, the federal government announced that the CCB would be indexed to inflation starting July 1, 2018.

The indexing not only applies to the base amounts given to children under 6 and children ages 6-17, but also to the adjusted family net income at which the phase-outs begin. That places even more emphasis on the strategy I highlighted for families to get more out of the Canada Child Benefit by making RRSP contributions to reduce their adjusted family net income.

This Week’s Recap:

On Wednesday I shared 15 money saving tips to live by.

On Thursday I answered the question, is renting throwing away money?

And over on the Toronto Star I shared how to find the best cash back rewards credit card.

Weekend Reading:

Here’s Jason Heath on why you need to understand risk and uncertainty when planning for retirement.

I had a post last month on CoPower’s Green Bonds. Harvard Business Review explains why Green Bonds benefit companies, investors, and the planet.

We talk a lot about the importance of temperament for investment success. But what exactly is temperament? Here’s an excellent summary:

“Temperament, in the investment sense of the term, is how we deal with the uncertainty that comes with making decisions about the future. It is the way that we make decisions based on incomplete information where the results will often be unknown for a long time.”

Investing in the all stock ETF Model Portfolio? Take on the risk, if you can, says Dale Roberts from Cut the Crap Investing.

Hedge-fund manager James Cordier tells his clients via YouTube that he lost all of their money – some $150 million – selling options in the natural gas market:

Jason Heath tries to explain to a mother why selling her home to her son for $1 is not a good idea.

Millionaire Teacher Andrew Hallam explains why retirees and millennials face a tug of war:

“Millennials should hope that stocks stagnate for years… or that stocks fall hard. It would allow them to pay lower prices for stock market shares. As a result of lower prices, dividend yields would rise. This would increase their odds of building stock market wealth.

Some of my friends, however, are already retired. They don’t want stocks to fall. And that makes sense. Retirees are selling their stock market assets. They want to see those assets rise.”

Mark Seed at My Own Advisor says it’s never too soon to run some retirement numbers. Agreed.

Many retirees are sour on ETFs because their dividend distribution is too low. Michael James answers a reader question about rising dividends in ETFs.

Finally, here is some interesting research posted by PWL Capital about bull markets, bear markets, and the average length of a full stock market cycle.

Have a great weekend, everyone!

I’m often asked to share my best or favourite money saving tips. It’s hard to pin down just one when there are so many ways to save money and build lifelong financial habits and skills. That’s what financial literacy is all about, right?

Here are 15 money saving tips that I try to live by:

1. Make it automatic.

The key to building a life-long habit of saving is to make your contributions automatic and as painless as possible. Pick a day that coincides with your paycheque and set up an automatic transfer into your RRSP, TFSA, savings account, or RESP. Start with as little as $25 and increase it annually, or as your budget allows.

2. It’s never too late to start saving.

The best time to plant an oak tree was 20 years ago. The second best time is now. Whether you’re 30, 40, 50, or 60, it’s never too late to take control of your financial future. See tip number 1 on how to get started.

3. The power of asking.

I challenged readers a while back to take a day off work to deal with their finances. A “bill haggle” day can help reduce your monthly expenses on everything from bank fees to cable and internet to insurance. Mark it down on your calendar once a year as your reminder to save money. You never know unless you ask.

4. Does your loyalty pay?

Most of us bank at the same place we did when we opened our first savings account as a child. Ask yourself what your bank has done to deserve your loyalty. Today, there are many free banking options, and online comparison sites have made it easy to shop around for the best deal on mortgages, savings accounts, and GICs.

5. Ask for more.

When I got my first real job, I naively accepted the initial low-ball salary offer. It was a mistake that cost me at least $5,000 per year. Remember, all your future wage increases will be pegged off of your initial salary. Know what you’re worth, what the industry pays, and negotiate wisely.

6. How much you save matters more than your return on that savings.

We obsess over investment returns and are willing to move mountains to get an extra half-percent on a savings account or GIC. But in reality, your savings rate (i.e. how much you save) will make much more of an impact than your annual returns, especially in the early years. Up your monthly savings from $100 to $150 and you’ll enjoy a 50 percent increase in your savings.

7. Track your income and spending.

The foundation to solid money management is understanding how much money comes in and how much goes out every month. There’s no other way around it – how else will you know what you can afford to save?

8. Estimate your future income and expenses.

Budgeting goes beyond just tracking what you’ve spent in the past. In order to make a plan for the future, such as to buy a house or car, or save up for a trip, you need to project where your finances will be several months in advance. We often forget about those irregular expenses, such as car maintenance, birthday presents, when a raise or bonus might kick-in.

9. Avoid the trade-up trap.

Tens of thousands of dollars have been wasted because homebuilders and real estate agents invented terms like “starter homes” and “trading up”. Buy a home that will suit you for the next decade or more, and stay put.

10. That goes for cars, as well.

I like a new car as much as the next guy, but if you can’t afford to pay it off in 3-4 years max, you can’t afford the car. And quit trading one in for something new every three years! Drive your vehicle for at least 8 to 10 years so that you can enjoy some car-payment free years.

11. Simplify your finances.

In an attempt to optimize every part of my finances I forgot to account for the pain-in-the-ass factor – the time wasted researching individual stocks, hunting down credit card offers and savings account promotions, transferring money back and forth between a no-fee bank and a full service bank. There’s something to be said about finding a simple solution that you can stick with, even if it’s not the most optimal solution.

12. Develop an entrepreneurial mindset.

They say you won’t get rich working for someone else and I think that Millennials need to develop an entrepreneurial mindset in order to succeed in today’s economy. Start a business, work on a side-hustle, move across the country (or to another country) and don’t wait for the ideal career to fall into your lap.

13. Save on the big things

People often stress over gas prices, bank fees, and cell phone bills while ignoring some of the ways they can potentially save thousands of dollars. Take out a variable rate mortgage instead of a 5-year fixed rate mortgage, avoid mortgage life insurance and other creditor insurance products, switch from expensive bank mutual funds into index funds or ETFs, avoid expensive name brands when a generic brand will do, and don’t fall for deceptive or misleading advertisements.

14. Live close to work.

We save money on gas because we bought our house close to where I work. Our fuel expenses are between $100 and $150 a month. One reason I was late getting into podcasts or audiobooks is because I have a five-minute commute to work instead of a 45-minute drive or train ride.

15. Spend on things you enjoy.

I’m not a big latte fan, but if you enjoy an expensive coffee then who am I to criticize? Spend on things that bring you joy (or that save you time) and then try to save money in other areas to offset your splurges. Go ahead and share your money saving tips in the comments section below.

The month of October was not kind to investors. A volatile stock market erased all of 2018’s gains and then some. My own portfolio plunged 5.72 percent in October after being up 4.73 percent from January to September. Time to panic? Not a chance.

In yet another example of why it’s best to ignore the headlines and stick with your plan (or why I say investors would be better off taking a Rip Van Winkle like 20 year nap) the market quickly returned all of those losses in just eight trading days.

Investors who panicked at the bottom of that dip locked in losses of nearly six percent, while investors who rode out the stock market volatility saw their portfolios get back to even.

A chart showing market returns over a few days, weeks, or even months can look like a stomach-churning rollercoaster. But as the months turn to years, and the years turn to decades, those returns smooth out and trend upwards. Yesterday’s headlines become ancient history, and ‘worst days ever‘ for the stock market become tiny blips on the radar over the long term.

The point is not to panic when markets get rocky. If your investing plan has a long term focus then it’s best to ignore the daily headlines and stick to your plan.

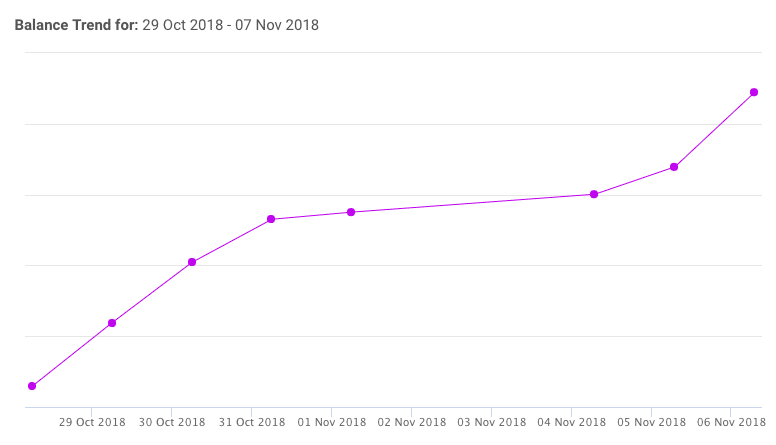

Here’s the power of ignoring the day-to-day market fluctuations and headlines, and sticking to your investing plan. Portfolio balance as of Oct 8: $231k. Balance as of Nov 8: $232k. Ignored in between: a low of $214k. pic.twitter.com/lBl4Xna9Va

— Boomer and Echo (@BoomerandEcho) November 8, 2018

This Week’s Recap:

On Wednesday I wrote about why past performance is not a good predictor of future investment returns. In fact, costs are a better predictor of returns.

In light of CBC’s recent coverage of the pitfalls of credit card insurance I looked at four big rip-offs that consumers should avoid.

Promo of the Week:

I’ve highlighted this before but if you have some upcoming spend planned for the holidays then this is an excellent opportunity to earn up to $200 cash back on your holiday spending.

That’s right, when you apply and get approved for the Scotia Momentum Visa Infinite Card you’ll earn an incredible 10 percent back on everyday purchases for the first three months, up to $2,000 in total purchases. Plus, your first-year annual fee is waived. This is a limited time offer so make sure to take advantage of it soon.

Weekend Reading:

The surprising retirement goal that 41 percent of Americans have? It’s to own a vacation home.

Will baby boomers destroy the stock market as they retire en masse? Ben Carlson examines some interesting trends and time lapses.

How Shane Parrish, a former Canadian spy, helps Wall Street mavens think smarter:

“Every world-class investor is questioning right now how they can improve,” he said. “So, in a machine-driven age where everything is driven by speed, perhaps the edge is judgment, time and perspective.”

Jonathan Chevreau highlights three online programs to help plan out your finances in retirement.

Personal finance 101: Some Canadian universities are offering practical personal finance courses.

Studies show that as we age, our brain becomes less able to detect fraud. Here’s a thoughtful post on how to safeguard your finances and protect your retirement savings.

Jason Heath explains how to avoid RRSP tax on your estate when you die.

Michael James has an excellent post explaining the value of delaying CPP and OAS until age 70. More people need to hear this message.

Last week I shared the “new rules” of personal finance. Million Dollar Journey blogger Frugal Trader looks at how these rules apply to his thinking on personal finance matters.

Dale Roberts explains the many lessons learned from a chart detailing the returns history of Tangerine’s five investment portfolios.

Finally, here’s Michael James again on whether it makes sense to hold U.S.-listed ETFs to save on MER and foreign withholding taxes. I’ve been thinking a lot about this lately and how it applies to my own two-ETF portfolio, in which I’ve chosen simplicity over cost savings. I’ll soon be at the point where the pendulum will swing towards cost savings.

Have a great weekend, everyone!