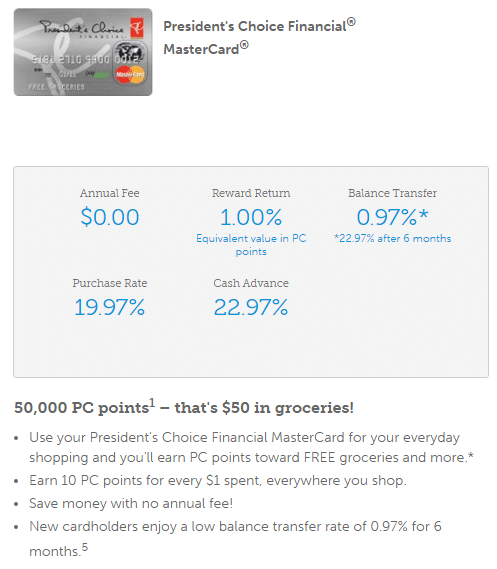

The PC Financial MasterCard has a bit of a cult following among certain rewards cards enthusiasts, and for good reason. This no-fee card pays 1 percent back in the form of PC Points, which can be redeemed for free groceries at any store where President’s Choice products are sold. Who doesn’t love free groceries?

Indeed, as I’ve written before, the PC MasterCard was my first rewards credit card and as a brand new parent I loved using PC Points to help supplement the cost of groceries, baby clothes, and diapers at the Real Canadian SuperStore.

I remember getting a $25 welcome bonus just for signing up; and from that moment I was hooked and I’ve used a rewards card to pay for my every day purchases ever since.

Of course, I’ve moved on and now use a premium rewards card to try and earn more points on my spending, but these types of cards come with annual fees and often make it complicated to redeem your points for things you want (and when you want them).

I totally get why someone would be perfectly happy to stick with a no-fee rewards card like the PC Financial MasterCard and continue to redeem their $20 in free groceries every month or two.

But even PC Financial upped its game recently when it introduced the first ever no-fee World Elite MasterCard in 2015, on the heels of Loblaw’s massive acquisition of Shoppers Drug Mart.

A premium card that requires applicants to have personal income of $70,000 per year or household income of $120,000 per year, the PC Financial World Elite MasterCard lets you earn 3 percent back on purchases made at participating stores where President’s Choice products are sold, 3 percent back at Shoppers Drug Mart, and 3 percent back at Esso gas stations.

A premium card that requires applicants to have personal income of $70,000 per year or household income of $120,000 per year, the PC Financial World Elite MasterCard lets you earn 3 percent back on purchases made at participating stores where President’s Choice products are sold, 3 percent back at Shoppers Drug Mart, and 3 percent back at Esso gas stations.

This card is a hidden gem for high income earners who again prefer a no-fee credit card and one that helps them earn free groceries on their spending. It’s a great deal for those who shop regularly at PC stores and at Shoppers Drug Mart and Esso.

A special offer from our partners at Rate Supermarket

So if you’re a fan of using a no-fee credit card to earn free groceries then our partners at Rate Supermarket have a great new offer that will give you 50,000 PC Points just for signing up for either the PC Financial MasterCard or the PC Financial World Elite MasterCard.

You’ll see why people love it – simplicity! No worrying about earnings caps, category bonuses, or using multiple cards – just earn a straight 1% back (or more) towards free groceries.

PC Financial MasterCard

Apply here for the PC Financial MasterCard and get 50,000 PC Points.

PC Financial World Elite MasterCard

Apply here for the PC Financial World Elite MasterCard and get 50,000 PC Points.

One thing people get concerned about is losing their hard-earned money in a stock market crash or by making poor investment choices. But sometimes, even people with disciplined, well-thought out investment strategies lose money in their everyday lives just by being careless.

What are some ways you could lose money?

- You could literally lose it

It’s probably not that common anymore to lose actual cash since most people don’t carry much of it around. But, have you ever misplaced your wallet and had it returned to you with all your cards intact, only to find the cash mysteriously gone?

I have read plenty of stories about people buying, for example, a second-hand couch and finding bills stuffed into the cushions. Or, someone losing an envelope full of cash on the way to the bank. Unless a good Samaritan finds it and returns it to you, you are out of luck and the money is gone.

- You could be careless with it

Back in the day when I always used cash for purchases, I would stuff any change I received (bills and coins) into my coat pocket and I sometimes forgot to put it away afterwards. With the change of seasons when I got back to wearing the coat, I’d be delighted to “find” a 10- or 20-dollar bill. I was actually being careless with my money. What if I would have given my coat to Goodwill? What if a crumpled $20 bill had fallen out of my pocket and blown down the road when I was pulling out my gloves?

Here are some other ways of being careless with your money because you’re not paying attention:

- Paying excessive service charges – evaluate how you’re using your bank accounts, check your phone plan for unnecessary data charges.

- Late fees – returning your library books late may not cost you much, but forgetting to make your credit card payment on time results in interest charges, fees and possibly an increase in your interest rate.

- Traffic ticket fines for parking, speeding and distracted driving are increasing – and may affect your insurance rates.

- Not checking a store’s return policy – especially for large ticket items. When I saw the hideous colour of my just-delivered couch I found out that there was a 20% restocking charge if I returned it. Also, it’s important to measure furniture items to make sure they will fit your space.

- Misplacing receipts that could be turned in for reimbursement at work or your medical plan, or used for tax deductions.

- You could waste it

Think of all the things we buy that we don’t need – the clothes we don’t wear and the food we throw away. What about the things we purchase and never get around to returning even if they’re the wrong size, the wrong type, or they don’t work right?

You sign up for “free trials,” hand over your credit card number, and then forget about them. How many unused subscriptions do you have – gym memberships, magazines, TV packages and your home phone?

Another way to waste money is by neglecting the maintenance on your vehicles and home. You don’t want your furnace to conk out in the middle of winter, or have to buy a new engine for your car because you were too “busy” to change the oil.

- You could have it stolen from you

There’s nothing more distressing than losing your wallet or having it – or your purse – stolen. Don’t set your purse in the shopping cart while you’re checking out the meat selection in the grocery store. Don’t leave your purse or wallet in your car, and watch out when you’re travelling or visiting tourist attractions or fairs – prime areas for pickpockets.

Besides the aggravation of having to replace all your important documents and cancelling your credit cards, the biggest problem is identity theft. Don’t carry around documents you don’t need, such as your Social Insurance card, chequebook, passport, birth certificate and multiple credit cards.

Only give your credit card number to reputable online companies and never to someone who unexpectedly phones you for whatever reason.

Put valuables and purchases in your trunk when you’re in your car. Make sure there’s no easy access to your home while you are out – an unlocked door or open ground floor window. You might consider a security system.

- You could lend it and not get repaid

If you decide to reject Shakespeare’s advice to “neither a borrower or lender be,” at least be a careful lender. It’s hard to admit that we made a loan to the wrong party.

Be smart when loaning money to friends and family. Treat the transaction as a business deal, complete with a formal contract in place outlining how much is owed, when it must be repaid and how much interest you are (or aren’t) charging. This creates accountability and increases the likelihood that you’ll actually get paid back.

Friendships end and family feuds begin all on account of well-intentioned loans that go unrecovered.

- You could gamble it away

When you take a risk, either the chances for winning should be very high or the consequences for losing should be very low.

You may feel that playing online gambling games – poker, fantasy football – or VLTs, or spending the evening at a casino is just a form of recreation and a harmless diversion. But sometimes you can get caught up in the game and spent a little more than you meant to, or start to gamble a little more often for the thrill.

Gambling is a sure way to throw away your money. Also, serious gambling problems cause harmful consequences that can negatively affect other areas of a person’s life, such as family relationships, work performance and mental health.

Buying stocks with money that you know you’ll need for a set expense in the near future, such as taxes or a down payment on a home, is taking a gamble.

- You could lose it in the financial markets

Investors sometimes get focused on only one side of the equation: making money. They can lose sight of what’s far more important: not losing it.

We have all made poor investments at one time or another, anyone, even the most experienced investor can do this. You can lose money by simply not doing proper research, getting caught up in a “bubble”, or by lacking patience. You could underestimate the liquidity, volatility, and risk of your investment choices.

Sometimes investors get so focused on wanting to double and triple their money for their ultimate financial goal that they fail to take into consideration what can happen if they lose what they have. Sometimes you can never get it back.

Final thoughts

We set aside cash for emergencies and large purchases, and set up regular automatic contributions to our investment plans.

But we can lose money in more ways than in the stock market.

Being careless, or inattentive, with your hard earned money is the equivalent of throwing it away.

Extreme frugality blogger Mr. Money Mustache and his family famously live on less than $25,000 a year. Of course, it helps to have a paid-off home and live in a relatively affordable town in northern Colorado. Getting around by bicycle or on foot also saves money on gas and keeps the family car-payment free. It’s an amazing example of frugal living which has inspired legions of followers called Mustachians.

I also track my family spending and Mustachians would be shocked to learn that the Engen’s will spend more than three times the amount of MMM’s typical family living expenses this year.

Where does all the money go? Let’s take a look at our anti-Mustachian family spending summary:

| HOME EXPENSES | $ | Comments |

| Mortgage/Rent | 15,362 | Mortgage balance of $244,000 |

| Property Taxes | 4,282 | |

| Utilities | 3,437 | Electricity, gas, water |

| Cell phone | 895 | |

| Cable/Internet | 1,666 | |

| Furnishings/Appliances | 665 | |

| Lawn/Garden | 151 | |

| Maintenance | 392 | |

| Total HOME EXPENSES | 26,850 | |

| DAILY LIVING | ||

| Groceries | 13,210 | Includes household items such as toiletries |

| Clothing | 1,421 | |

| Dining/Eating Out | 3,078 | |

| Haircuts | 640 | |

| Pet Food | 657 | |

| Alcohol | 1,252 | |

| Miscellaneous spending | 3,500 | |

| Total DAILY LIVING | 23,758 | |

| CHILDREN | ||

| Preschool expenses | 1,265 | |

| School supplies | 100 | |

| Sports | 482 | |

| Piano lessons | 750 | |

| Ballet | 490 | |

| Total CHILDREN | 3,087 | |

| TRANSPORTATION | ||

| Vehicle payments | 8,263 | Will be paid off this fall |

| Fuel | 2,246 | |

| Maintenance | 421 | |

| Registration/License | 169 | |

| Parking | 49 | |

| Total TRANSPORTATION | 11,147 | |

| INSURANCE | ||

| Auto | 1,328 | Two vehicles |

| Home | 1,400 | |

| Total INSURANCE | 2,728 | |

| CHARITY/GIFTS | ||

| Gifts | 2,050 | Birthdays, Christmas, etc. |

| Charitable donations | 755 | |

| Total CHARITY/GIFTS | 2,805 | |

| ENTERTAINMENT | ||

| Netflix | 110 | |

| Google Play Music | 96 | |

| Photography | 53 | |

| Movies/Theater | 50 | |

| Books | 30 | |

| Total ENTERTAINMENT | 339 | |

| SUBSCRIPTIONS | ||

| Amazon Prime | 83 | |

| Credit card annual fees | 219 | |

| Costco membership | 116 | |

| Library | 15 | |

| Total SUBSCRIPTIONS | 672 | |

| Vacation | ||

| Travel | 6,031 | Kelowna, Vancouver, plus misc. day trips |

| Total VACATION | 6,031 | |

| Total 2016 Expenses | 77,417 | Estimate |

We’re on track to spend an estimated $77,417 this year. Keep in mind this amount does not include any contributions toward my pension, RRSPs, TFSAs, or RESPs, and does not include any extra amounts we might pay towards our mortgage.

Turning around this anti-Mustachian budget

How can we reduce our spending down to a more respectable Mustachian level? Paying off the car this year will bring our total annual spend below $70,000 and free up nearly $10,000 to put towards our savings goals. PS – I can’t wait for the last car payment to go through in October!

Total spending could then be reduced to just $53,792 by paying off our mortgage – but that goal is at least eight years away. Besides, I prefer to steer any extra income into our savings and investing vehicles rather than using it to pay down our mortgage at 2 percent interest.

Next we have to look at groceries and household items – a category that will need to be cut in half to be on par with the Mustachian annual budget. Let’s take carve off $6,000 for groceries, and take $2,500 out of the anti-Mustachian dining out and booze budget to bring our total family spending down to $45,292 a year.

Now it’s time to get creative. I live close enough to work that I can walk, so by selling our second vehicle we can save $1,400 a year in gas, insurance, maintenance, and registration fees. So this is what Mustachianism feels like!

Miscellaneous spending can be reduced by $1,500, while cutting the cable cord can save an additional $900 a year. Scaling back on gifts and kids’ activities might put another $1,500 back into our wallet.

This would bring our family spending down below $40,000 ($39,992 to be exact!).

Vacation costs are rather high this year so we can either skip travel altogether or cut our budget in half. This takes our family spending down to between $34,000 and $37,000 a year.

Earning more vs. Spending less

I’m just going to stop right here because this is getting ridiculous and depressing. I’d have to use a scalpel to trim the rest of our expenses down to the bone and get to $25,000 a year.

Frugality can only get you so far, and even the most frugal people like Mr. Money Mustache, Sean Cooper, and Derek Foster started their journey from a position of strength. It’s easy to preach living the life you want when you already have a paid-off home, six-figure income, or made a lucky bet in the stock market.

The question is, can you live this way on your path to riches, or does it only work once you’re already there?

You can’t frugal your way to early retirement. That’s why in the debate about earning more versus spending less; I stand firmly in the ‘earn more’ camp.

Yes, we need to be prudent and watch our expenses. Believe me, I can’t wait to be car-payment free in a few months and start using that money to help reach financial independence faster.

But I’d much rather find ways to earn more money than cut out the things that make life more enjoyable.

Some extra time and effort spent on my side business this year will allow us to take out additional income of $6,000. We’ll spend a bit of that money on a trip for our 10th anniversary and save the rest. Doesn’t that sound better than cutting $6,000 from your family spending?

Readers: How much are you willing to cut from your budget in order to reach your savings goals faster? Can you live on $25,000 a year?