One of the biggest decisions as you edge closer to retirement is when to take CPP. The standard age to take your Canada Pension Plan benefits is when you turn 65; but you can take a reduced CPP retirement pension as early as 60, or you can get an increased benefit by delaying CPP up to age 70.

I asked Doug Runchey, pension expert at DR Pensions Consulting, to weigh-in on the benefits of taking CPP early versus late.

Taking CPP early

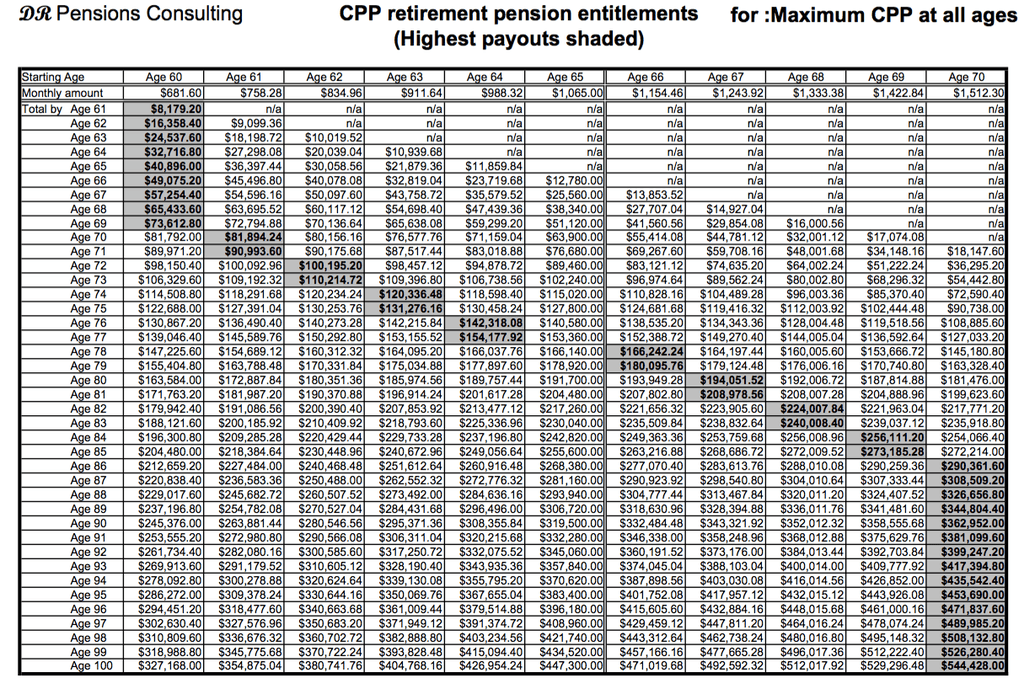

The earliest you can take your CPP benefits is the month after your 60th birthday, but you’ll get 36 percent less than if you had waited until 65.

This chart shows the monthly CPP pension you’d receive if you retired in 2016 and elected to take your benefits early:

| Age | Reduction | Monthly benefit* |

| 60 | 36.0% | $681.60 |

| 61 | 28.8% | $758.28 |

| 62 | 21.6% | $834.96 |

| 63 | 14.4% | $911.64 |

| 64 | 7.2% | $988.32 |

*Assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP early:

When you take CPP at 60, your benefits are based on your best 35 years of earnings, rather than your best 39 years of earnings if you were to take it at 65.

If you’re confident that you will be eligible for the Guaranteed Income Supplement (GIS) once you reach 65, you should generally take your CPP at 60.

Finally, if you’re thinking about taking CPP early because of ill health, always apply for a CPP disability pension instead.

“If approved, the CPP disability amount will always be higher than a retirement pension and it will convert to a full retirement pension at 65,” says Runchey.

Taking CPP late

The advantage to taking CPP after 65 is that you’ll receive a healthy 8.4 per cent increase for each year you delay receiving benefits, up to age 70. That works out to a 42 percent incentive for taking CPP at 70 instead of 65.

This chart shows the monthly CPP pension you’d receive if you delayed taking your benefits until after age 65:

| Age | Increase | Monthly benefit* |

| 66 | 8.4% | $1,154.46 |

| 67 | 16.8% | $1,243.92 |

| 68 | 25.2% | $1,333.38 |

| 69 | 33.6% | $1,422.84 |

| 70 | 42.0% | $1,512.30 |

*assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP late:

You will always get more CPP by waiting, even if you’re not working.

Runchey says that your “calculated (age-65) retirement pension” may decrease if you’re not working between age 60 and 65, but the age-adjustment factor will always make up for that decrease, and then some.

“In that situation I use the expression that you will receive a larger piece of a smaller pie if you wait, but you will always get more pie,” he said.

If you’re withdrawing RRSPs from age 60-70, it makes sense to defer your CPP until age 70 when you might be in a lower tax bracket.

The Verdict: When to take CPP

The choice of when to take CPP should be based on your individual numbers and take into account your life expectancy, current and future tax bracket, your immediate versus future income needs, plus the impact that taking CPP early has on any other benefits that you’re receiving, such as GIS and OAS.

One thing that’s clear, according to Runchey, is that taking CPP at 65 is never your optimal choice from a CPP payout perspective.

The bottom line: You will always eventually be ahead if you take CPP later.

As you can see from this chart (click to open in a new window), you will be ahead financially – considering the CPP only – if you take your CPP:

- At age 60 and if you don’t live past age 69

- At age 61 and if you live past age 69 but not past age 71

- At age 62 and if you live past age 71 but not past age 73

- At age 63 and if you live past age 73 but not past age 75

- At age 64 and if you live past age 75 but not past age 77

- At age 66 and if you live past age 77 but not past age 79

- At age 67 and if you live past age 79 but not past age 81

- At age 68 and if you live past age 81 but not past age 83

- At age 69 and if you live past age 83 but not past age 85

- At age 70 and if you live until at least age 86

Final thoughts

If you’re unsure about your Canada Pension Plan benefits, have questions about the optimal time to take your CPP benefits, or simply want to go over some different scenarios, I highly recommend consulting Doug Runchey at DR Pensions. He charges a fee-for-service, and in many cases it is well worth the money.

Also read:

Understanding your retirement benefits: Part 1 – CPP

Understanding your retirement benefits: Part 2 – OAS

Understanding your retirement benefits: Part 3 – Private Pension Plans

There’s an ‘a ha’ moment for many people when they decide to get serious about their finances. It may come after years of drowning in debt or after reaching a milestone like marriage or having children. If now is your moment, here are five ways to take control of your money:

Get going: Step one is to decide what needs to change. For singles, that means some serious thinking about your goals and what you want to accomplish. Couples will need to get on the same financial page and decide what’s important to them.

You can’t accomplish every goal at once and so you’ll need to prioritize. Start with a net worth statement and list everything you own and owe.

This is the yardstick used to measure your progress over time. Your net worth may be small, but your objective should be to grow it each and every year.

You need a budget: Before you decide how much to save and allocate toward your goals you have to know much you spend and how much is left over at the end of the month. To do this – there’s no way around it – you need to track every dollar you spend.

There are apps and software to automate the budgeting process but, as Carl Richards, author of The Behavior Gap said, when you automate you miss the chance to understand what the numbers mean.

“The act of looking at each receipt and adding those numbers mimics the act of hearing something and then putting it in our own words. We know where the money went, and, hopefully, we know why,” he said in a recent New York Times column.

That’s why Richards is a big proponent of manually tracking and recording your monthly spending with an Excel spreadsheet.

Watch where the cash goes: Once you’ve tracked your expenses for three months you’ll have an idea where your money is going. Now is a good time to make changes in areas that don’t align with your goals and values.

If there’s not enough left over to meet your objectives, you need to go back to your spending report and find additional areas to save (or earn) more money.

Match your spending to your goals and use any extra savings to fund your top two or three objectives. For example, that could mean paying off credit card debt, saving for a down payment, or starting an RESP.

Review your insurance coverage: Do you have enough insurance to protect yourself and your family in case of disaster?

Some employers provide group life coverage that tops-out at around 2.5 times your salary. That may not be adequate if you have young children and a sizeable mortgage. Research your options for term insurance. A 30-year-old non-smoking male living in Ontario can expect to pay about $50 per month for a 25-year term with a $750,000 face amount.

As for disability insurance, you’ll want enough to replace at least 60 percent of your income in case you get sick or injured. Most workplace benefit plans include disability insurance but review your coverage.

An emergency is no time to be scrambling for cash. Devise a strategy to deal with short and long term needs whether a cash buffer, an untapped line of credit, or stocks inside your tax free savings account.

What type of investor are you?: Your goals will likely include some type of long term savings plan.

Whether you go it alone as an investor or use an advisor, it’s important to know what type of investor you want to be and to stick with your plan for the long term. The point is to understand who you are, how much time you want to spend on your investments, and how much risk you’re willing to accept.

It’s prudent to check-in from time-to-time to review your progress and make any necessary adjustments along the way. Try to predict what your finances might look like a year from now, or five years from now. What’s on the horizon?

Keep score by updating your net worth statement. You’d be surprised how quickly you can move the needle forward once you’ve taken control of your finances.

We all like to compare ourselves with others when it comes to our financial affairs to see how we are doing.

The most recent Statistics Canada compilation of how Canadians spend their money shows an average spending pattern. Figures are from 2013 – so a bit dated considering economics in the past year – but it’s a good guide.

Average Canadian income was $76,550 and average Canadian consumption was $58,592. Here are average amounts in certain categories.

| Food | $ 7,980 | 14% |

| Shelter | $16,387 | 28% |

| Clothing | $ 3,550 | 6% |

| Transportation | $12,041 | 21% |

| Recreation | $ 3,922 | 7% |

| Health Care | $ 2,407 | 4% |

| Tobacco & Alcohol | $ 1,331 | 2% |

| Savings | $ 8,764 | 15% |

How does your spending compare?

Budgets are very individual and your spending may not be anywhere near the average noted here.

Related: How to save money on groceries

Grocery purchases, for example, depend on the size of your family and your dietary preferences. A family with four active teenage boys will spend more than one with two toddlers. People who favour gourmet and organic food will have a larger budget than those who buy less expensive store brands and discount produce.

Clothing is another category that can vary widely depending largely on your workplace and preferences. I dislike going to the mall so I avoid shopping whenever possible. Recently, while showing my mom pictures of her great-grandchildren, I was dismayed to see that my wardrobe has hardly changed in the past six, or so, years.

You may want to scrimp on a certain category in order to spend more in another. It’s all about individual choices.

Besides personal preferences, the region you live in makes a difference to how much you spend. Compare these three provinces.

| Category | Alberta | B.C. | Ontario |

| Total Expenditures | $71,429 | $61,007 | $60,718 |

| Food | $9,295 (13%) | $8,084 (13%) | $7,843 (13%) |

| Shelter | $19,532 (27%) | $18,766 (31%) | $18,074 (30%) |

| Clothing | $4,610 (7%) | $3,451 (6%) | $3,680 (6%) |

| Transportation | $15,360 (22%) | $11,184 (18%) | $12,103 (20%) |

| Recreation | $5,118 (7%) | $3,909 (6%) | $3,986 (7%) |

| Savings | $9,711 (13%) | $11,224 (18%) | $9,625 (16%) |

Final Thoughts

Your spending habits play a huge role in your overall financial health. It’s important to make sure that your budget is balanced and you are living within your means.

These tables can help you compare your spending with the average Canadian. If you find yourself spending above-average amounts of money in certain areas for no compelling reason, it may be a sign that you need to adjust your spending habits.

Over-spending on regular monthly expenses will have an affect on your ability to save and can result in excess consumer debt.