Investors should lower their expectations for future stock returns. I’ve been saying this for a while now, but it bears repeating again now that stocks have gotten off to such a rocky start this year.

Markets are largely efficient and tend to go up over the long term. But they can certainly overshoot expectations in the short term. Remember that Canadian and US stocks have returned an average of 8-10% over a very long period of time. But the actual annual returns have ranged between -47% and +47% (1929 – 2022).

Investors have short memories. A raging bull market feels like it can last forever and investors become overconfident with their risk tolerance.

Many conversations with readers and clients over the past two years have been about FOMO. Investors with a conservative to moderate appetite for risk suddenly hunger for higher returns and want to dial up their equity exposure or tilt it towards assets with strong recent performance (crypto, tech, clean energy, or simply more US stocks).

That’s understandable when Canadian and US stock markets soared 25% last year. But we can’t expect markets to rise by double digits every single year. Heck, we can’t expect a 60/40 balanced portfolio to deliver double-digit returns like it did in 2020 and 2021.

Indeed, that’s why we shouldn’t be surprised to see a sharp price correction like we’ve seen this past month to bring prices back in line with reasonable valuations and expectations. This is a feature of the stock market, not a bug.

But largely the same investors who were eager to dial up their risk to chase past returns have been even more vocal about January’s poor returns. They want to know why their portfolio isn’t working.

To be blunt, if you don’t know your risk tolerance the stock market will decide it for you.

Behavioural psychology has taught us that the fear of missing out on theoretical gains from holding a less risky portfolio will only feel half as bad as losing actual money when your riskier investments crash.

Worse than increasing the risk profile in your portfolio to chase higher returns would be to completely abandon ship and sell now that markets have fallen. Now you’re locking in those losses for good.

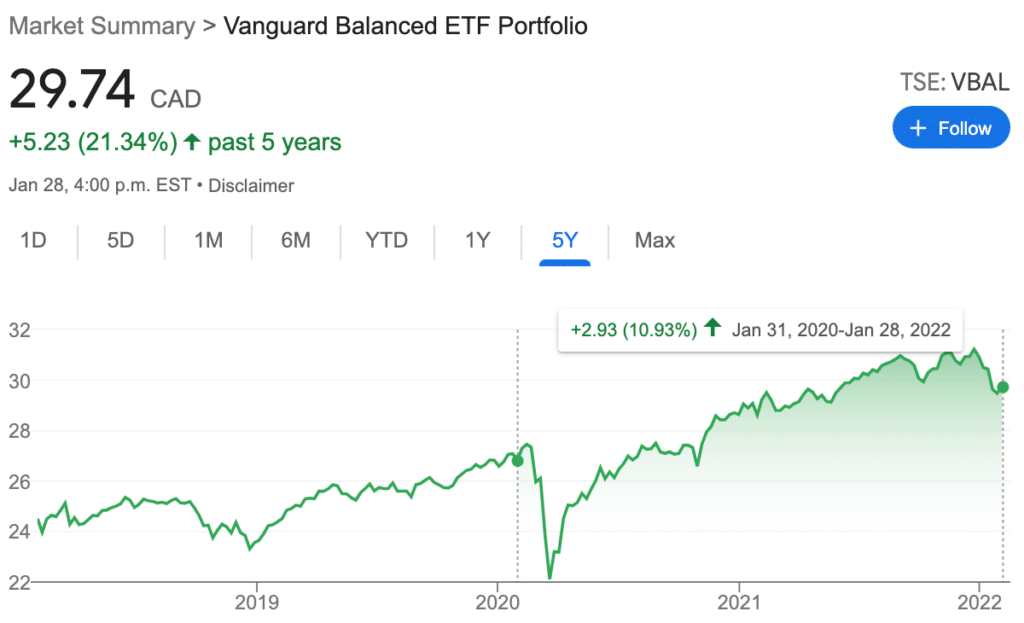

Zoom out. Take a breath. The broader Canadian market is down 2% on the year. That basically takes us back to November 30th price levels. How did you feel about your portfolio then? The S&P 500 is back to mid-October price levels. Again, were you in panic mode back then?

Balanced portfolio investors (represented by VBAL) have seen their holdings dip back to price levels not seen since early October. But if you zoom out one year, a balanced portfolio is up a respectable 3.95%, plus dividends. Zoom out two full years and it’s up nearly 11%, plus dividends.

Predict a Stock Market Crash

With that out of the way I want everyone to watch this excellent video by Preet Banerjee about predicting stock market crashes. You’ll see that the best investing strategy is to pick an asset mix that you can stick to for the long-term and ignore the short-term gyrations of the market.

More than just avoiding the worst mistake (selling everything and going to cash), a big lesson here is to resist the urge to do something based on current market conditions.

As PWL Capital’s Ben Felix says, “your investment strategy shouldn’t change based on market conditions.”

Now I want you to play the stock market timing game that Preet shared in the video and share your results in the comments. In my first attempt I sold out quickly after a 20% gain only to watch the market climb nearly 100% in the three-year period (early 1950s time period).

I’m sure you’ll find that a buy and hold strategy outperforms all but the luckiest market timers.

This Week’s Recap:

It has been a while since my last weekend reading update. I’ve since shared my net worth update for 2021. I also shared some tips on how to save more this year.

My retirement readiness checklist was a big hit. So was my recap of Vanguard’s 10-year anniversary in the Canadian ETF space.

This week I also busted a myth about working overtime with the next tax bracket myth.

I’m an emotionless robot when it comes to investing and so I stick with my simple one-ticket diversified portfolio (VEQT). But many investors adopt a core and explore approach to their investments and my latest MoneySense article offers some guidance on how to manage the riskier part of your portfolio.

Promo of the Week:

If you’re looking to change up your credit card rewards strategy (or start some light travel hacking) then our friends at Credit Card Genius have you covered with the best credit cards for 2022.

Once again the American Express Cobalt card tops the list of best overall credit card. My wife and I both use the Cobalt card for groceries and dining out.

What about your card – did it make the list?

Weekend Reading:

Economics professor Trevor Tombe offers a great explanation of what’s driving inflation in Canada. Worth a read for those who think the Bank of Canada simply needs to pull a lever to make this go away.

The Canadian Real Estate Association says its house price index was up 26% in 2021, the fastest pace on record.

Morgan Housel explains why it’s hard to distinguish what’s happening from what you think should be happening.

A terrific read on five investment lessons from the latest word craze – Wordle.

Millionaire Teacher Andrew Hallam shares a dumb investment mistake even smart people make:

“Unfortunately, buying last year’s top-performing funds is a bit like peeing in your own bathwater.”

Blair duQuesnay reminds us that we don’t get to choose when markets sell off.

John Robertson takes a deep dive into free investing apps and concludes, “Do not trade on your phone.”

Back to Preet Banerjee with another excellent video, this one examining the phenomenon of crypto FOMO. He looks at whether the early crypto returns can be repeated, and why you may already have exposure through the holdings in your index funds:

Here’s an interesting (and disturbing) look at what you learn from a year of watching bad financial advice on TikTok.

A Wealth of Common Sense blogger Ben Carlson shares his favourite investing performance chart for 2022 – the asset allocation quilt.

Should you invest a lump sum of mooney immediately or dollar cost average in over time? My Own Advisor Mark Seed shares the answer.

Jason Heath answers a reader question about whether you should apply for OAS if you have a high income.

Michael James on Money says now is a good time to decide whether your portfolio is too risky.

CPP benefits are indexed to inflation and that makes the case for deferring your CPP stronger than ever (subscribers).

Finally, remember the Beanie Baby crazy? Here’s what happens when the frenzy ends and the world doesn’t value your valuables.

Have a great weekend, everyone!

Let’s bust a myth about working overtime. Some employees incorrectly believe that when earnings from overtime, a bonus, or salary increase pushes them into another tax bracket they’ll actually take home less on their paycheque than before.

Some employees even refuse to work overtime because they believe they’ll pay more taxes and earn less money in the end.

I’m sure you’ve all heard of the next tax bracket myth.

Next Tax Bracket Myth

Here’s an example. An employee makes $50/hour and works 37.5 hours per week for 50 weeks per year. That works out to $93,750 per year before taxes.

Living in Alberta this employee pays $21,736 in taxes and takes home $72,014 after-tax for an average tax rate of 23.19% and a marginal tax rate of 30.50%.

The marginal tax rate is important because it’s the amount of tax paid on an additional dollar of income.

Here’s where the next tax bracket myth comes into play.

The employee is asked to work 20 hours per month of overtime and earn time-and-a-half for those hours – or $75 per hour. Over the course of a year the employee earns an additional $18,000, pushing their total salary earned to $111,750.

How does this affect the amount of taxes paid? Let’s take a look:

The employee now pays $27,851 in taxes for the year but takes home $83,899 – an increase of more than $11,800. The average tax rate is 24.92% while the marginal tax rate has jumped to 36%.

Problems with overtime earnings occur depending on how much tax the employer withholds at the source. This can work one of two ways:

- Source deductions are applied as if the employee remains at an average tax rate of 23.19%. The employee earned an additional $1,500 from overtime work but the employer only withheld $347.85 in taxes. This results in more money in the employee’s pocket every month; however there will be a tax-bill owing at tax time, resulting in an unhappy employee.

- Payroll can, however, withhold a greater amount of tax at the source in the case of a bonus or overtime earnings. For this example let’s say the employer withholds 36% of the overtime wages, or $540 per month in taxes.

In the second example, the employee is now upset because $1,500 in overtime earnings resulted in just $960 in additional take-home pay. Extrapolate these deductions over 12 months and the result is a fairly significant overpayment in taxes.

The good news is that the employee will get a refund at tax time.

Origin of the next tax bracket myth

My gut feeling is that the second scenario is more common and employees see more taxes deducted at the source when they work overtime or get a bonus.

Related: 5 myths about insurance

Some back-of-the-napkin math shows that the employee’s actual hourly rate for the overtime worked was just $48 (before the tax refund).

Employees might look at this and determine that picking up overtime is not worthwhile because they’ll earn less than their regular hourly rate after taxes. Enter the next tax bracket myth.

But this is simply not true. You can’t take the after-tax hourly rate and measure it against a pre-tax hourly rate. You have to compare apples-to-apples.

The employee’s regular hourly rate after taxes is $38.41. The actual overtime hourly rate is $48. Sure, it’s not exactly time-and-a-half. But the employee is clearly making more money working overtime regardless of the shift into the next tax bracket.

Final thoughts

Some people are confused about the difference between their average tax rate and marginal tax rate. Your average tax rate is simply the amount of tax paid divided by your income.

Related: 9 money myths experts wish you’d stop believing

Since Canada has a progressive tax system your average tax rate will always be lower than your marginal tax rate.

So just because a raise or another source of income bumps you into the next tax bracket doesn’t mean ALL of your income is now taxed at that rate.

Consider this myth busted.

This is the story of why we ditched our Endy mattress and chose Novosbed for our remodelled bedroom.

Four years ago, my wife and I wanted to replace our 12-year-old Sealy Posturepedic mattress. We heard about the bed-in-a-box trend – dozens of brands were selling foam mattresses online and shipping them directly to consumers – and so we decided to investigate. We pored over countless reviews and comparisons before testing out three different queen mattresses: one from Endy, Casper, and Bear. Ultimately, we chose the Endy mattress and slept comfortably on it for the next three-and-a-half years.

We remodelled our bedroom late last year (because who hasn’t renovated something during these times) and decided to upgrade to a king bed. That meant we needed a new mattress and, naturally, Endy was our first choice.

We paid $950 for an Endy king mattress and received it within a few days. After unboxing the mattress and letting it form to size, we laid down and something didn’t feel right. We had a horrible sleep that night! The mattress was not as firm and did not feel like the same material that was used in our old Endy queen mattress.

Of note, Endy was purchased by Sleep Country in November 2018. I reached out to Endy’s customer care team, and they confirmed that something had indeed changed:

“Yes, we did change the materials from a few years ago to now, we use air capsules whereas before we were using a cooling gel.”

In addition, the quality did not seem the same. It wasn’t as firm, or as thick as our previous mattress. The Endy ‘specs’ said the mattress was 10” thick but ours didn’t even reach 8” thickness after 48 hours. Also, the corners of the king mattress didn’t lie flat, they curled up.

Novosbed Review

Disappointed with our new king mattress we returned the Endy and started the shopping process all over again. We heard great things about Novosbed, which is another Canadian-owned and operated company selling mattresses online.

In fact, Novosbed launched the world’s first risk-free sleep trial back in 2009. They expanded their line-up of mattresses over the years to include brands like Douglas, Logan & Cove, Recore, and Brunswick to name a few. Now rebranded as GoodMorning.com, they’re one of Canada’s largest independent online-only mattress retailers.

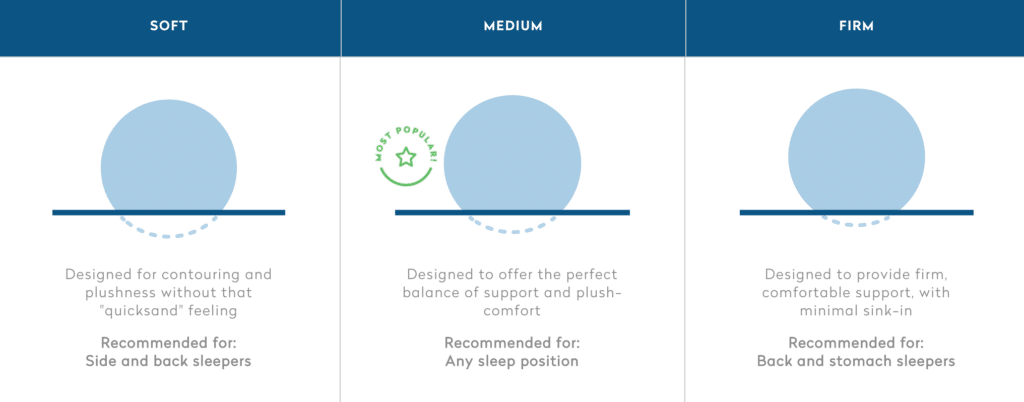

What we liked immediately about Novosbed is that they offered three choices of firmness instead of a one-size-fits-all choice like Endy and most other foam mattress retailers offer.

To select the appropriate firmness option Novosbed has a handy questionnaire and recommendation tool online. It includes the following questions:

- Do you sleep by yourself or with a partner?

- Height and weight of you and your partner

- Are you a side, back, or stomach sleeper?

My wife and I prefer a firmer mattress and so we chose The Novosbed – Firm.

Novosbed Pricing:

Novosbed describes itself as an affordable luxury mattress. It’s made of premium, high-density memory foam and is made in North America. Their mattresses come in the following sizes and price points:

| Size | Price |

| Twin | $999 |

| Twin XL | $1,099 |

| Full / Double | $1,199 |

| Queen | $1,399 |

| King | $1,599 |

| California King | $1,599 |

Shipping is free and usually takes 1-7 business days within Canada. Each Novosbed comes with a machine-washable cover. Shoppers can choose from three ‘firmness’ options (soft, medium, or firm) and the mattresses are 11” thick.

Sleep Trial

Novosbed has a generous 120-night sleep trial, one of the longest in the industry. If you don’t like your Novosbed mattress you can return it within the 120-night sleep trial and Novosbed will issue a full refund and make arrangements for the mattress to be picked up (typically gets donated to a local charity).

Novosbed also lets you fine-tune the firmness. After 30 nights, if you’re not in love with your mattress, Novosbed will send you a free Comfort+ kit to make your mattress firmer or softer.

Our experience with Novosbed

We ordered our Novosbed King mattress through GoodMorning.com and received it within three business days. The mattress-in-a-box is heavy and took two of us to lug it up the stairs and into our bedroom.

We unboxed it, removed the plastic wrap, and rolled it out onto the bed frame. The mattress decompresses within about 30 minutes but takes around 24 hours to reach its full intended comfort.

It can take some time to adjust to a foam mattress if you’re used to sleeping on a spring mattress. For us, since we had slept on a foam mattress for four years, we knew after the first night that this mattress was “the one”.

We’d say the Novosbed firm mattress is slightly firmer than our old Endy queen mattress, but not as firm as the Bear mattress that we tested out years ago. The Novosbed mattress provided the firmness we were looking for with a comfortable ‘sink’ that hugs you while you sleep.

We’re thrilled with our Novosbed king mattress and are now enjoying our remodelled bedroom. If you’re looking to make a mattress change or upgrade your sleep experience, I’d highly recommend checking out Novosbed.

*GoodMorning.com provided product in exchange for my honest review. All opinions are my own.*